In September 2008, Lehman Brothers collapsed, precipitating the worst global financial crisis since the Great Depression.

Excessive debt-especially mortgage debt funneled through a dizzying array of high-risk financial instruments-was the main culprit in the near-collapse of our financial markets. But the question with ten years gone by is: how has our relationship to debt changed?

A recent report released by Lending Tree looks at this question in detail. It is no surprise that the consumer debt landscape has changed significantly in the past decade. In this post, we’ll take a look at these changes, many of which we’ve touched upon in previous posts this past year.

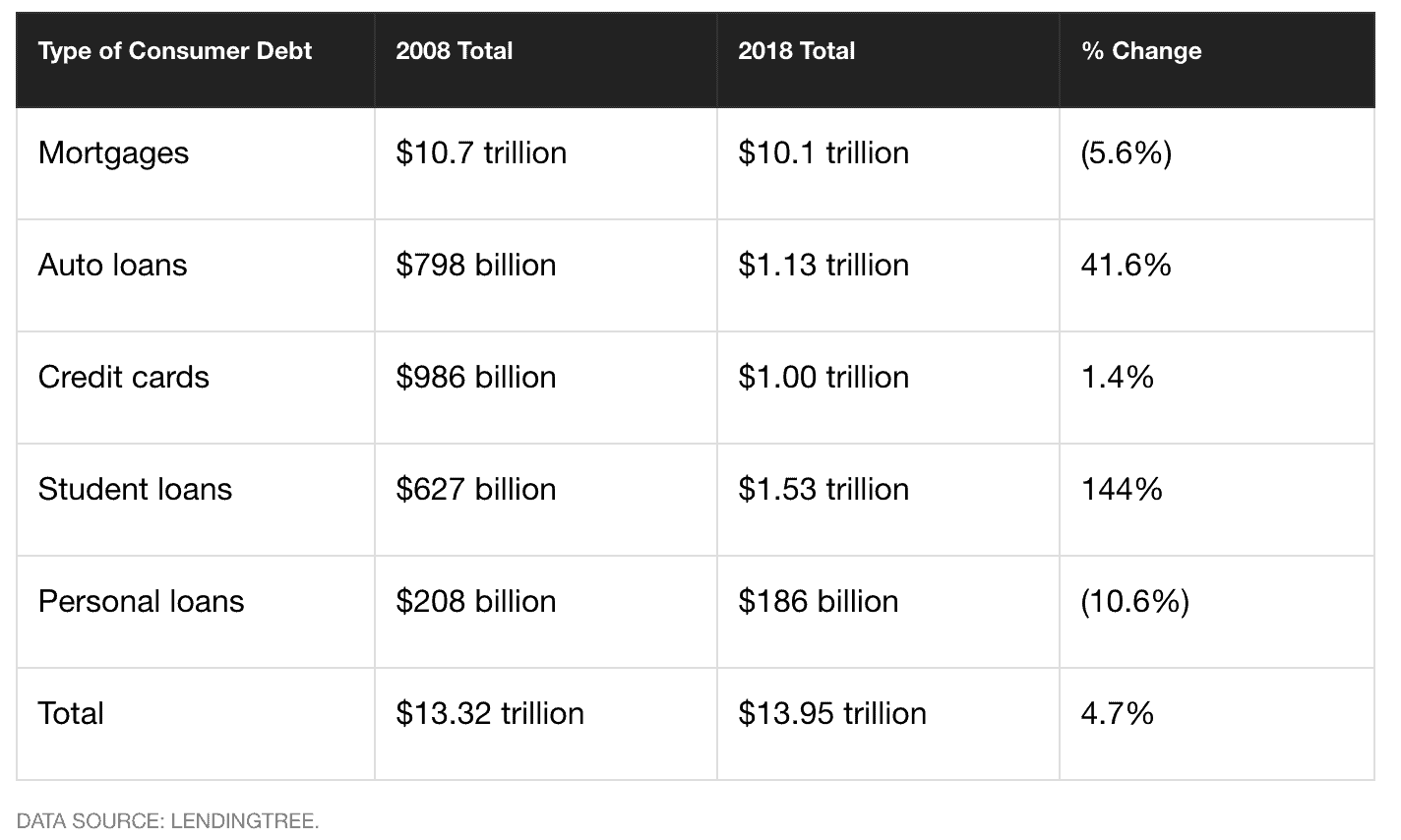

OVERVIEW

As we can see from the table below, there have been dramatic shifts in debt allocations since the financial crisis:

Let’s take a closer look at each sector.

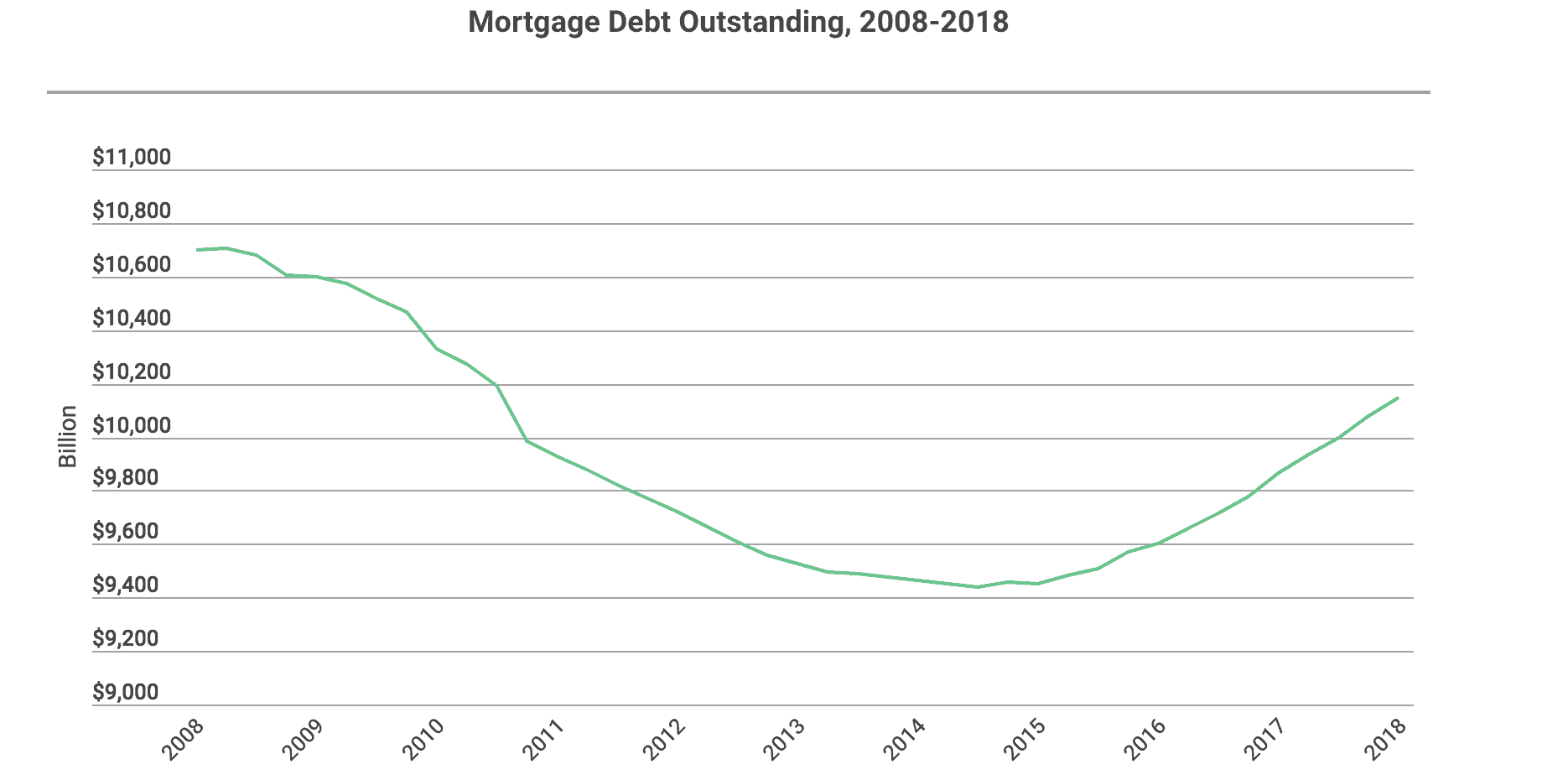

MORTGAGES

2008: $10.7 trillion

2018: $10.1 trillion

Annualized percentage increase since 2008: 0.5%

Current annual rate increase: 2.8%

Not surprisingly, mortgage debt, while still the largest sector by far, is considerably lower than it was in 2008. Home prices are still lower than their pre-crisis peak in some of the hardest hit areas.

It is fascinating to consider that in 2008, the average mortgage-to-income level was nearly 100%. Today, the same level sits at about 68%. Net, there just aren’t as many homeowners severely overextended as there were ten years ago.

The graph below shows us how mortgage debt has trended over the decade.

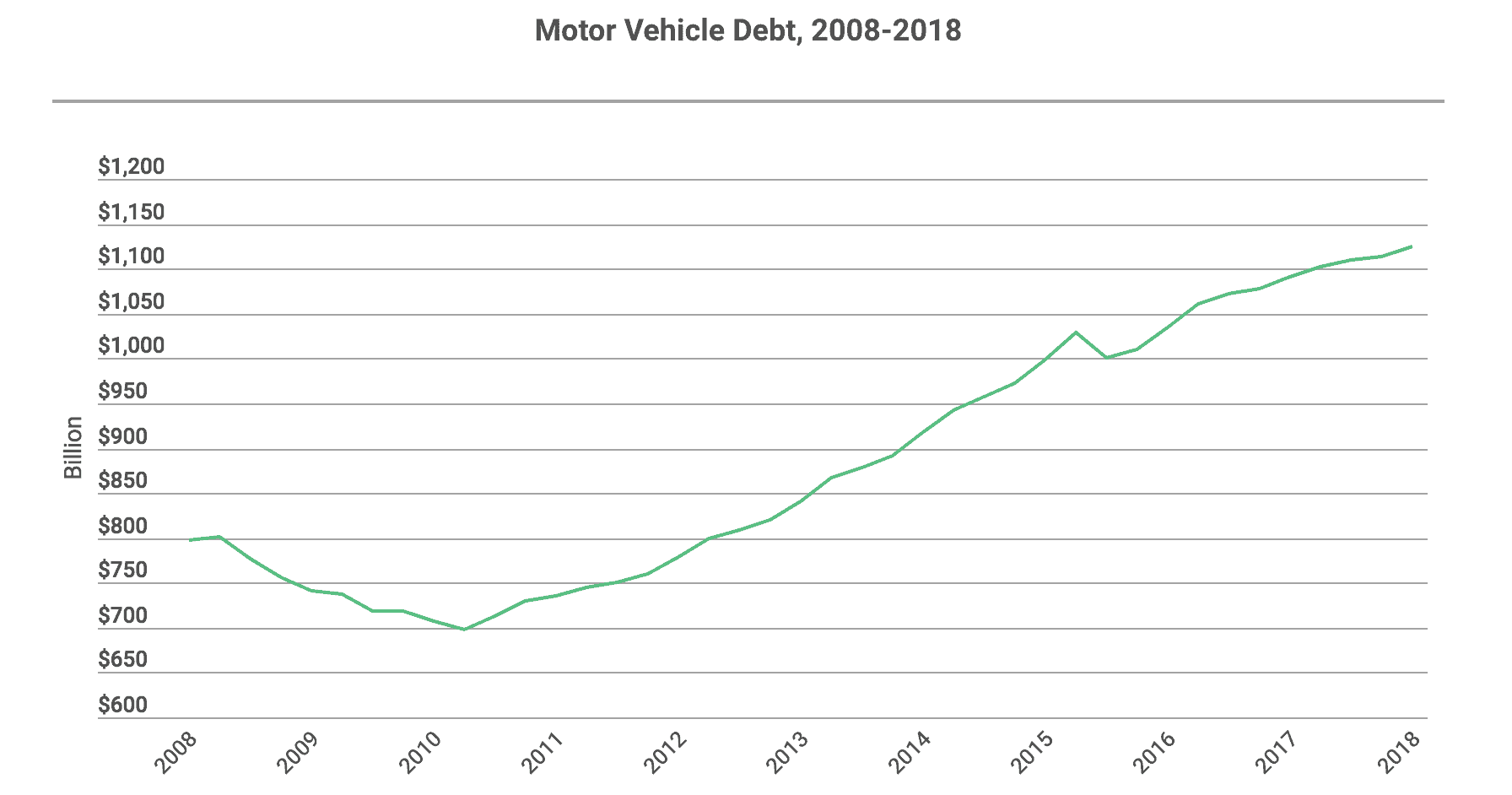

AUTO LOANS

2008: $798 billion

2018: $1.1 trillion

Annualized percentage increase since 2008: 3.5%%

Current annual rate increase: 3.1%%

Auto loan debt has risen more than 40% since the financial crisis, driven by several factors:

- The average price of new cars has risen about $8,000, from $28,000 to $36,000. At the same time, consumers are buying more units, going from 10 million in 2011 to more than 17 million by summer of 2018.

- With higher prices, more consumers are taking extended repayment plans, with the average term now approaching 70 months.

- The subprime auto-loan market has taken off. Sub-prime mortgages were, of course, a major factor in the 2008 collapse. Now we’re seeing similar trends in the automotive sector, with nearly 25% of all loans being given to consumers with sub-prime or deep-sub-prime credit ratings.

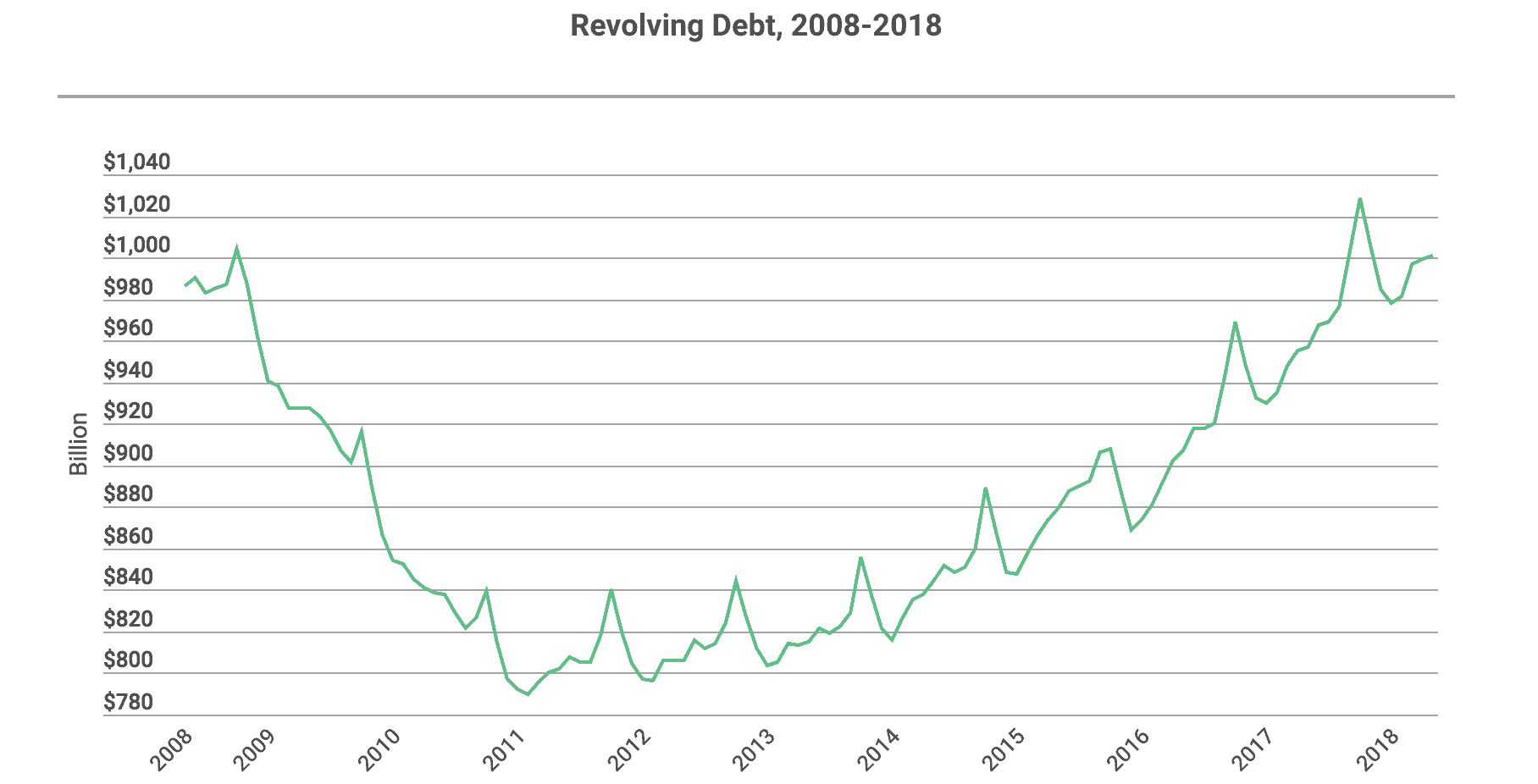

CREDIT CARDS

2008: $986 billion

2018: $1.0 trillion

Annualized percentage increase since 2008: 0.1%

Current annual rate increase: 4.5%

Credit card debt has exhibited the most erratic trends over the past decade. As the graph below shows, consumers cut back on credit card usage in the three years following the financial crisis. In fact, credit card spending was down 21% by 2011. But consumer confidence has rebounded in subsequent years, prompting consumers to reach for their credit cards more frequently. Only recently has credit card debt risen slightly beyond its 2008 level.

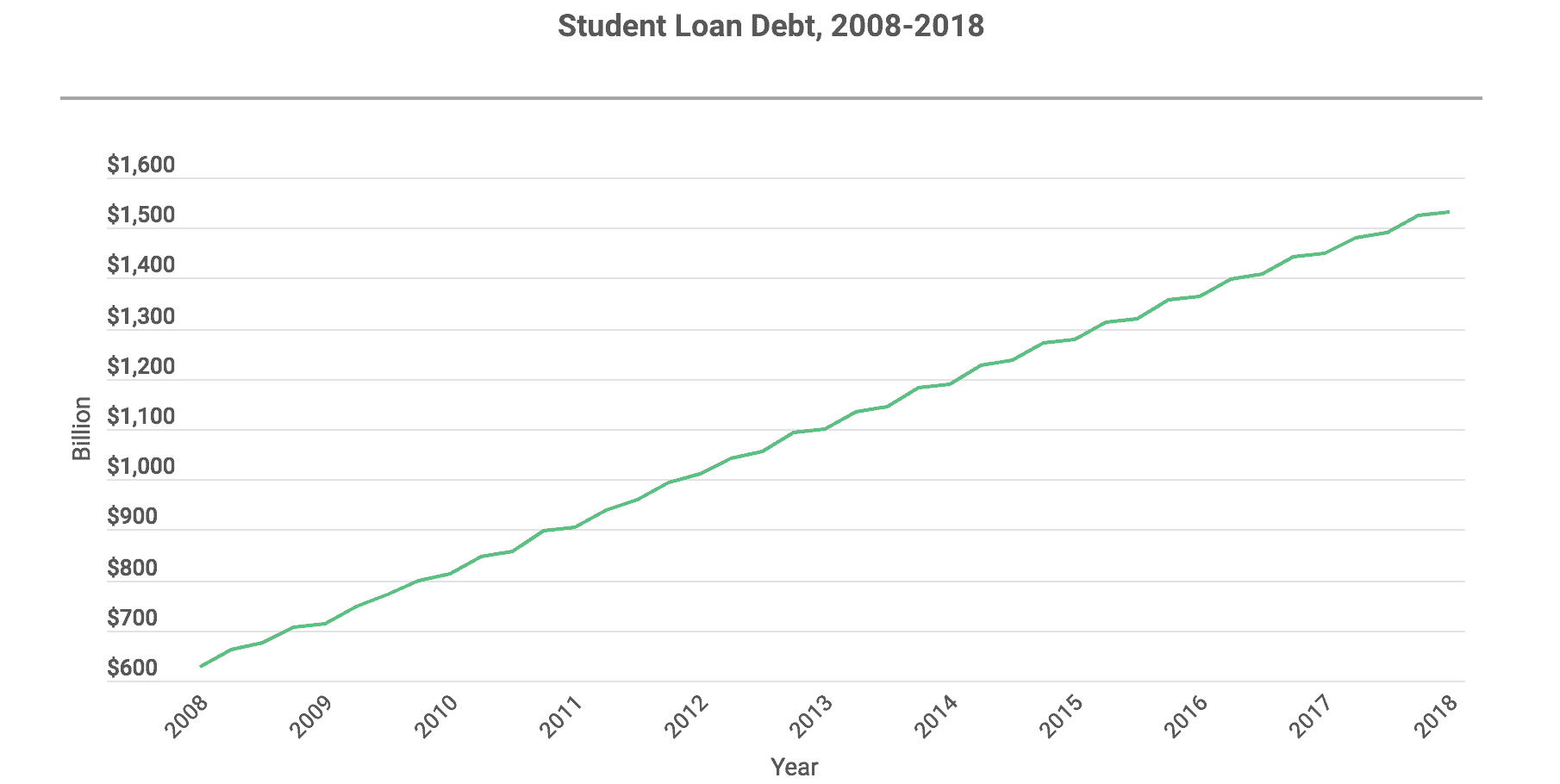

STUDENT LOANS

2008: $626 billion

2018: $1.5 trillion

Annualized percentage increase since 2008: 9.3%

Current annual rate increase: 5.7%

As we detailed in a recent post, student loan debt since the Great Recession has increased by 144%. This, of course, is driven by both increased demand for secondary degrees and soaring college tuition rates. Neither of these factors seems to be changing as families still are betting on the long-term benefits of a college degree.

CLOSING OUT THE YEAR

The economy is strong, unemployment is low and interest rates are climbing. As a result, Lending Tree estimates that non-mortgage debt will surpass $4 trillion by the end of the holiday season…up from $3.8 trillion in July of this year.

SOURCES

https://www.lendingtree.com/debt-consolidation/consumer-debt-outlook-september-2018/

https://www.fool.com/retirement/2018/09/23/10-years-later-how-has-americas-consumer-debt-evol.aspx