In 2008, the U.S. economy took a precipitous fall that began with the collapse of global financial firm Lehman Brothers, leading to what has been labeled “The Great Recession.”

Jobs vanished, houses were foreclosed on, retirement accounts shrank to virtually nothing – and it all started with soaring home prices and risky lending practices that gave borrowers more debt than they could manage.

Fast forward 10 years and the housing and job markets have largely recovered, but the U.S. faces another financial crisis with its roots in the recession: the incredible growth of student debt.

Student debt is now the second largest source of household debt in the country, coming in only behind home loans. College costs have grown an estimated three times the rate of inflation over the last 20 years and more than 70 percent of college graduates carry educational debt.

Various estimates show total debt at somewhere between $1.3 and $1.5 billion, an 80 percent increase since 2008. Most student loans are federally backed, so this is – or should be – a concern to everyone, whether they hold personal student debt or not. Let’s examine three of the primary causes of the student debt crisis and the future ramifications of the issue.

The Decline of Vocational Education: To talk about these factors is a bit like the chicken and the egg: which came first? Vocational education began declining in the late ‘80s as more parents began pushing their children to four-year universities and public schools phased out vocational-technical programs like auto body repair and metal shop. Thus, fewer high school graduates planning to enter the workforce directly after graduation were technically prepared for well-paying jobs. They were among the first wave hit during the recession and many went back to school to gain retraining or higher job skills in order to qualify for increasingly technical jobs.

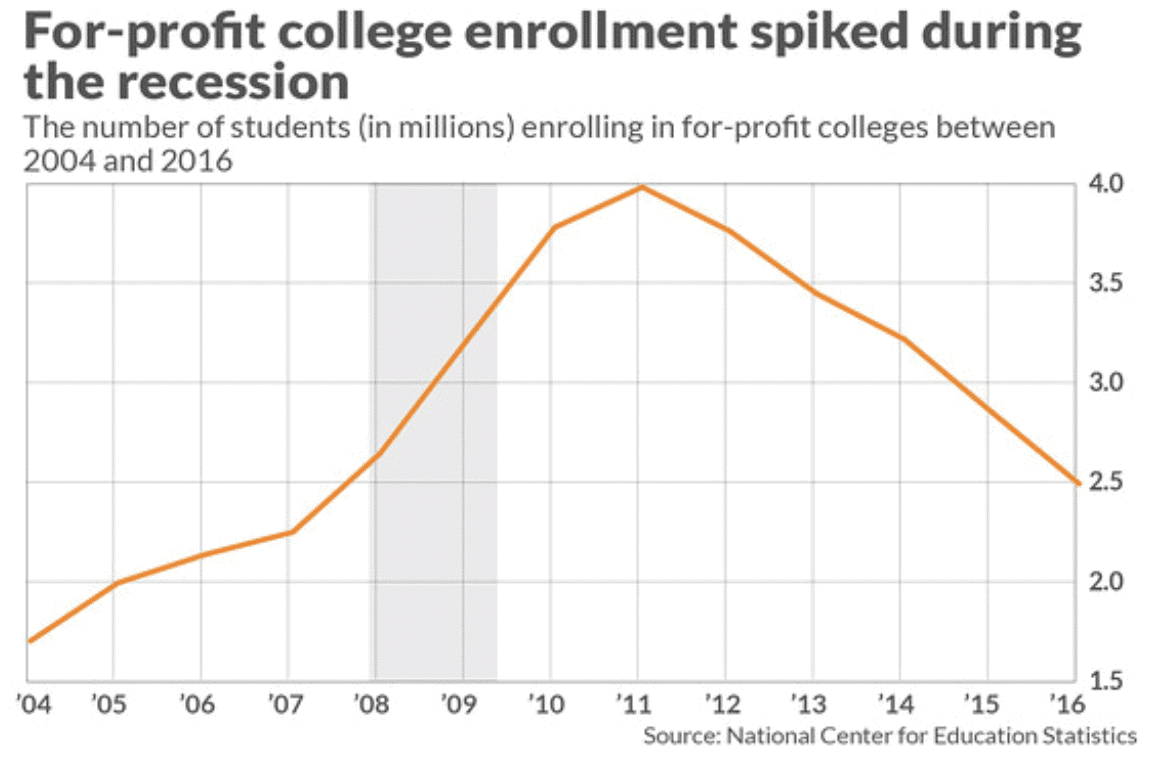

The Rise of For-Profit Universities: Funding cuts hit community colleges, the traditional choice for those seeking job training or advanced degrees in times of recession, but for-profit schools stepped in. For-profits tend to have comparably higher tuition than public universities but don’t produce correspondingly high salaries for graduates. The result was a double-whammy for students left with debt and no means to pay it off. The graph below, from the National Center for Education Statistics, illustrates the explosion in for-profit enrollment.

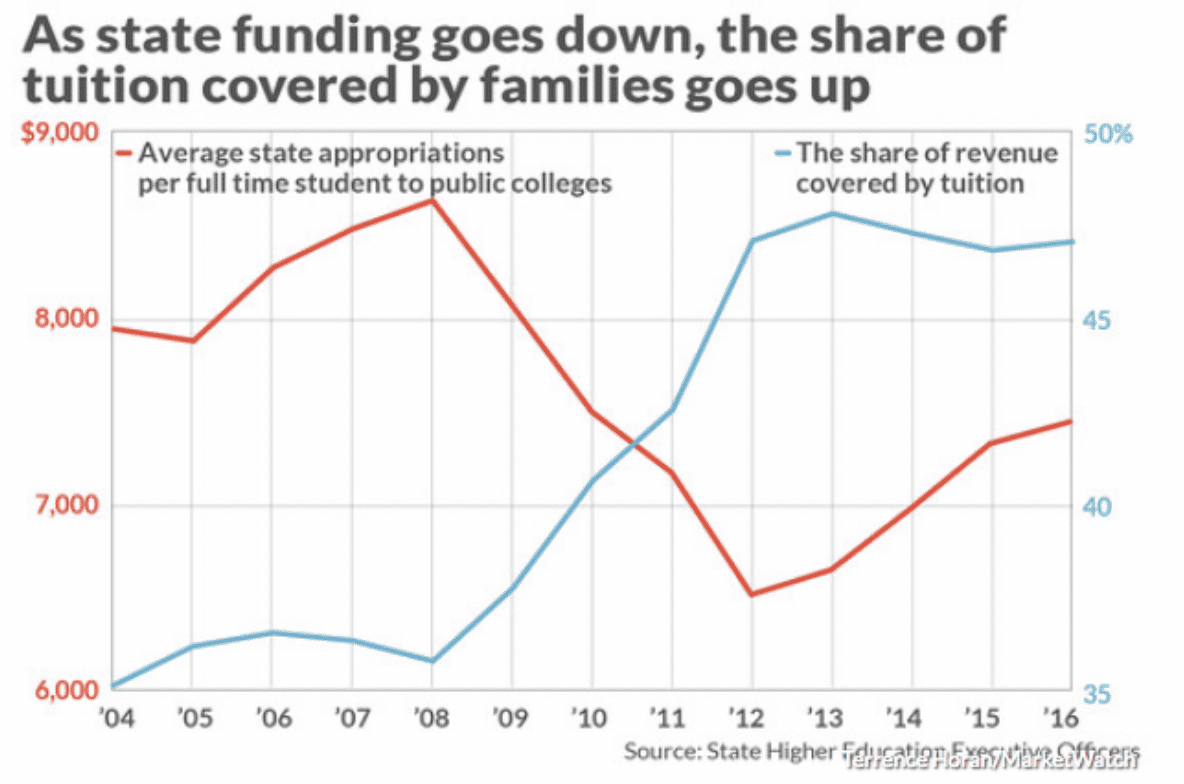

Tuition Inflation by Public Universities

One of the first cuts typically made by state governments in downturns is to public colleges and universities, with the result that tuition rises and a greater share of the burden falls on students and their families. Another chart from the National Center for Education Statistics graphically displays the correlation between the drop in government funding and how tuition increases cover shortfalls.

This all brings us back to the premise we started with: that, just as making home loans to buyers without sufficient credit or income precipitated the country’s 2008 economic collapse, the current student debt load is creating a situation ripe for another financial catastrophe. Similar to the housing situation, government-backed student loans are being made to individuals who may not ever have the careers that enable them to pay the loans back and thus are a poor risks for loans. Not surprisingly, those who leave school without completing their degrees struggle even more to pay back debt.

High student loan debt can affect someone through the course of their life, not just in their 20s. Delinquency or default leads to low credit ratings and inability to purchase homes. Clearly, a financial issue of this magnitude will require more than one solution. Certainly, tightening regulations on for-profit schools, a move that is already underway, is part of it, as is a move towards income-based repayment options.

In the future, these are fine solutions, but for those already saddled with debt, there are no quick fixes and an unexpected wave of loan defaults could create another recession of 2008 scale.

SOURCES: