In today’s post, we review a recent report from the CFPB (Consumer Financial Protection Bureau) about the state of credit card limits through the pandemic.

The CFPB’s uses its Consumer Credit Panel, which is a “de-identified sample of records from one of the three nationwide consumer reporting agencies.

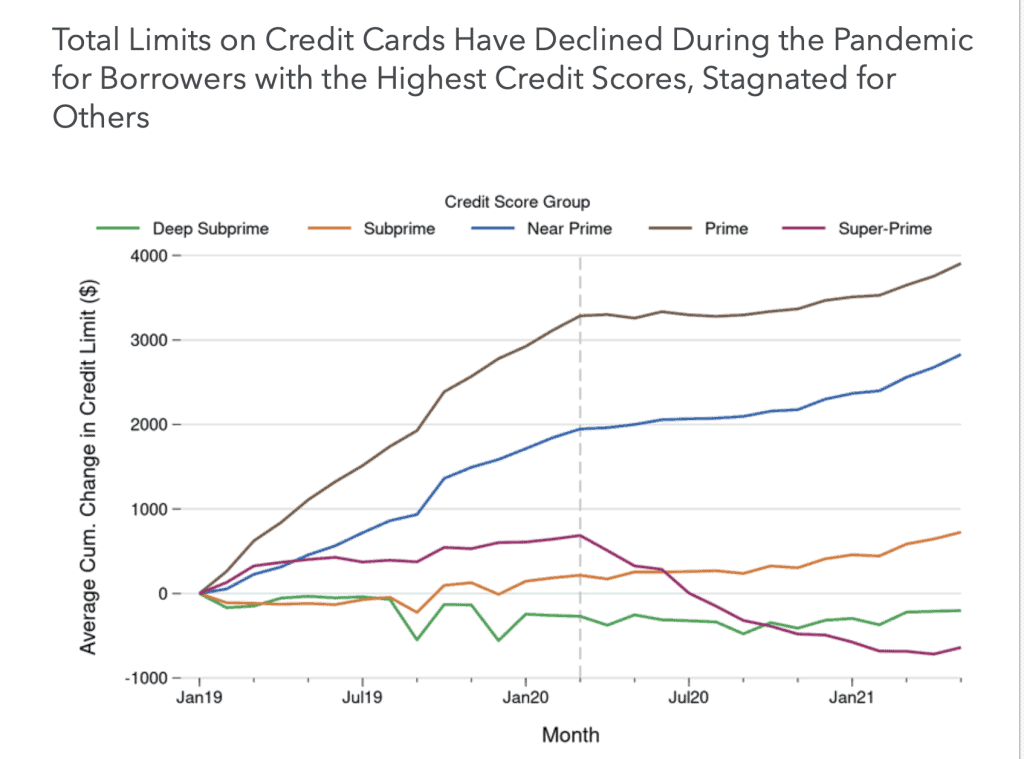

The first chart below dates back to December 2018 and looks at the average cumulative change in consumers’ total credit limits (for all accounts, both open and closed). Here’s what we see:

- After consistent and steep credit, credit limits leveled off for Prime and Near Prime borrowers in March 2020. But both groups saw a return to modest growth starting in February 2021.

- Super-prime borrowers were hardest hit by the pandemic, seeing dramatic declines starting in March 2020. As of May 2021, super-prime borrowers had about $640 less credit card credit available to them compared to December 2018. But compared to their peak credit limit just before March 2020, super-prime borrowers have $1,320 less today

- Subprime and deep subprime credit card borrowers saw little impact over the same period.

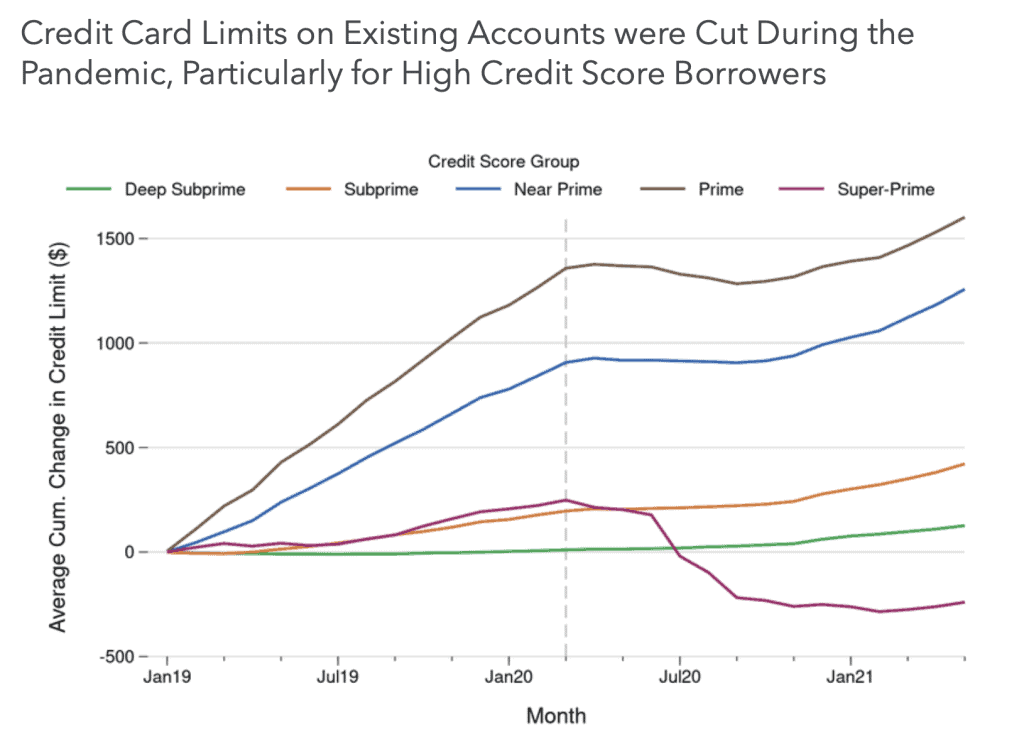

In the chart below, we look at the same credit score groups as in the previous analysis. However, the data here looks at credit card limits on existing accounts (not counting new or closed accounts.)

We see the same trends as shown above for “all accounts,” with:

- Near prime and Prime borrowers enjoyed significant growth in their existing credit card limits from December 2108, leading up to the early months of the pandemic. Both groups leveled off starting in March 2020, only to see a gradual upswing in limits as we move through 2021.

- There was little movement for Deep Subprime and Subprime borrowers over the past two years, although both groups see a gradual increase in credit limits on existing accounts as we move through 2021.

- Credit card limits on existing accounts were relatively flat for Super-Prime borrowers until the pandemic hit. Then these borrowers were hit by significant reductions in their existing credit card limits, a situation that is only now beginning to correct itself.

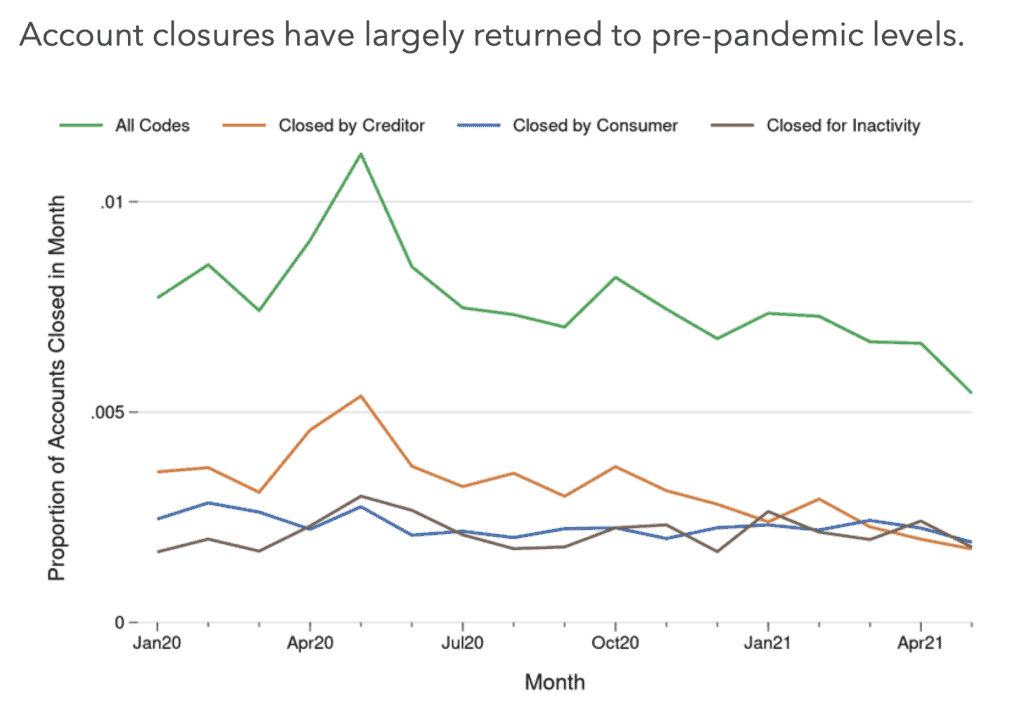

The final section of the CFPB’s report dealt with account closures.

Not surprisingly, as we see below, there was a tremendous spike in credit card account closures in the early months of the pandemic. The vast majority of these closures were initiated by consumers, more than double the amount undertaken by the creditors.

However, by the summer of 2020, closures fell to pre-pandemic levels, where they remained through May 2021.

It will be interesting to watch what happens to the economy if interest rates begin to creep up as the economy recovers. Higher interest rates might cause banks’ cost of lending to rise, which could lead to a slowdown in the growth rate of available revolving credit limits.

SOURCE

To learn more about Recovery Decision Science, contact:

Kacey Rask : Vice-President, Portfolio Servicing

[email protected] / 513.489.8877, ext. 261