We recently blogged about the impact the pandemic had on credit card limits. We saw that total limits on credit cards declined during the pandemic for those borrowers with the highest credit scores, while stagnating for others. We also looked at the role stimulus checks and forbearance played in helping borrowers pay down expensive revolving debt balances. Today, we revisit the credit card, looking at how credit access and usage continue to evolve as the country emerges from the pandemic.

CREDIT CARD BALANCE PATTERNS

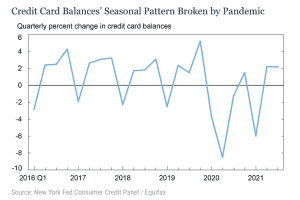

In general, credit card usage and related balance levels have historically followed a predictable pattern from year to year:

- Modest balance increases in Q2 & Q3.

- Sizeable increases in balances during the Q4 holiday buying season.

- Significant, post-holiday pay down in Q1.

As we can see in the chart below, the pandemic significantly impacted credit card usage and balances. As a result, compared to the predictable patterns of previous years, credit card balances went on a wild ride starting in Q2, 2020. Finally, we begin to see a return to standard seasonal patterns over the most recent two quarters.

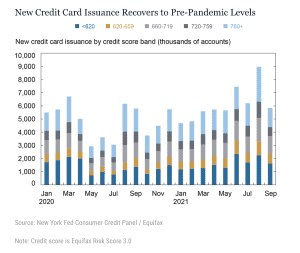

Next, we look at monthly credit card issuance, starting in January 2020 and running through September 2021. Finally, we look at newly issued credit card information broken out by borrowers’ credit card scores for this analysis. Here’s what we see from the chart below:

- There was a steep drop in card issuance during the early months of the pandemic, especially for sub-prime borrowers (credit scores below 620). The Federal Reserve’s Survey of Consumer Expectations cites a combination of factors leading to the drop: declines in demand for cards and more restricted access to credit.

- Issuance of credit cards rebounded to pre-pandemic levels in the fall of 2020.

- The sharp rise in card issuance starting in Q3 2020 reflected an increase in demand for credit as consumers began to satisfy their pent-up demand for goods and services. But, of course, this demand drove up balances significantly. As a result, the Fed saw that average balances across all accounts rose by $645 in the fall, 2020.

ACCOUNT CLOSURES

ACCOUNT CLOSURES

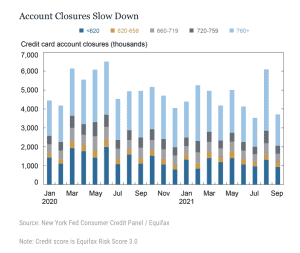

Finally, in the chart below, we see a temporary increase in credit card account closures in the early months of the pandemic. But by fall 2020, the rate of closure adjusted back to its pre-pandemic levels.  Overall, credit card balances have been impacted by several factors. Most notably, the dramatic swings in consumer consumption throughout 2020. Also, governmental cash infusions helped to tamp down the use of high-interest revolving credit accounts. Another aspect of the credit card story was that banks paused the issuance of new cards when the economic shutdown hit while taking steps to close many existing accounts as a strategy for minimizing risk.

Overall, credit card balances have been impacted by several factors. Most notably, the dramatic swings in consumer consumption throughout 2020. Also, governmental cash infusions helped to tamp down the use of high-interest revolving credit accounts. Another aspect of the credit card story was that banks paused the issuance of new cards when the economic shutdown hit while taking steps to close many existing accounts as a strategy for minimizing risk.

But as we can show above, after the understandable irregularities created because of the pandemic, we begin to see a return to regular credit card usage patterns as the economy rebounds.

SOURCE Andrew Haughwout, Donghoon Lee, Daniel Mangrum, Joelle Scally, and Wilbert van der Klaauw, “Credit Card Trends Begin to Normalize after Pandemic Paydown,” Federal Reserve Bank of New York Liberty Street Economics, November 9, 2021, https://libertystreeteconomics.newyorkfed.org/2021/11/credit-card-trends-begin-to-normalize-after-pandemic-paydown

To learn more about Recovery Decision Science’s Business Intelligence Team, contact:

Kacey Rask : Vice-President, Portfolio Servicing

[email protected] / 513.489.8877, ext. 261