As part of our ongoing coverage of issues related to the pandemic, we’ve taken deep dives into the role forbearance has played in stabilizing the economy since passage of the CARES Act. In fact, we just completed a four-part series on forbearance that included the following posts:

- How Forbearance Works

- Consumer Behaviors in Forbearance

- Forbearance and Small Business

- What’s Next for Those Coming out of Forbearance

Today, we study the forbearance story from a different angle. Working from a report by the Federal Reserve Bank of New York, we look at how various demographic groups benefitted across four different categories of forbearance: renters, mortgage holders, credit card holders and auto loan borrowers.

As a framework, the Fed published an extensive study in August, 2020, that looked at who participated in some type of forbearance, or deferment. Here’s what they found:

- 9.89 percent of renters received some level of relief, either through deferment, forgiveness or rental reduction.

- 5.5 percent of mortgage holders received forbearance.

- 13.6 percent of auto-loan holders received some level of assistance from their loan servicers.

- For credit card users, 11 percent of holders received assistance ranging from fee/interest reductions to credit limit increases.

Using these four categories, the Fed recently did a deep dive to determine the degree to which demographic characteristics (race, age, income, education) impact relief receipt.

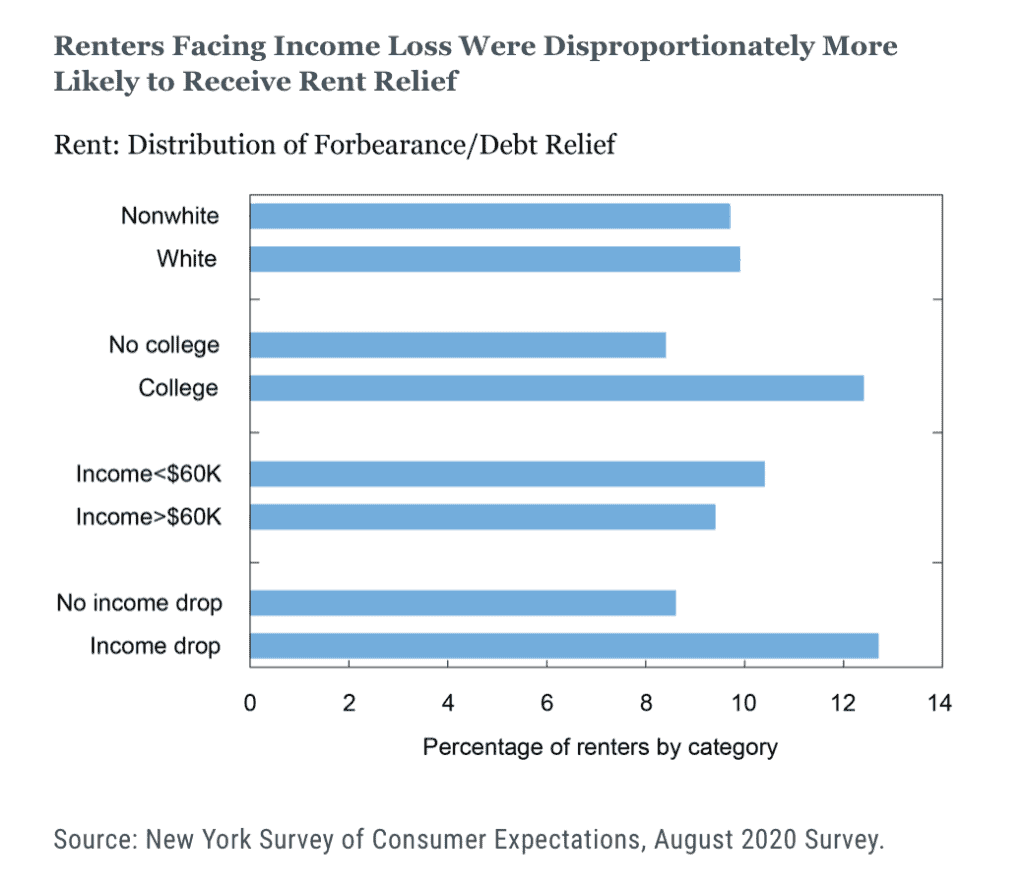

RENT RELIEF

As we’ve previously covered, mortgage forbearance was an important element of the CARES Act. However, CARES did not include provisions for rent relief. Still, rent relief was widely offered by landlords on a voluntary basis. However, landlords who received mortgage forbearance on their rental property were required to provide rent relief.

The chart below looks at the demographic breakdowns for the 9.8 percent of renters who received some level of relief:

Here is what we learn:

- Race did not play a notable role in who received rent relief, with 7.9 percent of whites and 7.7 percent of non-white renters, respectively, getting relief.

- 12.4 percent of college educated renters received rent relief, compared to 8.4 percent of noncollege renters.

- Low income renters were far more likely to receive relief than those in higher income brackets.

- Finally, with regard to income, those renters who experienced a drop in income were significantly more likely to receive rental relief.

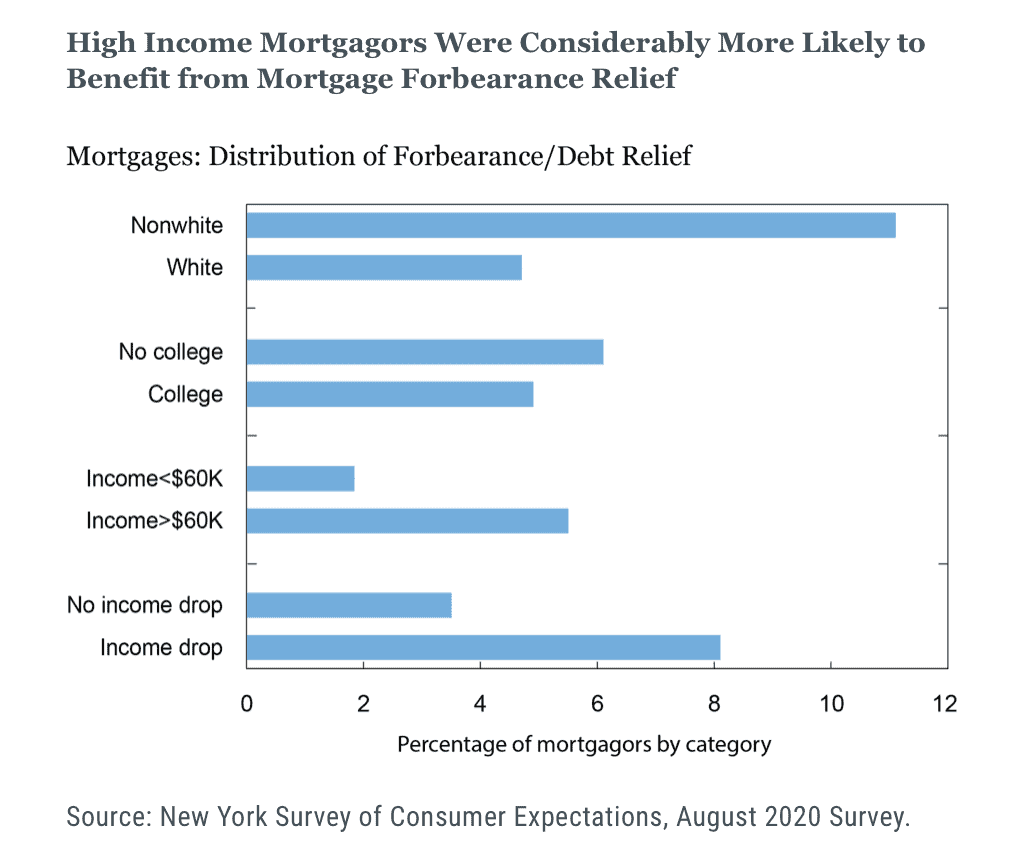

MORTGAGE RELIEF

The chart below breaks down mortgage relief for the 5.5 percent of mortgage holders receiving forbearance:

We see:

- Nonwhite mortgage holders were much more likely to receive relief than their white counterparts (11.1 percent vs. 4.7 percent, respectively).

- Noncollege educated mortgage holders were more likely to receive relief than college educated mortgage holders (6.1 percent vs. 4.9 percent).

- However, 8.1 percent of those who experienced a drop in income because of the pandemic received relief versus only 3.4 percent for those who did not have an income drop.

- High income mortgage holders were nearly three times more likely to received relief that lower income holders.

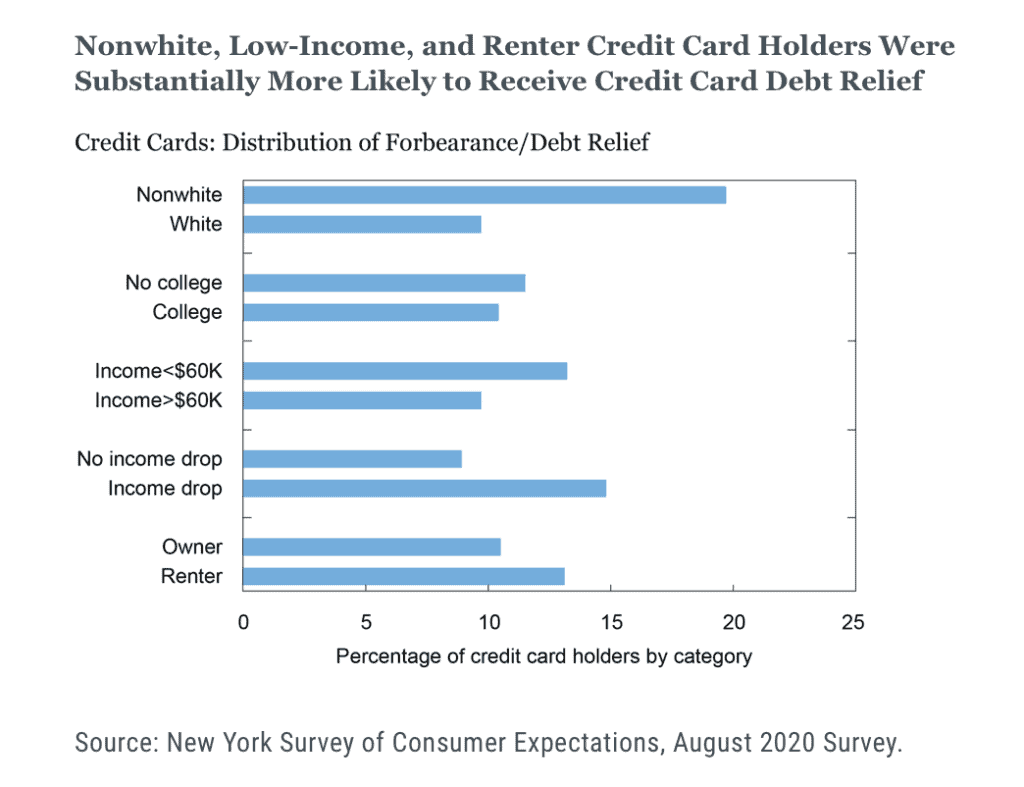

CREDIT CARD RELIEF

As with auto loan relief, credit card debt relief was offered by lenders on a voluntary basis.

The chart above on relief for the credit card holders reveals:

- Nonwhite credit card holders were twice as likely to receive relief than white holders (19.7 percent vs. 9.7 percent).

- Noncollege educated credit card holders were slightly more likely to receive relief (12 percent) compared to college educated card holders (10 percent).

- Income played a big role in credit card relief, as both lower income credit card holders, along with those who experienced income loss, benefitted from some form of relief.

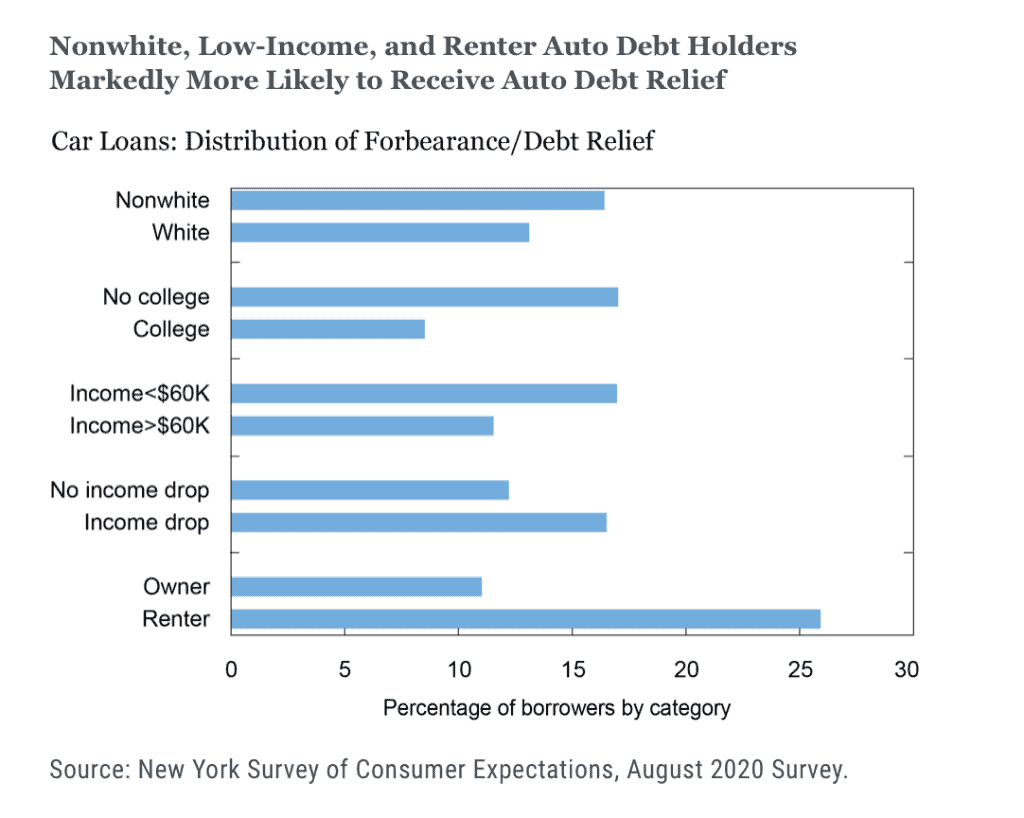

AUTO LOAN RELIEF

Finally, we look at the demographic characteristics of those received relief on auto loans:

The chart above shows us:

- As with credit card holders, nonwhite, less educated and lower income auto loan holders received considerably more relief than their demographic counterparts.

- Also, in an interesting cross-tab, renters holding auto loans were about 2 ½ times more likely to have received loan relief than homeowners with a car loan.

Beyond federal support through the CARES Act, it’s clear that voluntary loan relief played an important role in the economic recovery. Most importantly, as we see above, relief was generally more likely to benefit those demographic groups who were impacted the most by the pandemic.

SOURCE

https://libertystreeteconomics.newyorkfed.org/2021/08/who-received-forbearance-relief/

To learn more about Recovery Decision Science, contact:

Kacey Rask : Vice-President, Portfolio Servicing

[email protected] / 513.489.8877, ext. 261