This is the third in a four-part series on mortgage forbearance in the wake of the COVID-19 pandemic.

Several notable points from those first two posts include:

- About 7 percent of all mortgage holders entered forbearance by May, 2020. By March, 2021, the level of forbearance across all mortgage holders had declined to 4.2 percent.

- Not surprisingly, more than 10 percent of those living in the lowest-income neighborhoods (average income belonging in the lowest 25 percent) entered forbearance by May, 2020.

- Overall, the cash flow relief of forbearance was significantly higher for those in the highest–income zip codes, with a higher likelihood of home ownership and higher mortgage balances.

SMALL BUSINESS OWNERS ENTERING FORBEARANCE

As has been widely reported, in this blog and elsewhere, the pandemic was devastating to U.S. small businesses, especially within certain business sectors.

Recovery Decision Science’s Tableau Public page, ECONOMETRIX, began tracking (and continues to track) a variety of data sets related to U.S. unemployment. We showed that sectors like food service saw unemployment levels hover above 40 percent in the early stages of the pandemic.

It’s not surprising then that many small businesses took advantage of cash flow opportunities afforded through the mortgage forbearance aspects of the CARES Act. Let’s first look at a demographic snapshot of small business owners, who, compared to the general population, tend to:

- Be slightly older

- Have higher credit scores

- Have a wider variety of credit-related products

- Live in wealthier neighborhoods

- Maintain higher balances on financial accounts

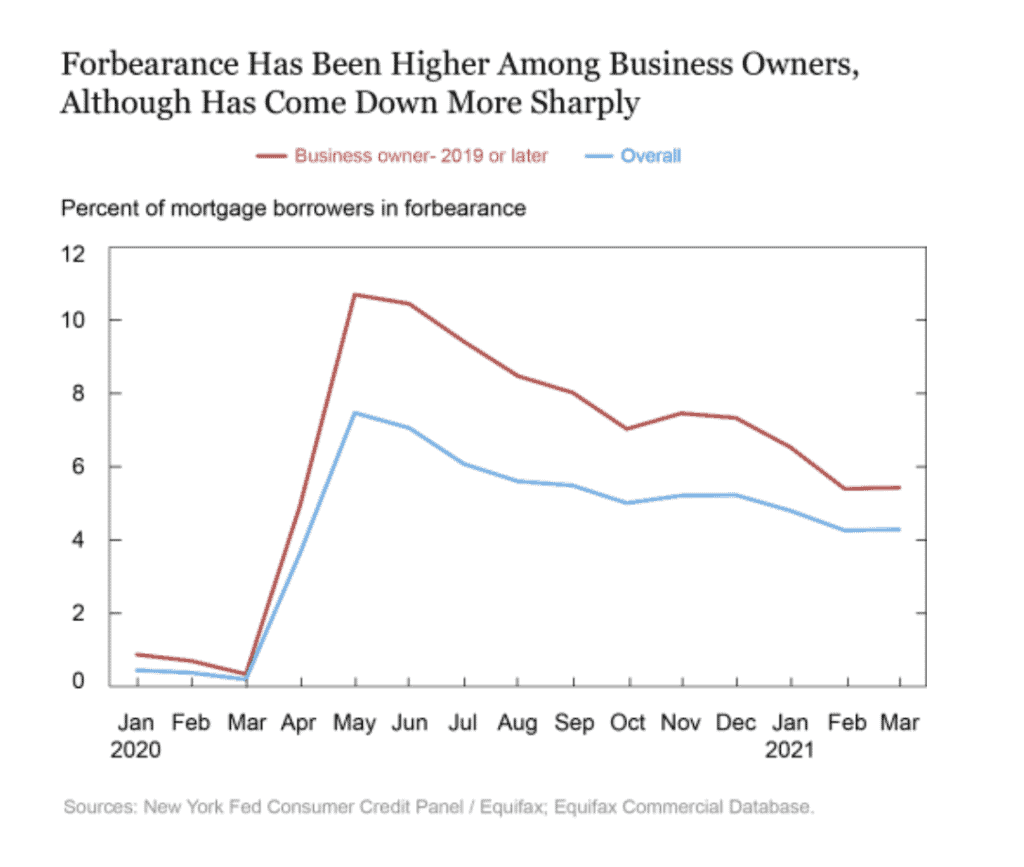

With regard to forbearance, a significantly higher number of small business owners entered forbearance in the early month of the pandemic compared to the general population. Specifically, as we see in the chart below, 11 percent of small business owners entered forbearance, compared to 7 percent of the general population. But participation in forbearance declined dramatically for small business owners and stood at 5 percent in March, 2021, compared to 4.2 percent for the general population.

Over the period from February, 2020, through March, 2021, more than 17 percent of small business owners participated in forbearance programs.

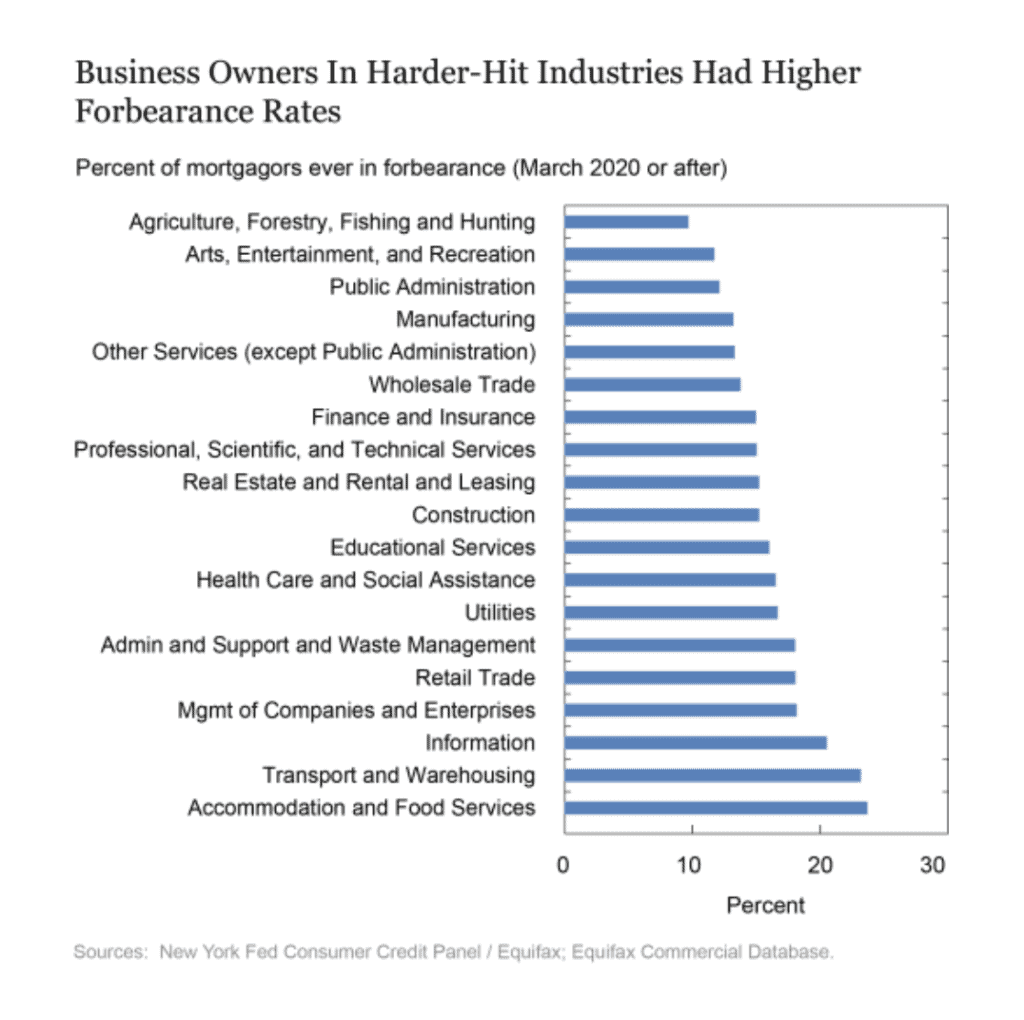

While 11 percent of small business owners entered forbearance, the levels vary dramatically depending on the specific industry. The chart below looks at forbearance levels by industry. Not surprisingly, the hardest hit sectors saw heavy participation in forbearance program. Most notably, 23 percent of those business owners in the food service and accommodation sectors entered forbearance. This compares to level of about 10 percent in agriculture.

WHAT ABOUT PERSONAL CREDIT?

In addition to taking advantage of the cash flow benefits of mortgage forbearance, small business owners leaned heavily on their personal lines of credit.

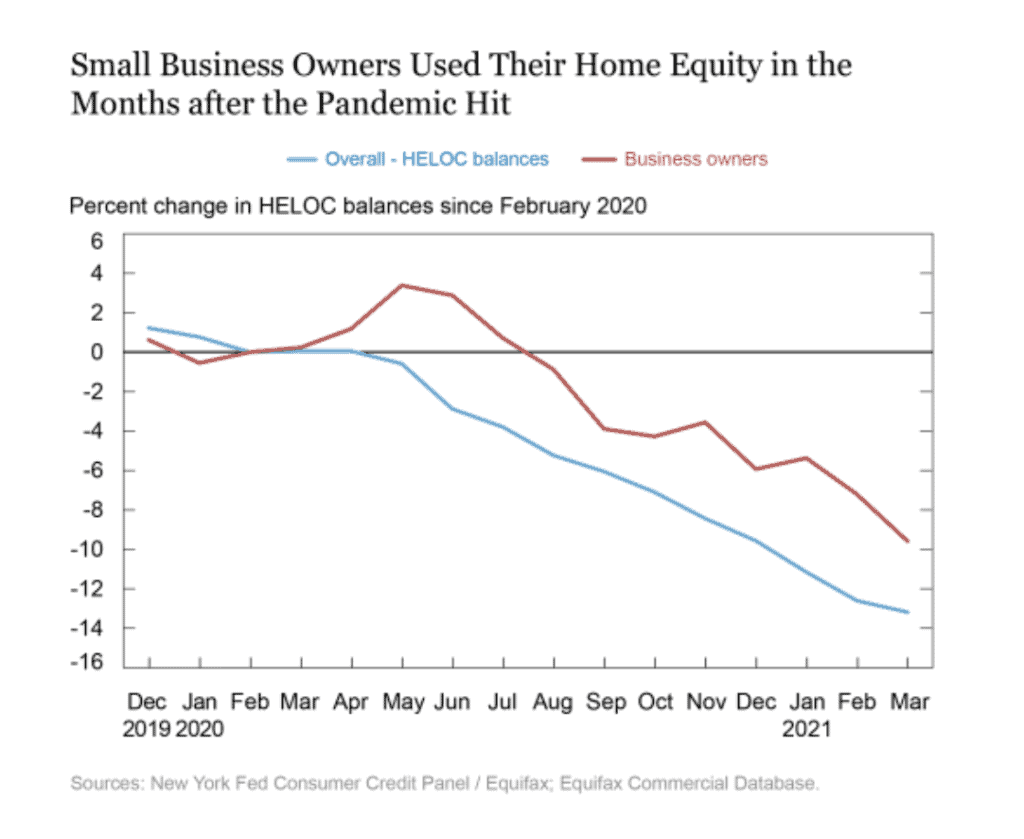

In particular, small business owners borrowed heavily against the equity in their homes, as seen below. In general, since the Great Recession, Home Equity Line of Credit (HELOC) balances have been in decline. But you’ll see that, for small business owners, there was a significant increase in HELOC balances in the early stages of the pandemic. Between February and May, 2020, HELOC balances for small business owners grew by 3.4 percent, compared to a drop of 0.6 percent for the general population. And, as you’ll see, while small business owners began to pay down their HELOC balances, they are still paying down at a slower rate than the general population in March, 2021.

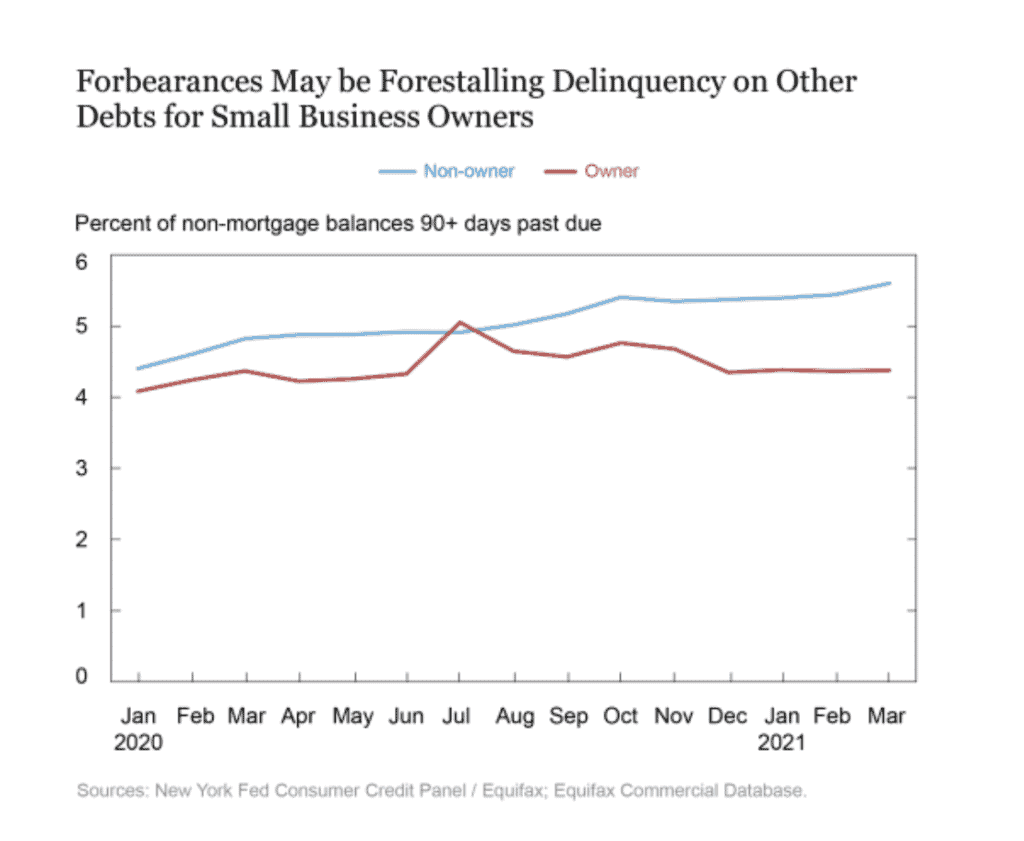

Finally, we look at non-mortgage debt in the chart below. It suggests that mortgage forbearance may be forestalling non-mortgage debt for small business owners. The blue line shows a steady increase in non-mortgage debt for non-business owners since January, 2020. By contrast, non-mortgage debt is remained relatively stable during the same period, other than a slight uptick in the summer of 2020.

SOURCE

Andrew F. Haughwout, Donghoon Lee, Joelle Scally, and Wilbert van der Klaauw, “Small Business Owners Turn to Personal Credit,” Federal Reserve Bank of New York Liberty Street Economics, May, 19, 2021, https://libertystreeteconomics.newyorkfed.org/2021/05/small-business-owners-turn-to-personal-credit-.html.

To learn more about Recovery Decision Science, contact:

Kacey Rask : Vice-President, Portfolio Servicing

[email protected] / 513.489.8877, ext. 261