In last week’s post, we reviewed the Federal Reserve’s recent report on CREDIT ACCESS AND DEBT PAYMENT in the post-pandemic economy. The report covered credit and debt holding, delinquencies, and balances in collection for the major credit product categories: mortgages, credit card, auto loans and student loans.

Of these four categories, how to handle the burgeoning level of student loan debt has garnered the most attention from pundits and politicians alike. Which might explain why the Fed is embarking on a series of reports covering the student debt story.

In today’s post, we take a deep dive into student loan repayment during pandemic forbearance.

OVERVIEW

About 37 million borrowers of Direct federal student loans did not have to make loan payments starting in March, 2020. This translates to an estimated $195 billion in waived payments running through April, 2022.

On the flipside, more than 10 million borrowers who held private or FFEL (Family Federated Education Loan) loans, continued making payments during the pandemic. (NOTE: FFEL loans are broken out into those held by the Federal government or commercial banks).

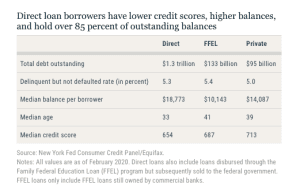

This post looks at how each of these loan-holding groups fared prior to and during the pandemic. For perspective, let’s look at the debt/credit profile of each group, in the chart below.

As you can see, Direct student loan borrowers have lower credit scores, higher balances and about 85% of total, outstanding student loan balances.

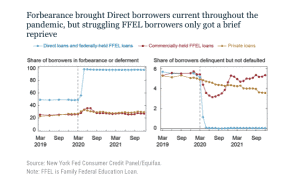

FORBEARANCE AND DELINQUENCY DURING THE PANDEMIC

The chart below walks us through the state of borrowers in forbearance/deferment, as well as the level of delinquencies (not defaults). Here’s what we see:

- In the year leading up to the pandemic, the share of borrowers in forbearance remined consistent across all groups. Note that the forbearance rate for Direct loans is about double that of FFEL and private loans. This is primarily a function of in-school deferments, a type of deferment that allows the borrower to temporarily pause payments while attending college.

- In the early stages of the pandemic, forbearance rose across all borrowing groups, with Direct loans rising to near 100% administrative forbearance.

- We then see that previously-marked delinquent loans (grid to the right) were immediately marked current for Direct borrowers.

- Many previously delinquent FFEL loans were also marked current, which drove the FFEL delinquency rate to 3.2%, from 5.4%. Because voluntary forbearance lasted on a few months, FFEL delinquencies rose through the remainder of 2020, dropping slightly in March, 2021 when the federal government issued a new round of stimulus checks.

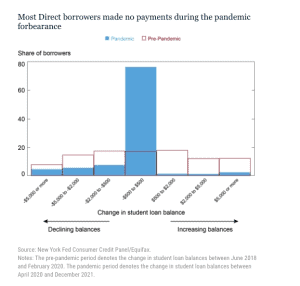

HOW STUDENT LOAN BALANCES EVOLVED DURING THE PANDEMIC

Next, the Fed’s report looked at the evolution of borrowers’ balance before and during the pandemic. The three charts below outline two metrics:

- BLUE BAR: Changes in balances during the pandemic-April 2020 through December 2021.

- RED BAR: Changes between June 2018 and February 2020.

Let’s start with Direct borrowers:

- Prior to the pandemic, there was nearly an even split between borrowers who were making progress (40% with decreasing balances) and those with increasing balances (43%).

- The share of borrowers with increasing balances dropped to nearly zero during the pandemic thanks to administrative forbearance, and the temporary 0% interest rates.

- Of the borrowers who had increasing balances pre-pandemic, 83% had no change in their balance during the pandemic forbearance period. However, 9% did make some progress.

- Borrowers with declining balances pre-pandemic were more likely to continue with declining balances during the pandemic.

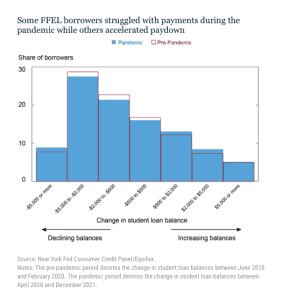

Next, we look at FFEL borrowers:

- Prior to the pandemic a higher share of FFEL borrowers showed declining balances (59%) compared to Direct borrowers (40%).

- In general, FFEL borrowers tend to be older and hold higher credit scores. This might explain why they tend NOT to show increasing balances over time. In fact, FFEL borrowers did not change their paydown habits during the pandemic.

- About 1% of FFEL borrowers actually accelerated their rate of paydown during the pandemic. On the flipside, 2% grew their balances during the pandemic.

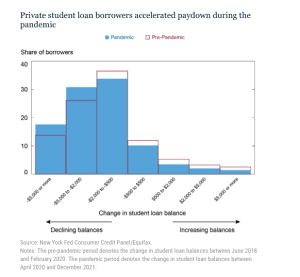

Finally, we look at private student loan borrowers, and find:

- This group of borrowers accelerated paydown during the pandemic, compared to the 20 month period leading up to the pandemic.

- Private borrowers tended to make larger balance reductions during the pandemic. For example, 49% of private loan borrowers paid down their balances by at least $2,000.

Moving forward, the question is: how will Direct borrowers fare now we’re reaching the end of forbearance programs. We know that Direct borrowers have higher balances, lower credit scores and made less progress in paying down their balances during the pandemic.

Various policy proposals have been put forth. These include not reporting missed payments to the credit bureaus, or possibly cancelling student loan debt outright. As of now, these ideas are the subject of much debate, but little action. To that end, the Fed will continue to explore the issue of student loan debt in future reports.

SOURCE

Jacob Goss, Daniel Mangrum, and Joelle Scally, “Student Loan Repayment during the Pandemic Forbearance,” Federal Reserve Bank of New York Liberty Street Economics, March 22, 2022, https://libertystreeteconomics.newyorkfed.org/student-loan-repayment-during-the-pandemic-forbearance

To learn more about Recovery Decision Science contact:

Kacey Rask : Vice-President, Portfolio Servicing

[email protected] / 513.489.8877, ext. 261