With household debt again increasing in third quarter 2018 for the 17th consecutive quarter, the New York Federal Reserve Bank’s Quarterly Report on Household Debt and Credit recently took a look at debt and bankruptcy patterns by age demographic.

Based on the New York Fed Consumer Credit Panel (CCP) and a 5% sample of anonymized Equifax credit reports, the Fed report provides no big surprises. Debt and bankruptcy rates have risen among consumers 65 and older but remains lower than other age groups, with the rise logically assumed to be due to their increasing share of the population as the Baby Boom generation hits retirement age.

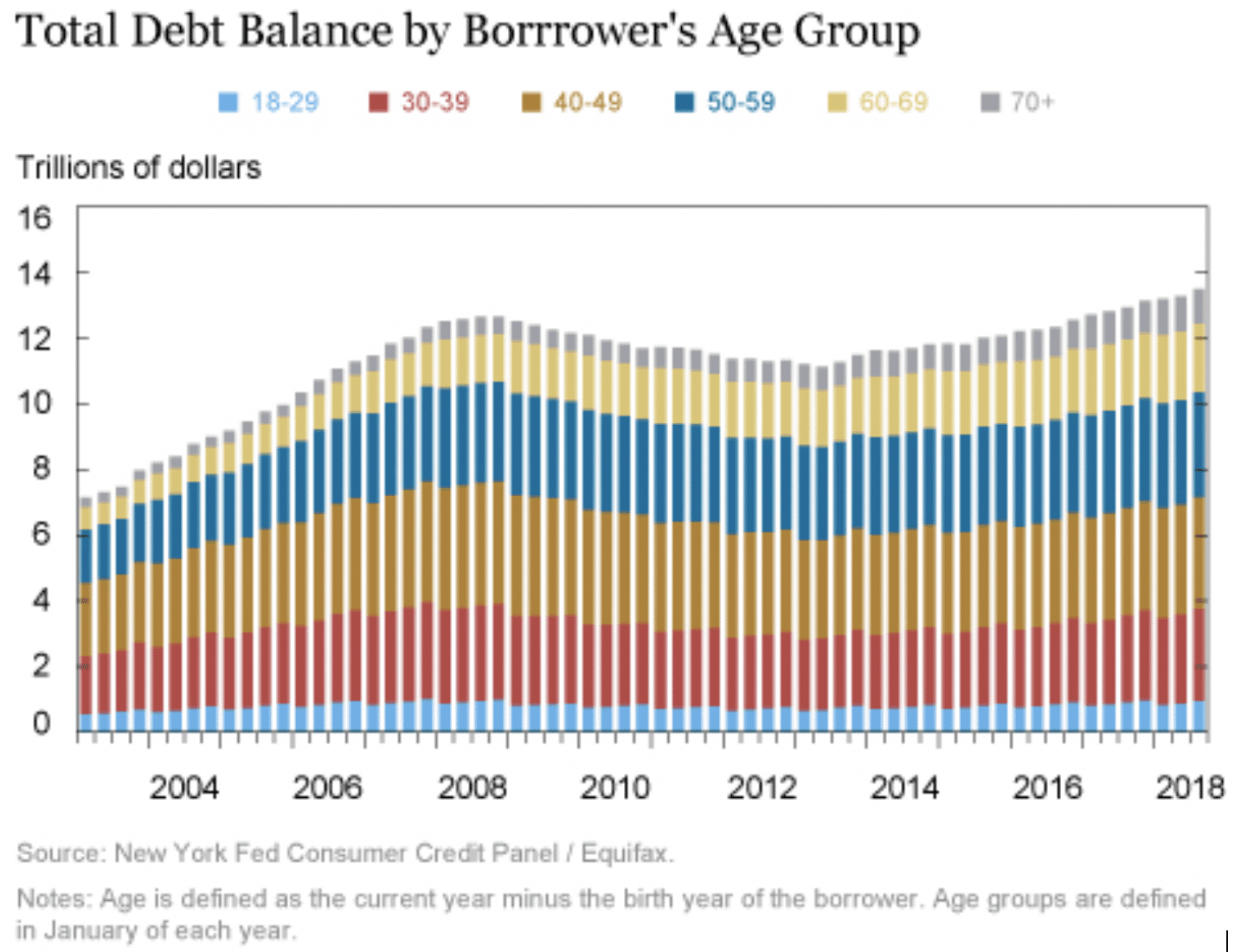

In 2016, the Fed found debt among people ages 50-80 increased more than 60 percent in the period 2003-2015. That trend continues due to shifts in lending practices and credit demand, in addition to the aforementioned aging Baby Boomers. Mortgage lending practices have tightened while credit card issuance and auto loans have become more prevalent. The combined factors contribute to the overall increase in debt balances held by people over the age of 50. Not surprisingly based on prior reports, the majority of debt for people under 30 is comprised of student and auto loan debt. For borrowers over the age of 60, housing debt makes up the majority of debt held. The chart below demonstrates debt levels based on age cohort.

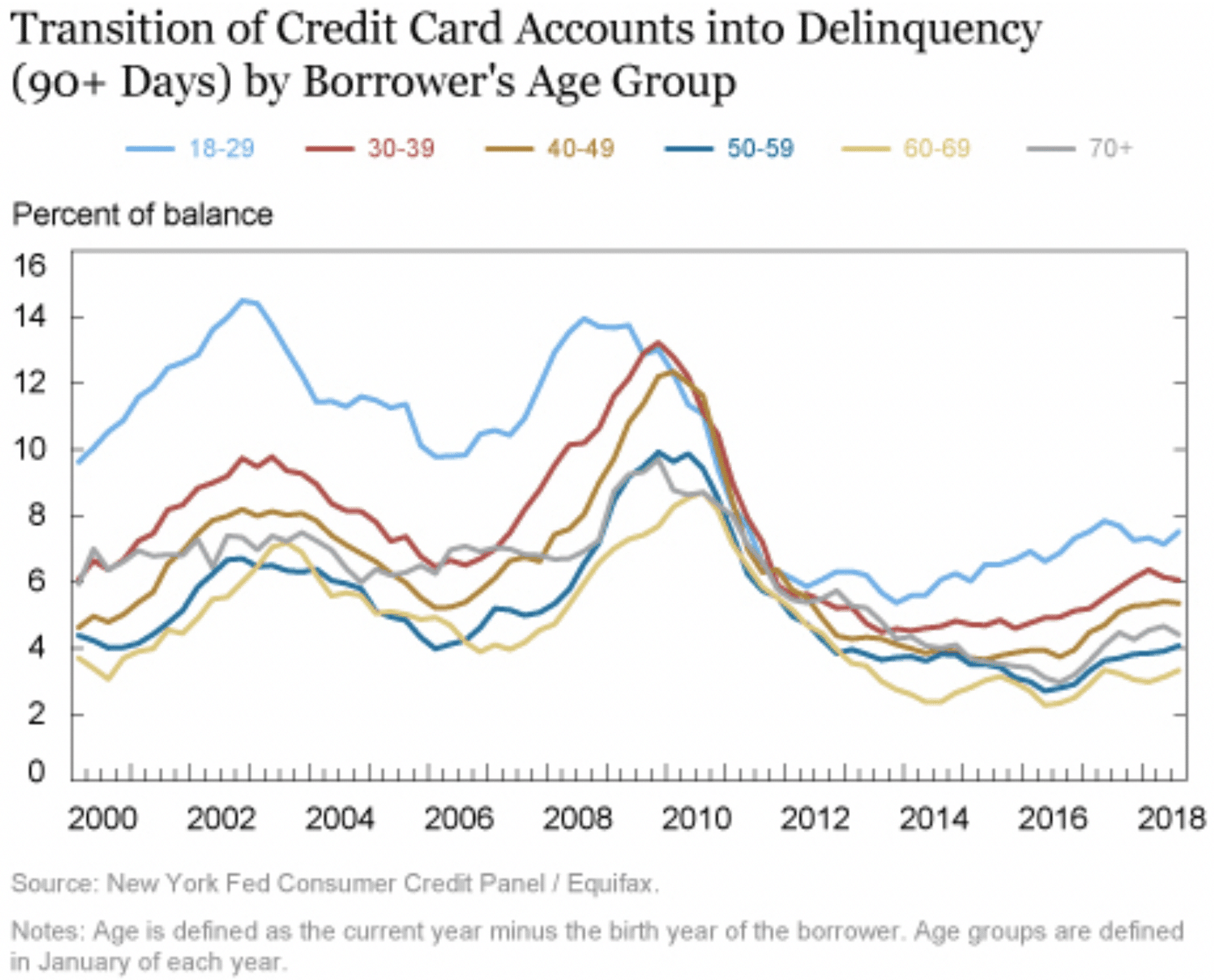

The report also reviews debt balance by age group. Again, it’s no surprise to find the youngest group of borrowers (18-29) is more likely to become seriously delinquent on credit payments – defined as more than 90 days overdue – although fewer young consumers are delinquent than prior to the Great Recession. This largely can be attributed to the Credit Card Act of 2009, which made procuring credit cards tougher for younger borrowers, resulting in a lower rate of delinquency. However, it is worth noting, as seen in the chart below, that delinquency rates have begun to rise again among all age groups in the last three years.

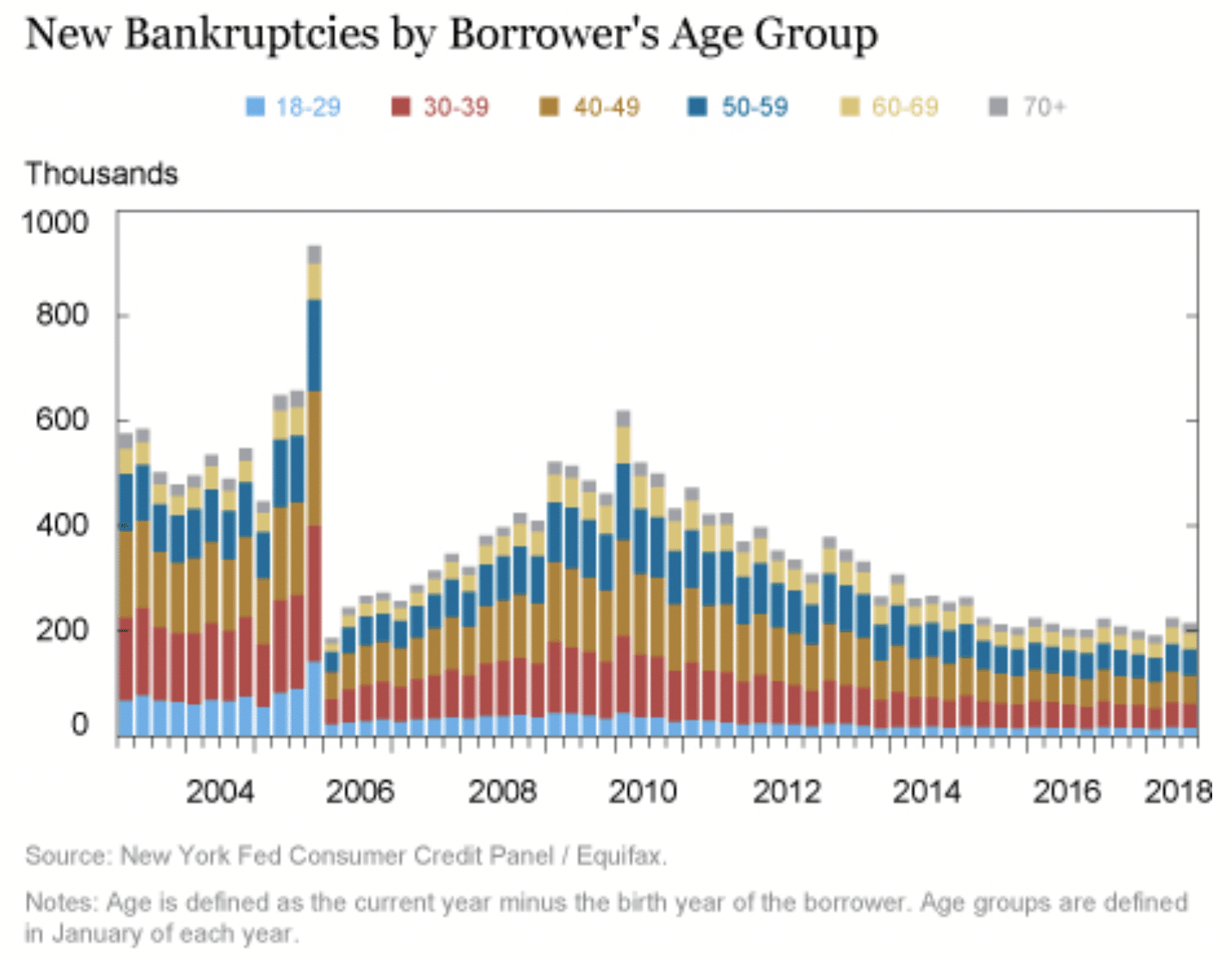

In the final component of the report, the Fed examines bankruptcy rates by age. Bankruptcy, like credit delinquencies, skews to younger age cohorts with the majority of bankruptcies in the 30-49 cohort.

The chart below graphically demonstrates the sharp decline in bankruptcy among young borrowers following the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005, which made filing for Chapter 7 bankruptcy more difficult. As we noted in our opening, bankruptcy filings among Americans 65 and older have risen as the “leading edge” Baby Boomers, or those born between 1946-1955, deal with more out-of-pocket healthcare costs and declining incomes, whether those individuals are still in the workforce or in retirement. That age cohort alone accounts for more than half the total Baby Boom generation, or approximately 38 million people.

Even with bankruptcies among older Americans on the uptick, there still appears to be no cause for concern. There was a bump in bankruptcies for all age groups in 2010, coming off the height of the Great Recession, but bankruptcies have again tapered off.

Having said that, the next cohort of Baby Boomers, the Late Boomers, or those born between 1956-1964, will turn 55 in the coming year. As American’s largest generation continues to reach retirement age, it’s likely we will see a corresponding increase in debt and bankruptcies.

SOURCE