Another year draws to a close and there’s no better time to assess how Americans are feeling about their economic well-being.

To do so, we will examine over the next few weeks the fifth annual Survey of Household Economics and

Decision making (SHED), conducted by the Federal Reserve Board’s Division of Consumer and Community Affairs (DCCA) from May 2017-May 2018.

The report analyzes how adults in the U.S. are faring financially, providing insights on overall economic well -being, employment, housing, retirement savings, banking and credit, student loans, dealing with unexpected expenses and, for the first time, an examination of how the national crisis of opioid drugs is affecting Americans. More than 12,000 people drawn from low and moderate-income populations were sampled in an attempt to gain new information on the groups’ financial challenges.

In the first installment of our analysis, we review perceptions of economic well-being by educational level and racial and ethnic status.

Improvement since the Great Recession continues, and more people generally feel better about their financial standings than in the past four reports, but pockets of fragility and distress remain, particularly in minority groups and those people with lower educational attainment.

More than three-quarters of the sample reported they were either living comfortably or doing okay in 2017 – 33 percent for the former and 44 percent for the latter. The share of those who report managing ‘okay’ has risen since the study’s inception in 2013 by 10 percent.

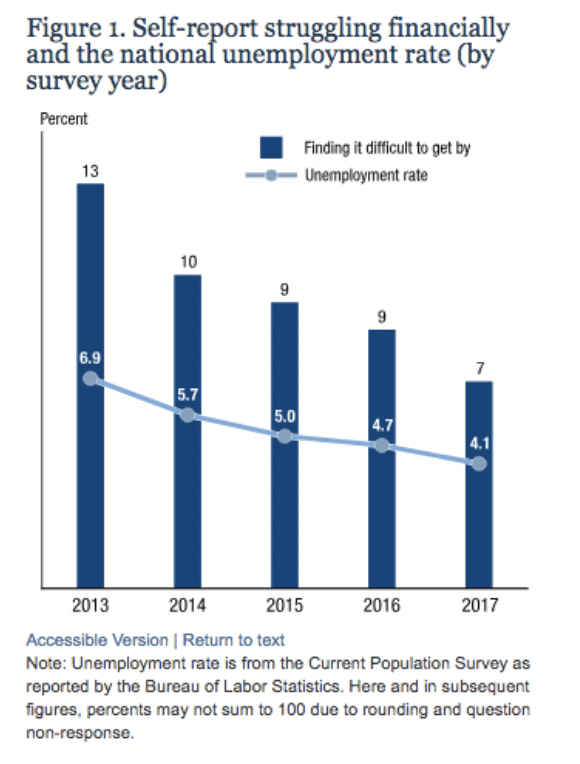

The decline in the national unemployment rate over the last five years also correlates with a decrease in the number of respondents reporting they struggle financially, as is illustrated in the graph below.

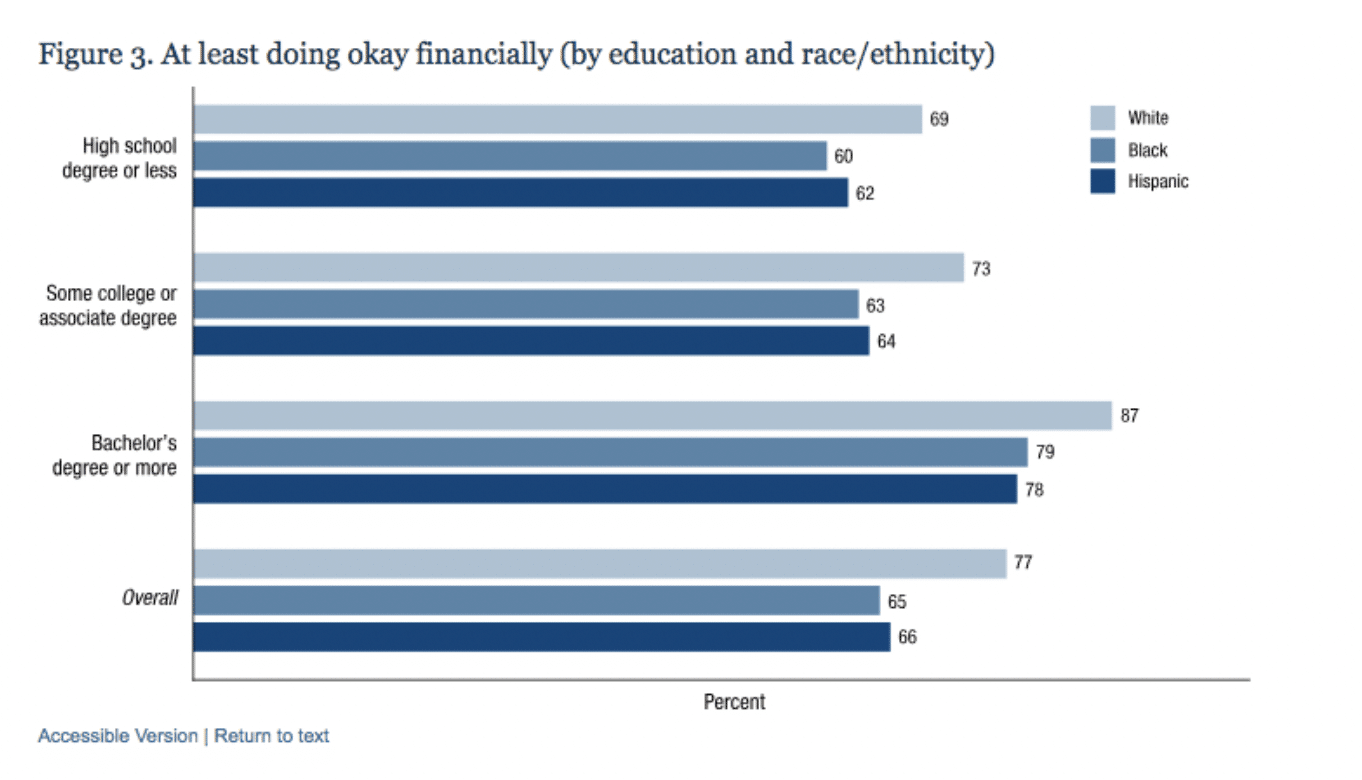

We were not surprised by one of the key takeaways from the report: while people of all education levels report financial improvements, education still correlates with financial stability.

However, blacks and Hispanics remain financially worse off than whites at every educational level. As the figure below demonstrates, whites who only have a high school degree often report they are in better financial condition than members of other ethnic groups that possess some college education or an associate degree.

Given that members of Hispanic and black populations generally have completed less education, a clear pattern emerges that those groups have been substantially less financially sound than whites. More than three-fourths of whites report doing ‘okay’ financially while less than two-thirds of the other two groups report similar results.

The trend continues when individuals were asked if their financial situation improved in the year prior to the survey.

Despite a larger share reporting improving financial situations in 2017, again, those with less education showed smaller gains than those with higher educational levels. At each educational level, blacks and Hispanics reported similar rates of improvements as whites, a contrast to prior years when the gap narrowed as racial and ethnic minorities reported larger improvements than whites.

In the next installment, we will examine the effect of opioids on financial well-being and take a look at housing issues.

SOURCE