Americans now owe more than $1.6 trillion in student loan debt that is increasingly becoming a burden for people of all ages.

According to the American Association of Retired Persons (AARP), those ages 50 and older account for 20 percent of the debt, an approximate $289 billion.

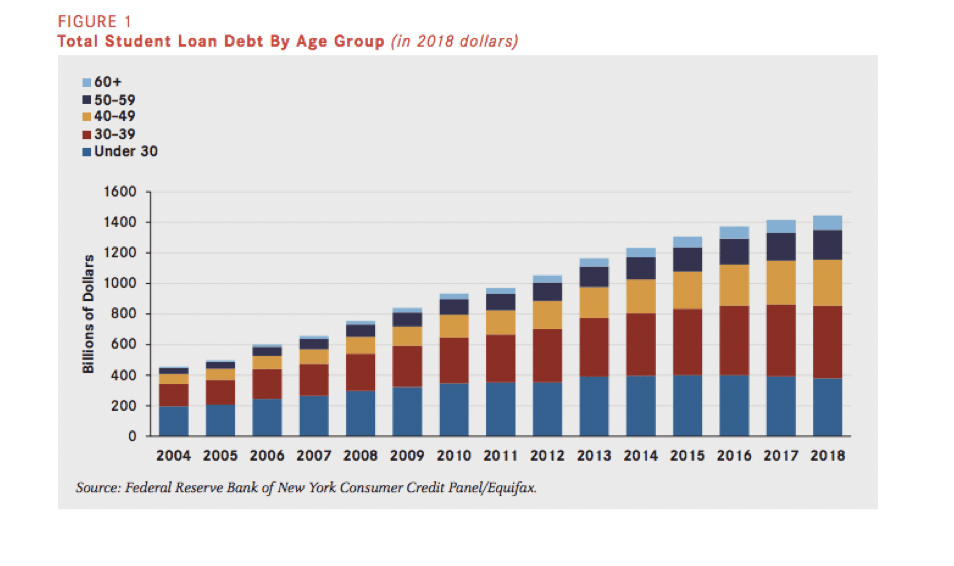

The overall increase reflects a sharp rise in both the number of families borrowing and the amounts they borrow, as demonstrated in the chart below. Historically, people tended to incur debt at younger ages – to pay for their college education and buy homes — and then paid the debt off during their working years. This enabled them to enter retirement debt-free and gave them a better chance of obtaining and retaining financial security as they aged.

Over the past three decades, however, the life cycle of debt has changed dramatically. The cost of attending college has increased substantially during this period, with the average cost of a four-year higher educational institution more than doubling on an inflation-adjusted basis. Meanwhile, nationally, state and local funding per student for higher education has decreased.

In addition, family incomes have not increased enough to keep pace with inflation, much less the increase in college costs. As a result, more students are taking on greater amounts of student loan debt than in the past. This creates a large repayment burden, which squeezes budgets of young families and, in many cases, impedes and delays their ability to save for a home or for other purposes such as retirement. Over the life course, families have more student loan debt at younger ages and carry the debt with them for longer periods.

The increased debt burden reaches beyond the young adult who takes out a student loan. In many families, parents, grandparents, and other relatives are taking on debt to help finance a family member’s education. This includes taking out loans directly or cosigning loans for students who cannot qualify on their own. Given that cosigners are responsible for making loan payments when the borrower fails to do so, a seemingly simple secondary signature can ultimately create financial hardship for an older cosigner who never expected to be saddled with such payments. Compounding the problem is that many older borrowers in or near retirement often face their own debt burdens, most often from a mortgage or credit cards.

The increase in student loan debt today is an intergenerational problem, burdening borrowers of all ages and threatening the long-term financial security of millions of families.

Notably, millennials and generation Xers also said their student loan debt has prevented or delayed their ability to save for their children’s education. This inability to save increases the likelihood they will need to borrow when the time comes for their children to attend college, thus perpetuating the intergenerational student loan debt cycle.

In our next post, we will take a look at data from the Federal Reserve Bank of New York and the AARP Public Policy Institute to analyze the impact of student loan debt on older adults.

SOURCES