In a recent post, we discussed the Consumer Financial Protection Bureau’s 2018 Fair Lending Report to Congress.

Among the topics presented by the agency, which regulates the offering and provision of consumer financial products, was an examination of the geography of credit invisibility and credit deserts. To learn more about credit invisibility, check out this EARLIER POST.

First, let’s define the term ‘credit deserts.’ The term is frequently used to describe geographic areas with limited access to traditional financial service providers and, often, with easy access to alternative ones, such as payday lenders or pawnshops.

While low credit usage may be correlated with restricted credit access, the two concepts are not equivalent: Areas with high incidence of credit invisibility don’t necessarily constitute a credit desert.

For instance, areas around college campuses often show a high level of credit invisibility but shouldn’t necessarily be considered a desert. While consumers younger than 25 make up a disproportionate share of credit invisibles, credit invisibility appears to be less of a barrier to credit access for these consumers.

The vast majority of consumers do not have a credit record when they are 18, but the incidence of credit invisibility among those ages 25-29 is less than nine percent. This suggests that over 90 percent of consumers transition out of credit invisibility by their mid-to-late 20s.

Thus, the CFPB has focused on credit invisibility among people aged 25 and older. By excluding the young, for whom credit invisibility appears to be predominantly transitory, this metric should better identify those geographic areas where credit access might be more limited.

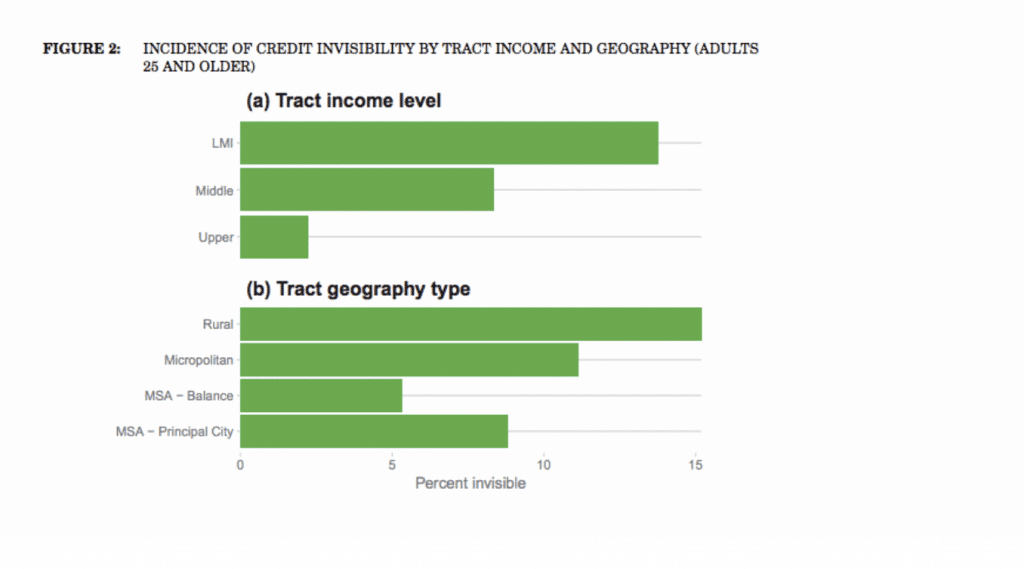

The CFPB has previously shown the incidence of credit invisibility is significantly higher in lower-income neighborhoods. In particular, almost 30 percent of adults in low-income U.S. Census tracts were credit invisible, a rate about 8 times higher than that in upper-income census tracts.

While the CFPB has found neighborhood income level is closely related to the incidence of credit invisibility, other geographic characteristics appear related as well. One of these is whether the neighborhood is more of an urban area.

The CFPB assigned each area a geographic category based upon whether it was within a Core Based Statistical Area (CBSA) as defined by the Office of Management and Budget. Tracts located within Metropolitan Statistical Areas (MSA) were categorized based on whether the tract was part of the MSA’s principal city (MSA – Principal City) or outside of it, which is called the balance area (MSA – Balance). The remaining tracts were categorized as “Micropolitan” if they are within a Micropolitan Statistical Area or “Rural” otherwise. The chart below demonstrates the incident of credit invisibility by each area.

Rural areas have the highest incidence of credit invisibility among the four geographic areas. Credit invisibility does not invariably decrease with urbanization, as more urban principal cities have a higher percentage of adults 25 and older who are credit invisible than the more suburban balance areas of the MSAs.

Within MSAs, there is a strong relationship between neighborhood income and the incidence of credit invisibility. Low-to-moderate income (LMI) neighborhoods have higher concentrations of credit-invisible adults 25 and older

By contrast, the relationship between income and credit invisibility is much weaker in rural areas, where credit invisibility is higher even if the tract’s relative income level is higher. Specifically, upper-income tracts in rural areas have concentrations of credit invisibility that are comparable to those of LMI tracts in the principal cities of MSAs and higher than those of all tracts in micropolitan areas or suburban areas of MSA

In our next post, we will explore other aspects of credit invisibility by geography, including entry products and the proximity of financial institutions.

SOURCE