There is no question that the American economy has been, in large part, fueled by the average person’s easy access to consumer credit. The flip-side, of course, is that many Americans are unable to meet their debt obligations, leaving them vulnerable and often unable to fully participate in that fragile concept we refer to as “the American dream.” This is particularly true for those Americans who reside at the lower end of the socio-economic scale.

PYMNTS.com, in conjunction with Unifund, recently published the results of an extensive study on Americans’ financial habits and circumstances, especially as they relate to access to and use of consumer credit. PMYNTS.com and Unifund surveyed 2,100 Americans. The sample generally mirrored national demographics with one important exception: it focused more heavily on relatively low-income Americans. Entitled FINANCIAL INVISIBLES, the goal of the study was to “help deepen our insights into the use of credit by those who are financially challenged.”

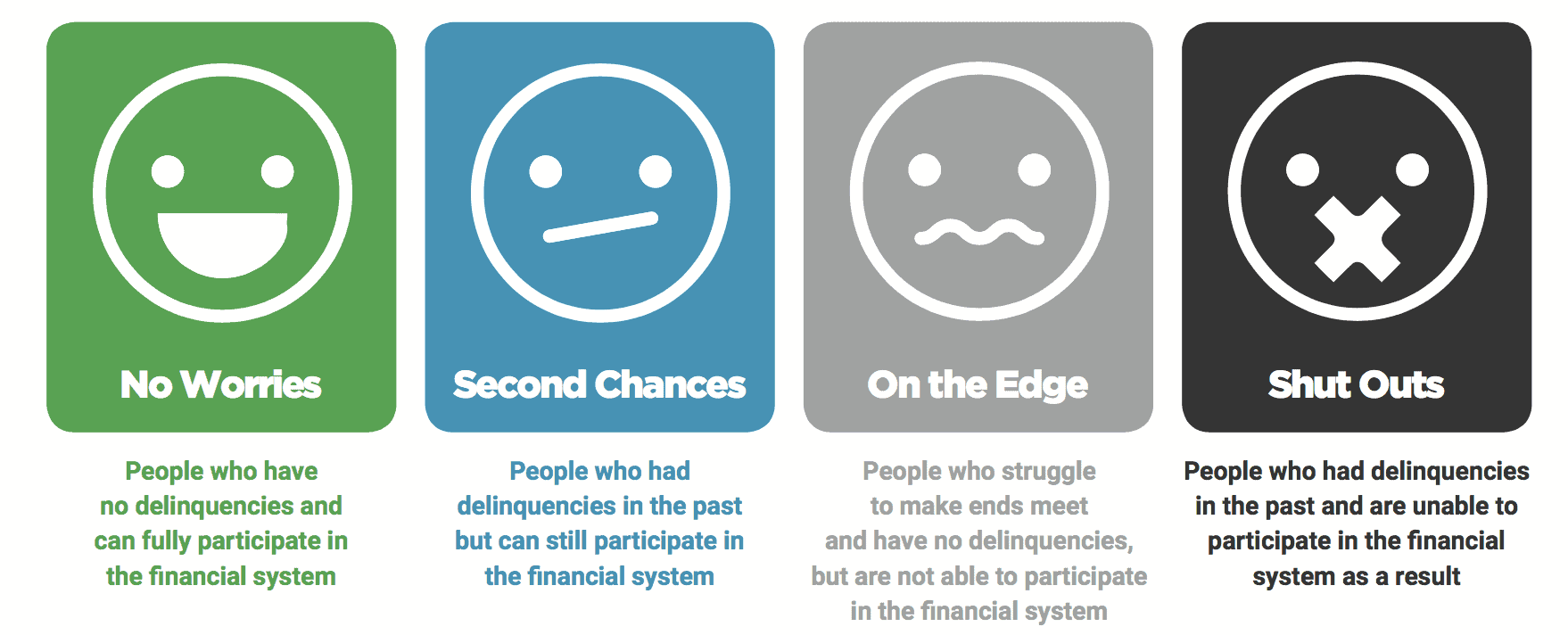

The respondents were divided based on four different profiles:

The following points are pulled from the report:

- The Shut Outs have credit scores of approximately 525, compared to 714 for the No Worries

- Only 4% of Shut Outs have credit cards. By contrast, 30% of On the Edge and 65% of No Worries have cards.

- Almost 98% of Shut Outs without a credit card can’t get one.

- More than 1/3 of all people who cannot get credit cards use prepaid cards as an alternative; the next most common financing technique is to borrow from friends and family members.

- Shut Outs were almost twice as likely to have suffered a life-changing event (g. divorce, death) than No Worries-72.1% vs. 37.1%.

- In general, No Worries and Second Chances, when compared to On the Edge and Shut Outs are:

- Older

- Have significantly higher income

- Male

- College educated

- Employed full-time

- Retired

Here is a link to PYMNTS.com where you can download the entire FINANCIAL INVISIBLES report.