In a recent post, we reviewed the CFPB’s report on the pandemic’s impact on credit card limits, learning that:

- Total limits (for all accounts-open or closed) declined for borrowers with the highest scores while stagnating for others.

- Limits on existing accounts fell again, especially for high credit borrowers.

- Account closures, which spiked during the early stages of the pandemic, have returned to pre-pandemic levels.

Today’s post reviews the CFPB’s follow-up to the credit card study by looking for credit access for all major credit categories: cards, mortgages, and auto loans.

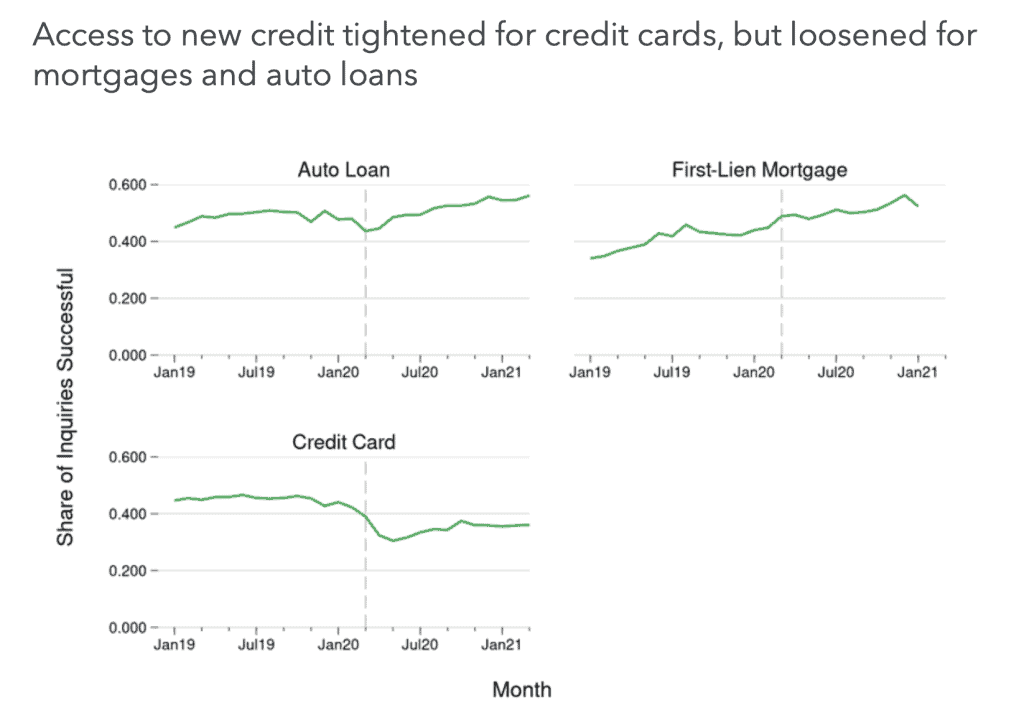

The data below reflects the “success” rate of inquiries, meaning the percentage of hard inquiries to a consumer’s credit report that results in a NEW account or an INCREASE in a credit limit.

In the first chart, we see the share of hard inquiries (to a consumer’s credit report) that were followed by either the opening of a new account or in an increase of the credit limit within:

- 14 days for credit card and auto loans

- 120 days for mortgages

The analysis covers the period from January 2020 through February 2021. Here’s what we see:

- There was a dramatic drop in the inquiry success rate for credit cards in the early stages of the pandemic-from about 45 percent in January to 30 percent in May. The CFPB points out that a drop of this magnitude was far more than would be expected from seasonal variations. While success rates rebounded a bit in the summer of 2020, they are still well below pre-pandemic levels. In March 2021 (not shown), success rates for credit cards began to return to pre-pandemic levels.

- After a minor dip in March 2020, inquiry success rates for auto loans rose throughout 2020 before beginning to level off in early 2021.

- We see the same inquiry success rate trends for mortgages throughout 2020 and into 2021. But, in the case of mortgages, we did not see an impact on inquiry success rates in the early stages of the pandemic.

The CFPB points out that the significant decline in success rates for credit cards might partially be explained by the fact that different types of consumers applied for credit cards during the pandemic, compared to the typical (i.e., pre-pandemic) credit card applicant. In other words, fewer consumers with a high likelihood of inquiry success applied during the pandemic, especially the early stages.

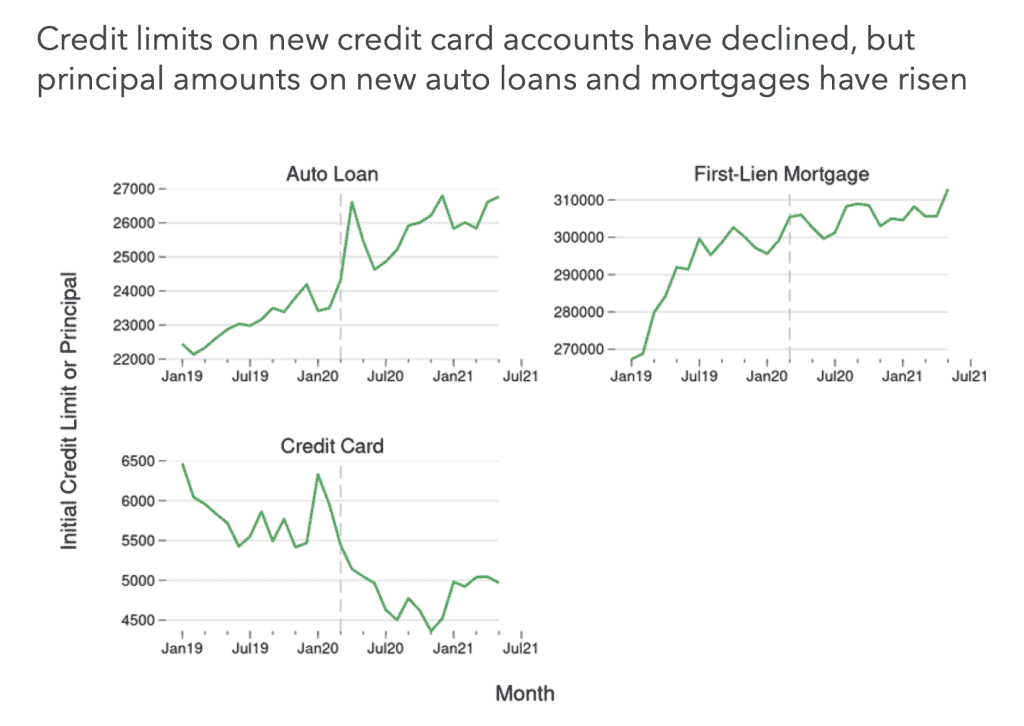

Next, we look at credit limits.

The chart below considers initial credit limits on principal balance on auto loans on accounts opened between January 2020 and April 2021.

We see:

- Generally, those who borrowed for new cars and mortgages enjoyed higher initial balances through the pandemic and into 2021. These trends reflect the fact that prices of vehicles and homes rose during the same period.

- We see a completely different story with credit cards, as limits dropped dramatically in the early months of the pandemic. The average limit for 2020 was about $4,900, or 14 percent less than the 2019 average.

We will continue to monitor the credit story as the safety net afforded by the CARES Act begins to drop away. For example, extended unemployment benefits for millions of Americans ended a few weeks ago. Will the reduction in benefits prompt more Americans to re-enter the workforce? And, if so, will employment bolster their chance of securing more credit?

SOURCE

To learn more about Recovery Decision Science, contact:

Kacey Rask : Vice-President, Portfolio Servicing

[email protected] / 513.489.8877, ext. 261