Earlier this year, the New York Federal Reserve Bank released its first Small Business Credit Study. The report looked at the business conditions and credit environment faced by businesses that employ full- or part-time workers.

OVERVIEW

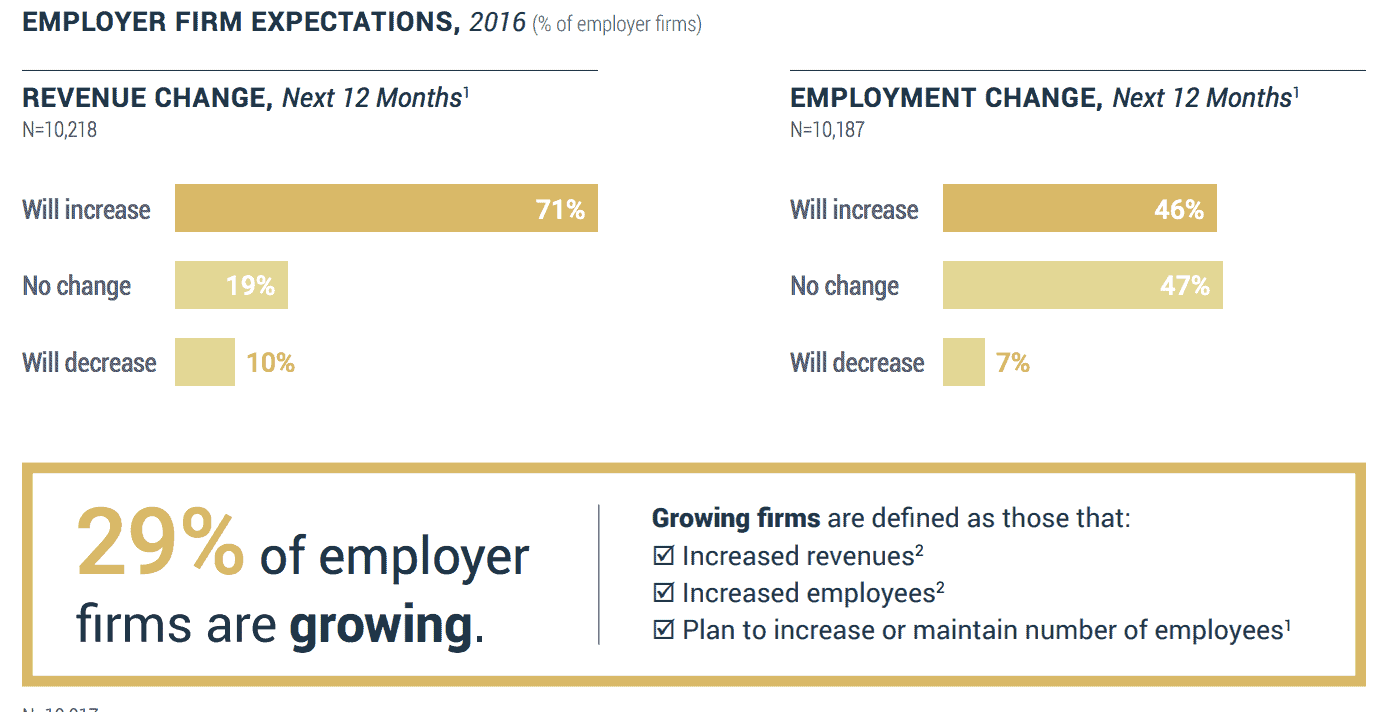

Generally, small business owners were optimistic about the state of the economy as well as their business situations. Specifically, 29% of employer firms were growing, as defined by expectations for both increased revenues and employee growth:

At the same time, a majority of owners said their financial situation dictated the need to use personal resources to fill financing gaps for their business. The issue of business financing becomes more challenging for smaller firms.

Let’s take a look at some of the highlights of the report:

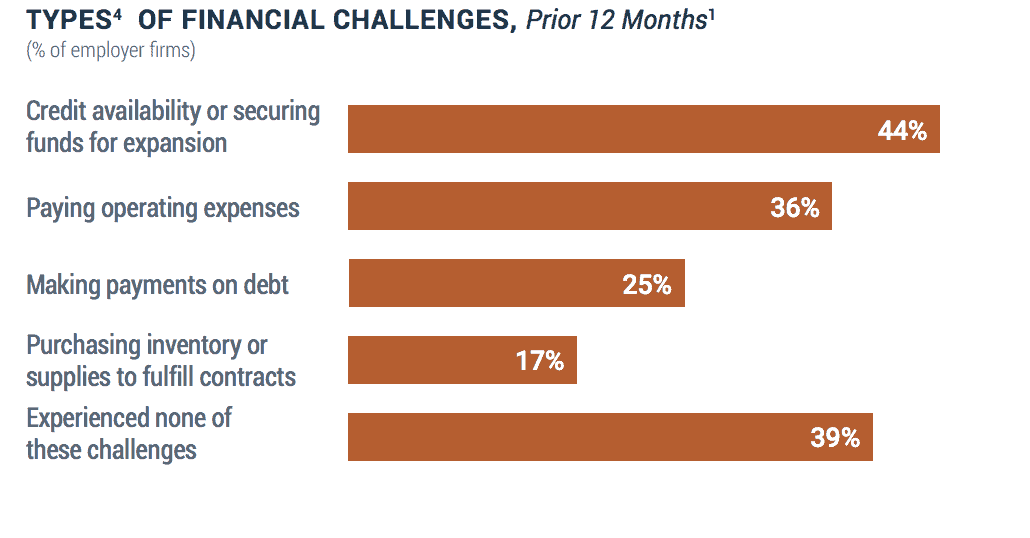

FINANCIAL CHALLENGES

- 61% of employer firms faced financial challenges. Of those challenges, securing credit for expansion was the most significant, as seen in the chart below:

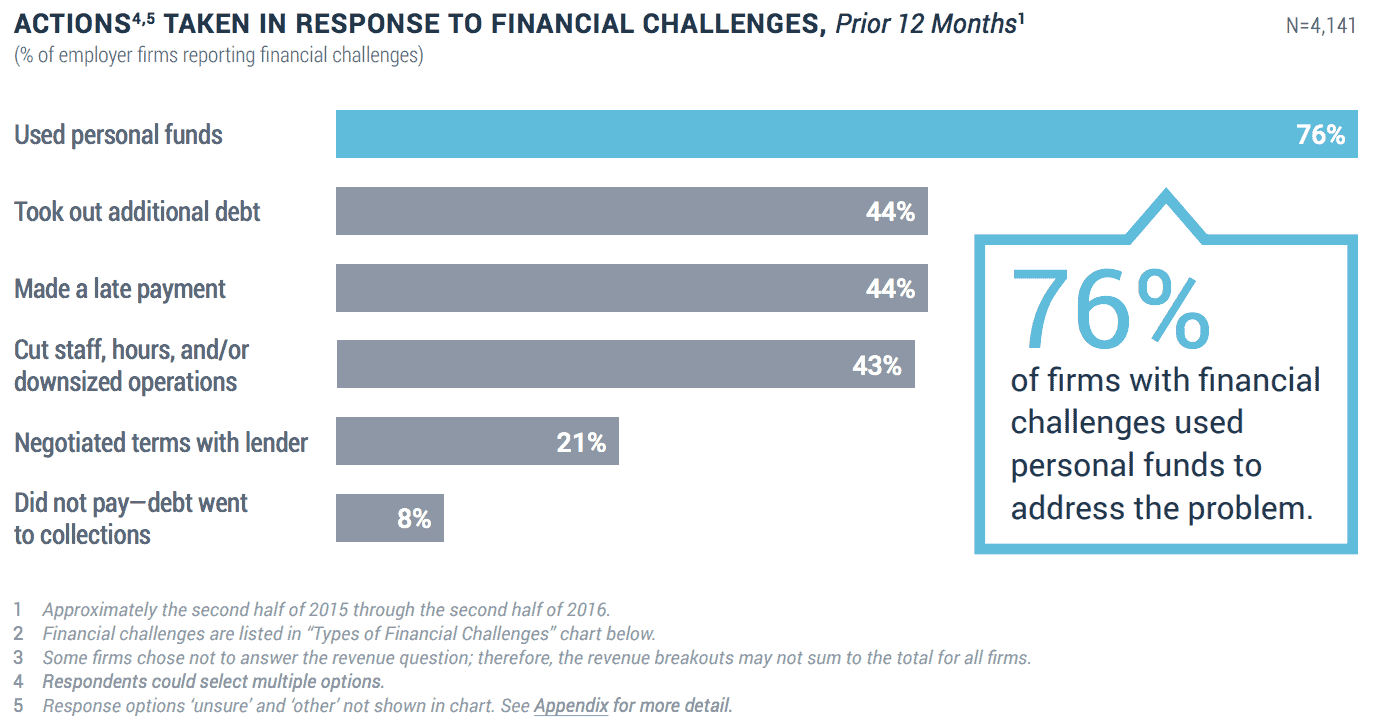

- 76% of firms used personal funds to cover business shortfalls:

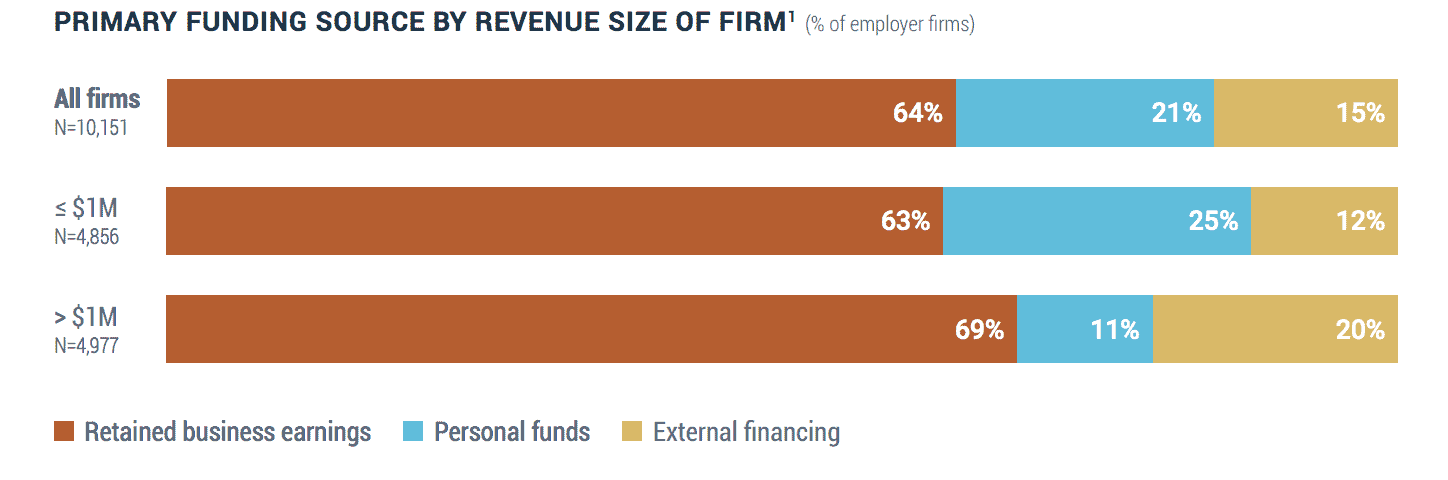

FUNDING BUSINESS OPERATIONS

- Smaller firms are more reliant on personal resources to fund business expansion:

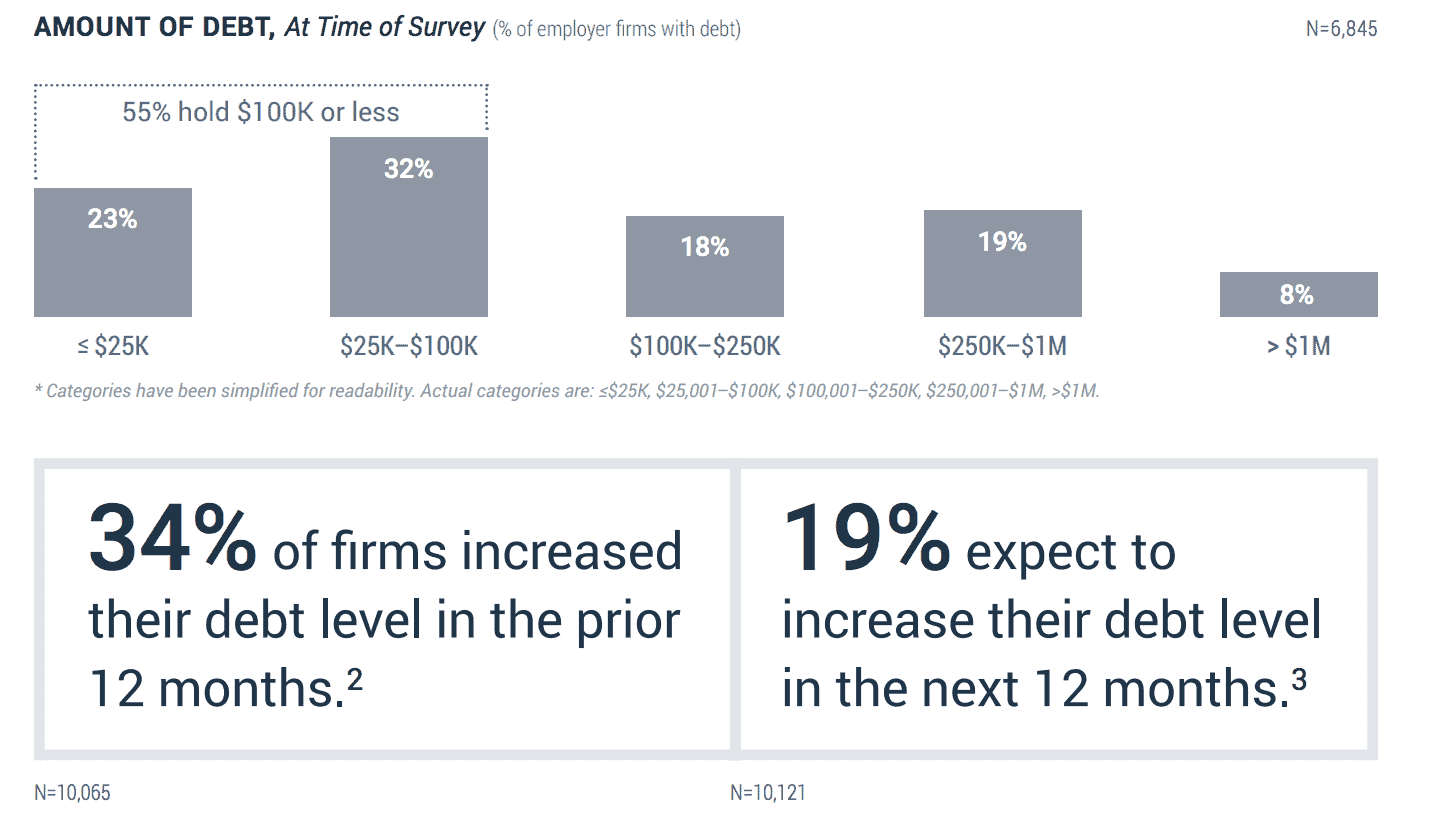

- 71% of firms have outstanding debt:

RELIANCE ON PERSONAL FUNDING

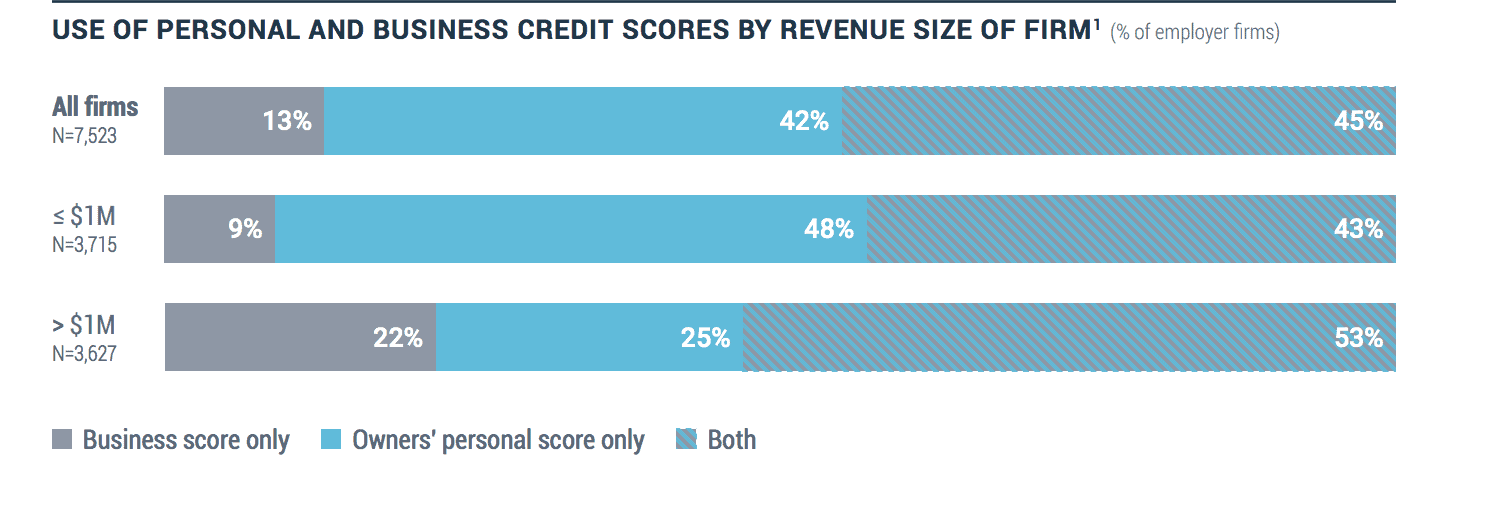

- 87% of firms rely on their personal credit scores to secure funding:

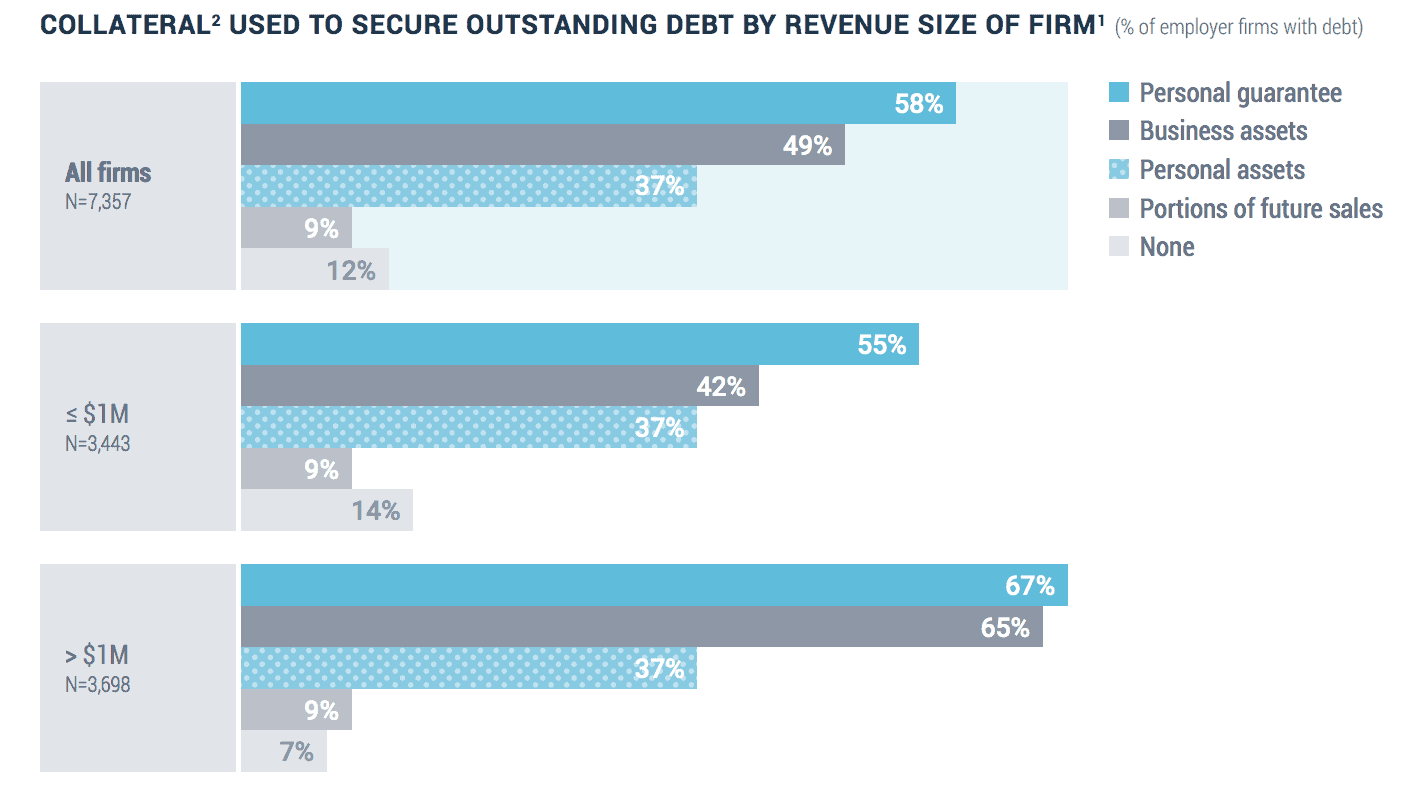

- Personal assets and personal guarantees are commonly used when securing funding:

DEMAND FOR FINANCING

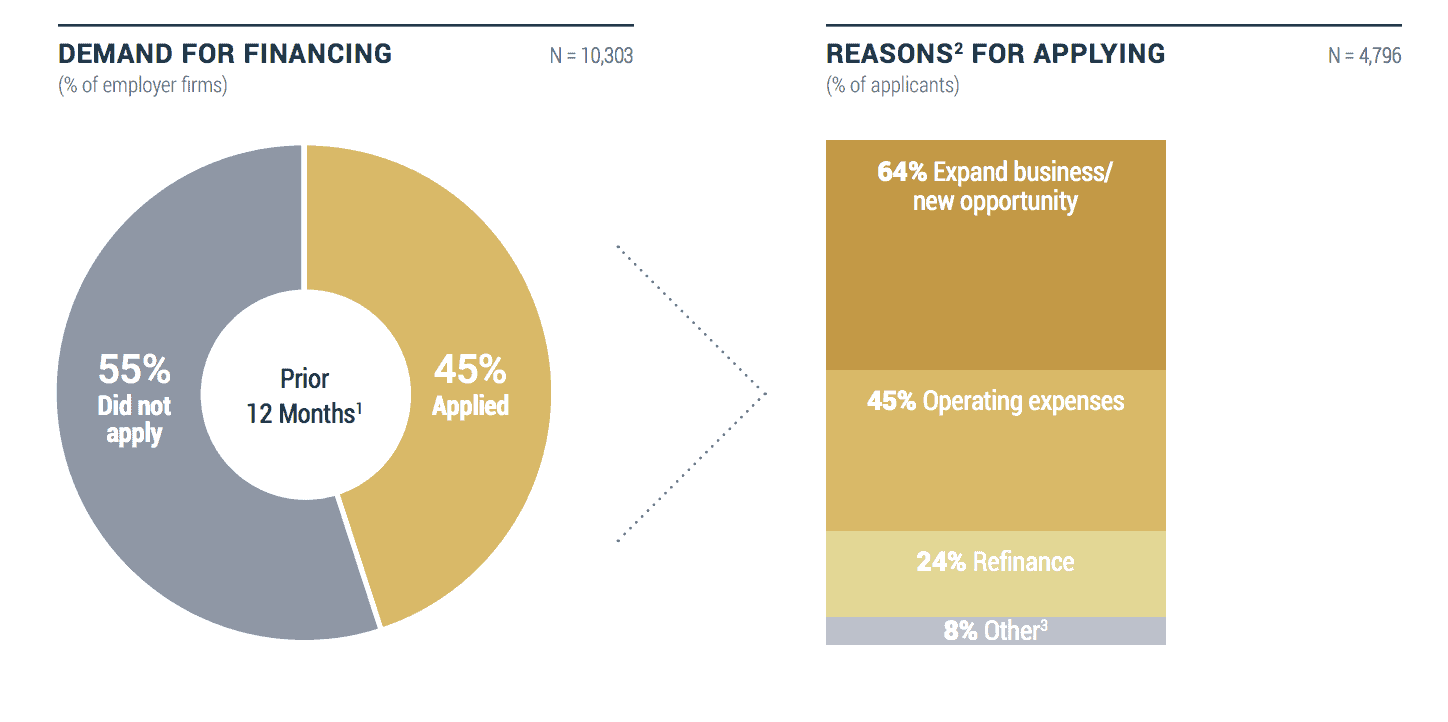

- Of the 45% of firms that sought financing, nearly two-thirds were looking to expand their business and take advantage of new opportunities:

- 55% of those seeking financing asked for $100,000 or less:

CREDIT WORTHINESS

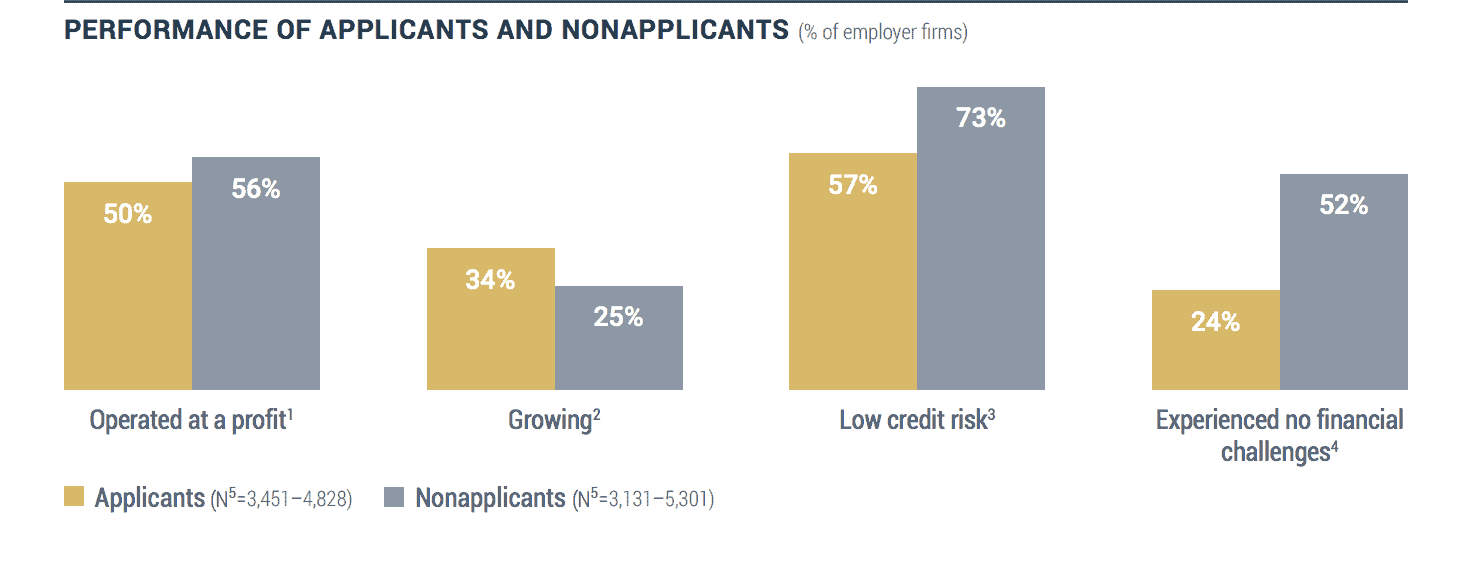

- Interestingly, those businesses applying for financing were typically growing compared to non-applicants, yet had challenges that impacted their creditworthiness:

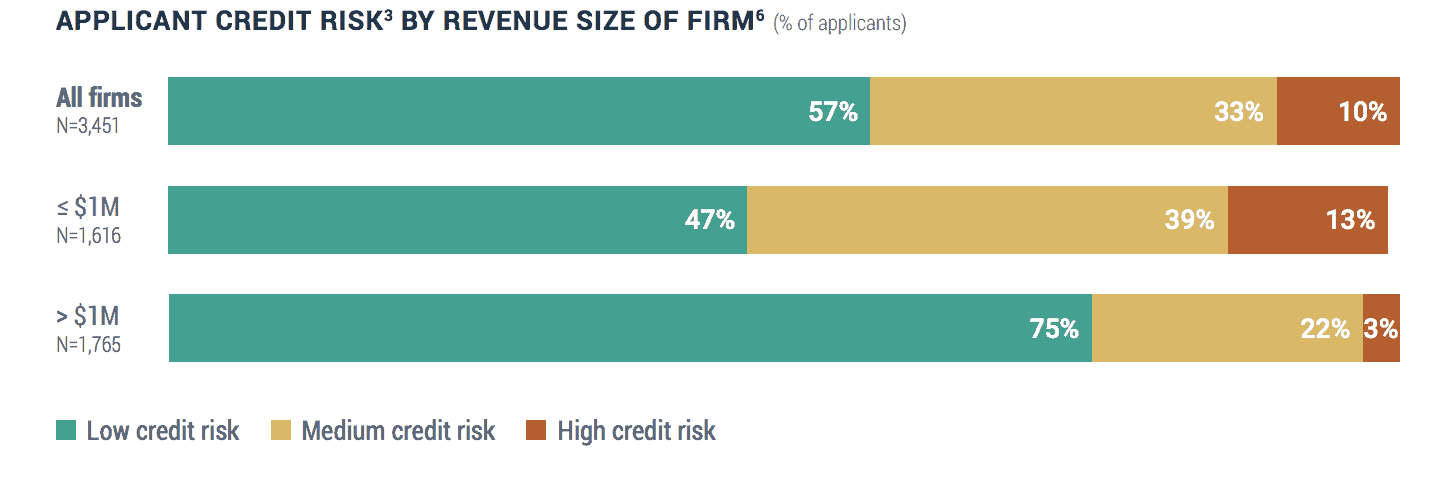

- Larger firms ($1MM+) tended to have better credit scores than smaller firms:

FINANCING RECEIVED

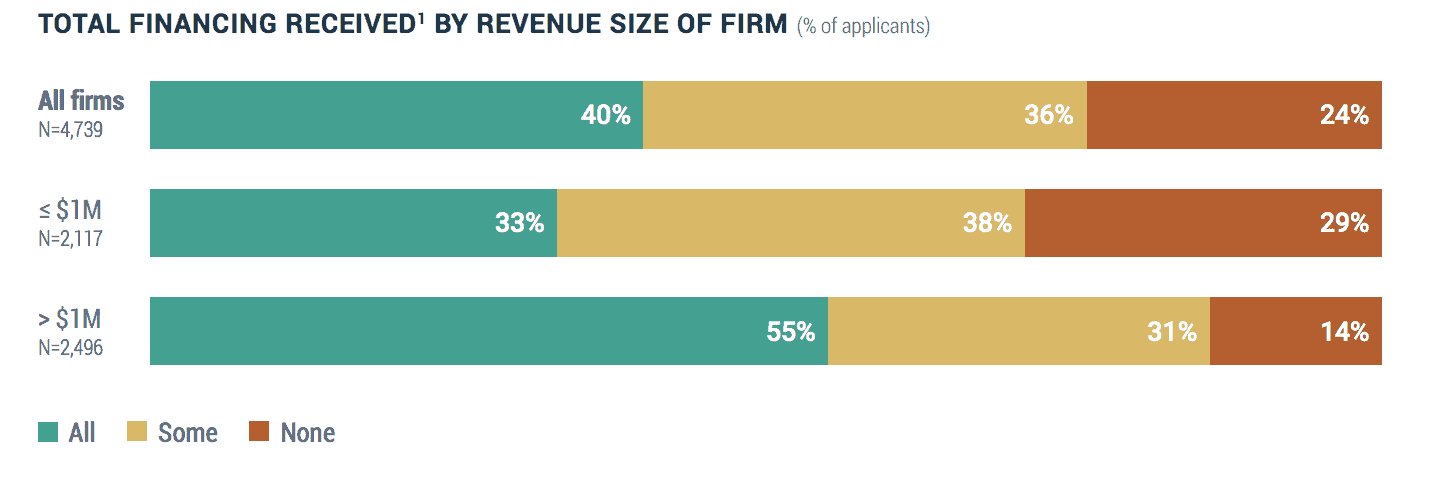

- 76% of firms received funding, with 40% securing the total amount sought:

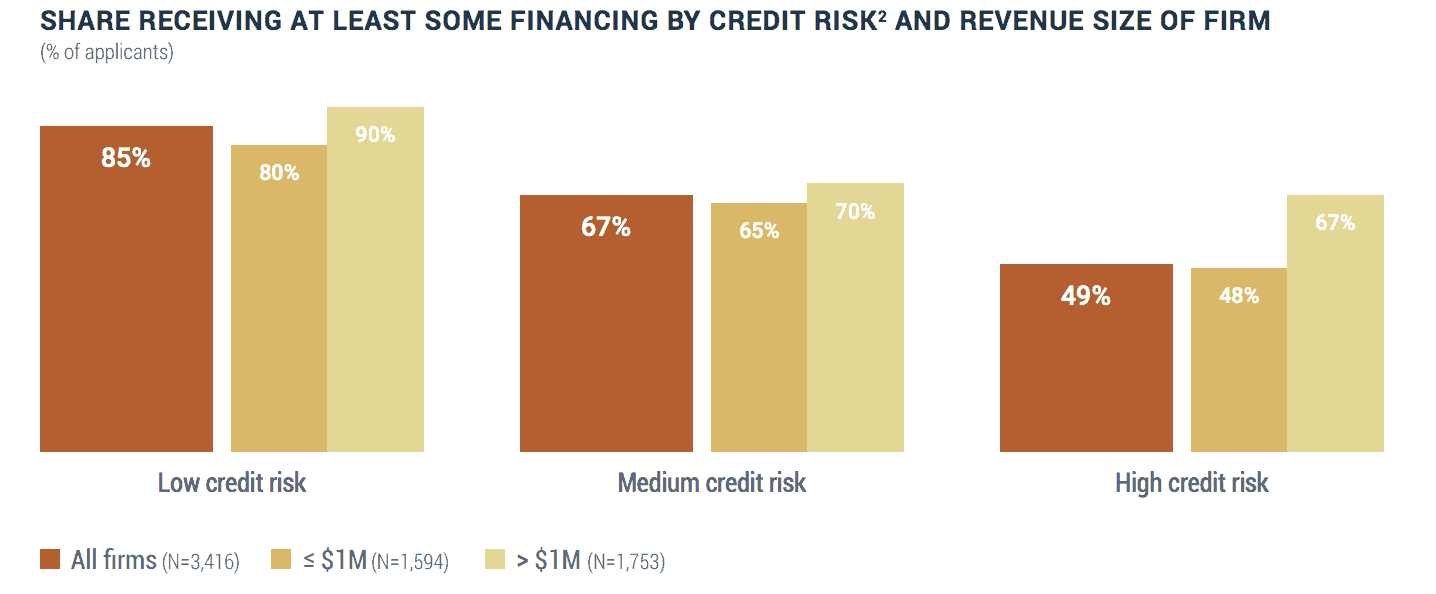

- Smaller firms received less funding than their larger counterparts, even taking into account credit risk:

FINANCING SHORTFALLS

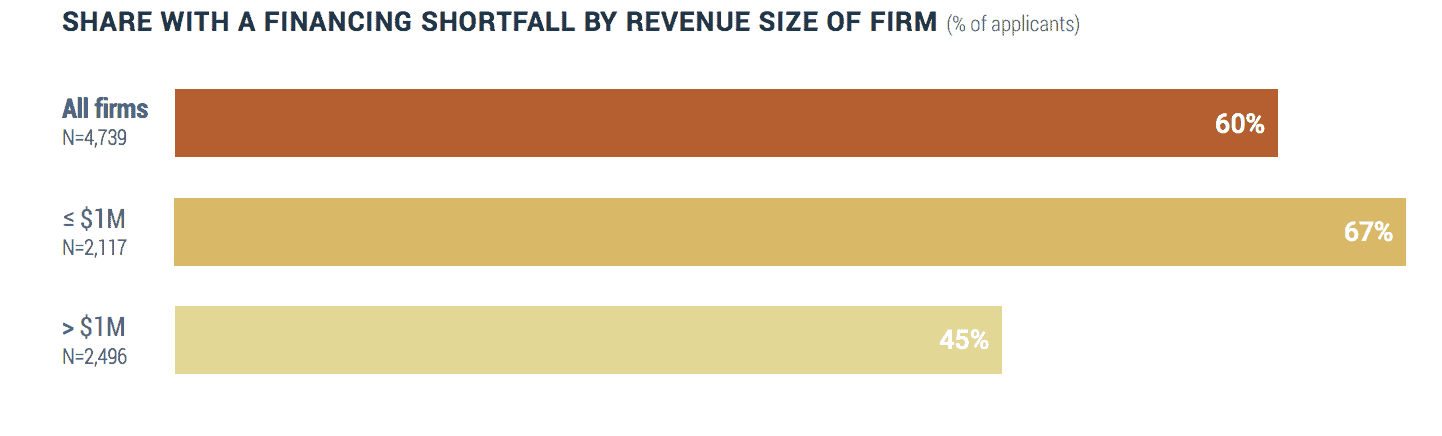

- 60% of firms received less than their desired financing, while 24% did not obtain any financing:

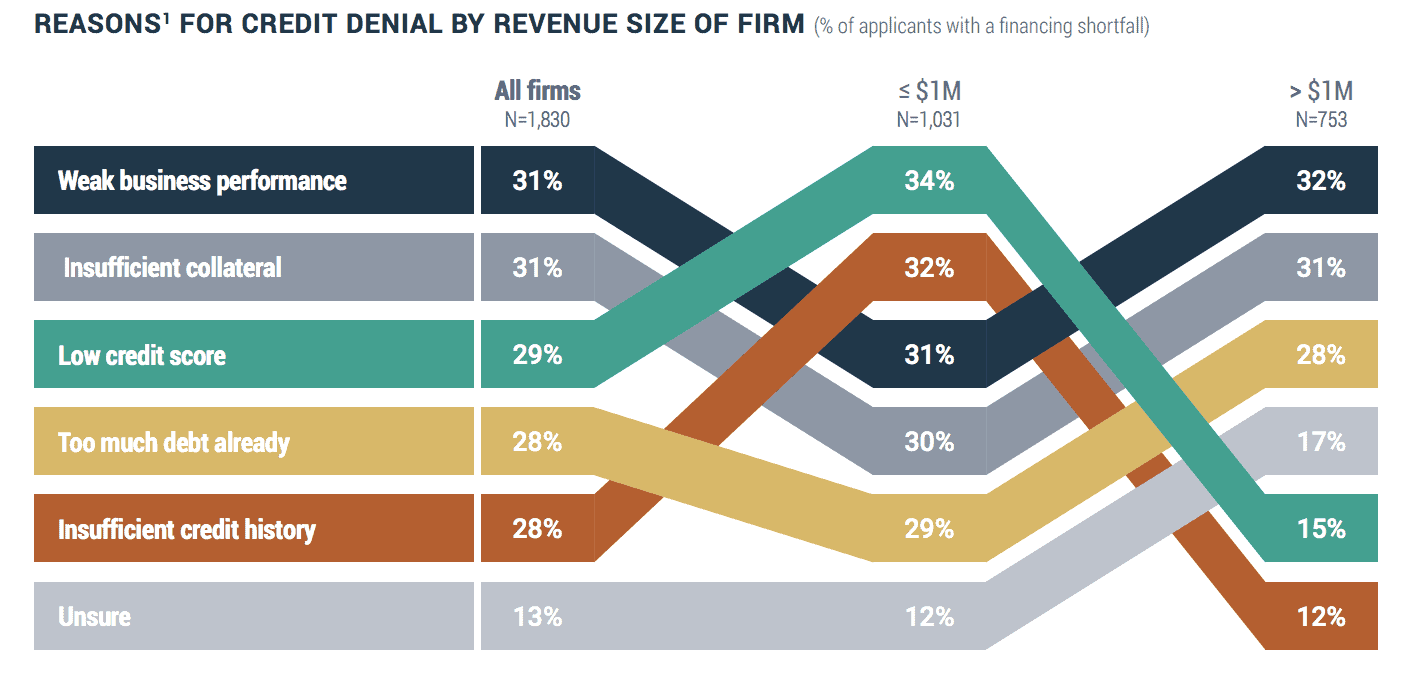

- The reasons for not receiving financing varied by size of the firm. Smaller firms were blocked because of either poor credit scores or lack of credit history:

SUMMARY

It’s important to remember, this study covered the 2016 business environment. As interest rates climb and credit tightens, it will be interesting to watch how market dynamics impact smaller firms in particular. We know, for example, that among the general population, credit card delinquencies are starting to creep up. Could we expect to see the delinquency trend extend to small business owners?

SOURCE:

https://www.newyorkfed.org/medialibrary/media/smallbusiness/2016/sbcs-report-employerfirms-2016.pdf