According to data from the Federal Reserve Bank of New York, total household debt balances increased by $92 billion in the third quarter of 2019, with one of the largest gains coming in the $20 billion increase in student loan balances.

The Quarterly Report, as with other Fed reports, is based on the Consumer Credit Panel, which is itself based on anonymized Equifax credit report data.

Race is a dimension in which repayment of student loan outcomes vary, but data limits the Fed’s exploration of the topic. Credit bureaus do not capture information on race, as the Equal Credit Opportunity Act prohibits the collection of information on protected characteristics, including race. By design, federal student loans are not underwritten to ensure that students may finance their own college education without concern for their own or their parents’ financial history.

Instead of individual-level race information, the Fed extrapolated information about the borrowers’ location and assigned zip codes based on which racial group is predominant, according to the U.S. Census Bureau’s American Community Survey. They grouped zip codes by the race of the majority of zip code residents.

While not perfect, as certainly, there are many black Americans who live in majority-white areas, the technique found 33 percent and 42 percent of black and Hispanic people respectively live in majority-black or majority-Hispanic zip codes. Thus, the framework serves as a rough proxy for a large share of the population, and particularly those who face the effects of living in segregated neighborhoods.

When the Fed disaggregated student loan borrowing and repayment behavior by area race composition, significant gaps presented. Borrowing rates are somewhat higher in areas with a majority of black residents, at 23 percent, compared with 17 percent in Hispanic-majority zip codes and 14 percent in white-majority zip codes.

The differences are likely explained, in part, by income disparities, as lower-income students are more likely to need student loans to afford tuition, even with need-based aid covering some of the affordability gap. But in addition to higher borrowing rates, the balances are higher too.

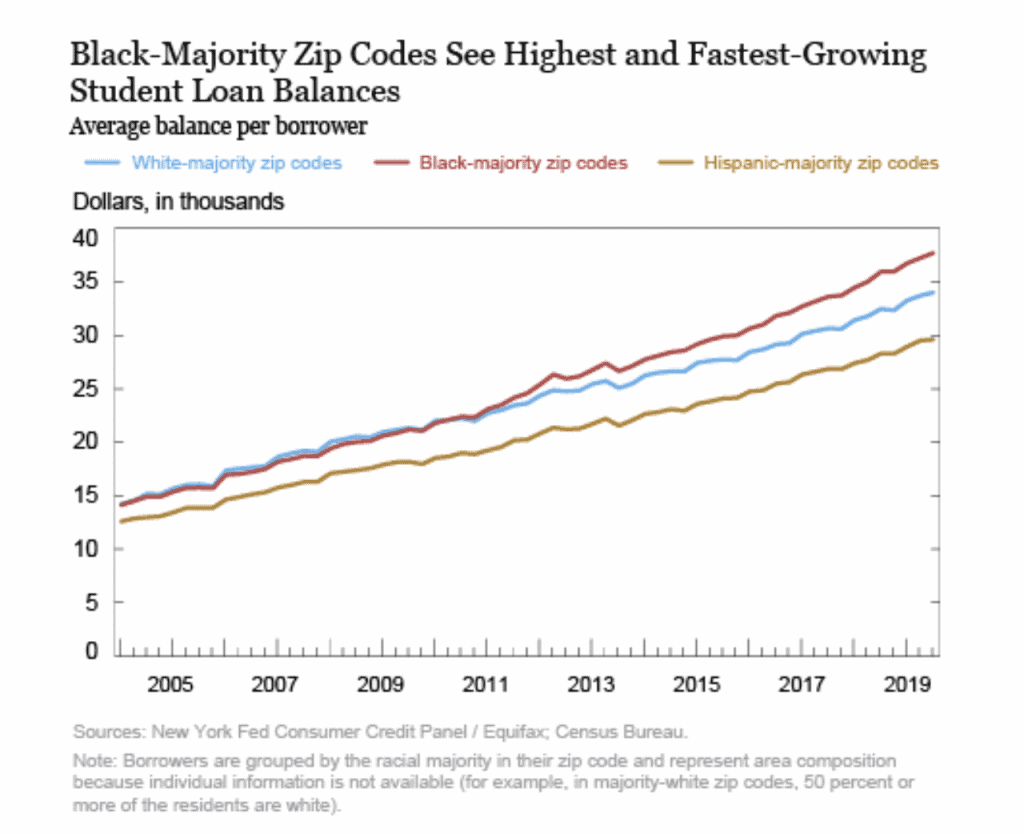

Below, we look at the average student loan balances, per borrower, with zip codes grouped by the race of the majority of residents. Student loan balances at the end of September 2019 are between $29,000 and $38,000 and have experienced steady growth in the past fifteen years.

The average student loan balance is highest in black-majority areas, at more than $37,000. This is especially remarkable when we consider that the average income reported on tax returns in these areas – 2016 was the most recent year available — was $38,000, implying very high debt-to-income ratios for student loans alone. The average balance for Hispanics, though lower than the average balance in majority-white areas, is about $29,000.

There have also been differences in the growth rates. The average balances among borrowers in white- and black-majority zip codes tracked each other very closely until about 2010, when the balances of borrowers in black-majority zip codes began diverging from those in white-majority zip codes and have since continued to trend higher.

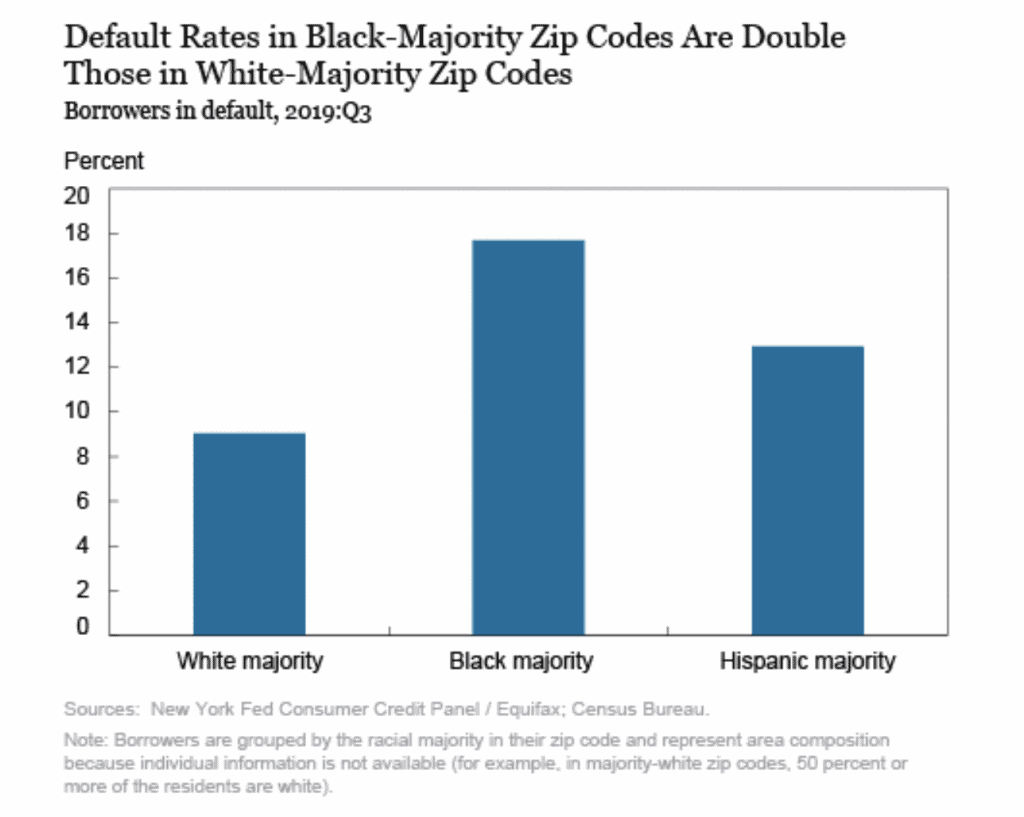

The chart below shows default rates broken out similarly by the racial composition of zip codes. The default rate, measured as the share of defaulted borrowers among all borrowers, in black-majority areas is 17.7 percent, compared with 9.0 percent in majority-white areas. The repayment struggles suggested by relatively higher default rates in majority-black and majority-Hispanic areas point to the likely importance of income differences across borrowers from different areas.

The federal student loan program aims to make college education available for all qualified students and certainly has achieved its goal for many. Recent studies from the Fed have concluded that college remains a good investment and,on average, that’s true.

But, high delinquency rates suggest that the high borrowing rates may not be paying off immediately for all borrowers, particularly if their income remains insufficient to maintain current status on their debt service payments. Further, with lower rates of homeownership among student loan borrowers — and particularly among delinquent student loan borrowers — this rate of borrowing and default may have long-term consequences on the financial stability and wealth of the borrowers.

Fair and equal access to the federal program to help finance college remain central to its purpose. For those borrowers who are successful in completing their degrees and repaying their loans, the student loan program remains a critical piece of the financing of higher education.

t’s is important to recognize that a significant share of students who borrowed to finance their education, with a disproportionate fraction from majority-minority areas, are falling behind the repayment requirements, even in a historically strong labor market.

SOURCE