In prior posts, we’ve examined other measures of first-time home purchasing, including the changing characteristics of first-time buyers, using data from the Federal Reserve Bank of New York.

In Part Three of our series on first-time home buyers, we today examine Fed data to see how rising student loan debt is crowding out home buyers generally, and first-timers in particular.

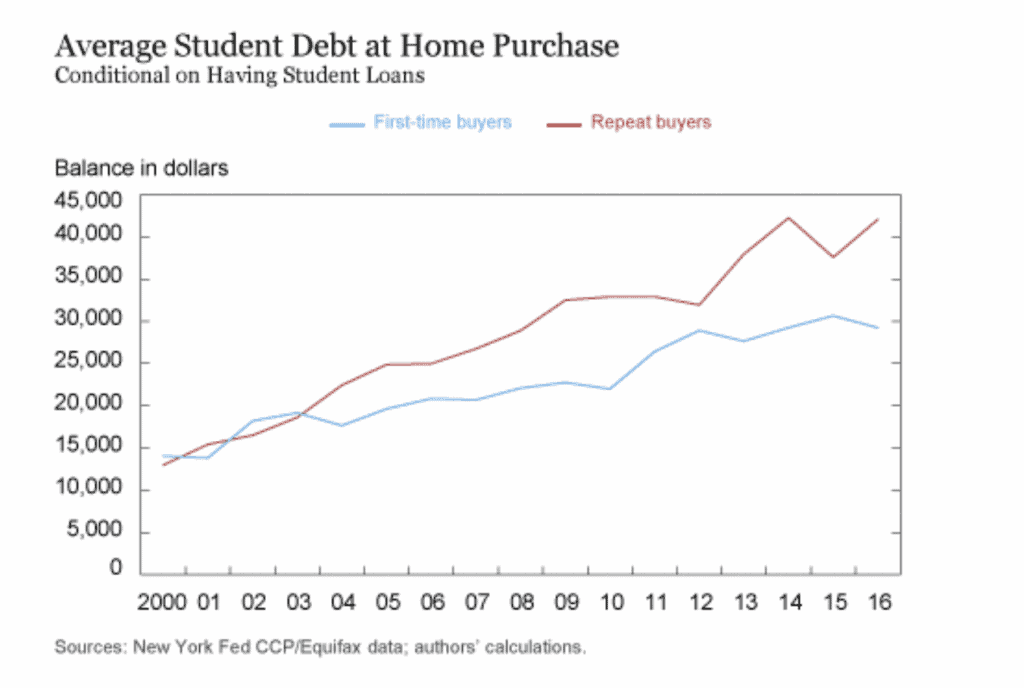

In the chart below, we show average student loan debt for both first-time buyers and repeat ones, conditional on the buyer having one or more student loans.

In 2000, there was essentially no difference in the average size of student loans between first-time and repeat buyers. For both types of buyers, the conditional average student loan debt was around $14,000. This was largely the case until around 2003.

From 2003 to 2010, the average student loan debt grew faster for repeat buyers than for first-time buyers. By 2010, the gap between the two types of buyers had reached $11,000. In the same time range, the home ownership rate for households headed by individuals aged 24 to 32 fell from 45 to 36 percent between 2005 and 2014, nearly twice as large as the five percent-drop in homeownership for the overall population.

By 2016, the average student loan debt for first-time buyers had reached $29,000, compared with $42,000 for repeat buyers, a gap of $13,000.

The Fed has found that student loan debt has a substantial negative effect on homeownership early in life. In particular, a $1,000 increase in student loan debt accumulated before age 23 represents an approximately 10 percent increase in early-life borrowing, which causes a decrease of about 1.5 percentage points in the homeownership rate.

This is equivalent to a delay of two and a half months in attaining homeownership, given the rapid increase in the probability of home purchase the college-going population experiences through this period.

Student loan debt affects a borrower’s ability to obtain a mortgage primarily via credit scores. Higher debt balances increase the borrower’s probability of becoming delinquent on their student loans, which has a negative impact on their credit scores and makes mortgage credit more difficult to obtain.

Since cumulative balances are generally largest immediately upon entering repayment, the effect of higher student loan debt on homeownership access is usually largest immediately upon school exit. Given that income profiles tend to rise over life and student loan payments are fixed, budget constraints ease over time, allowing the individual to accumulate assets for a down payment at a faster rate.

The Fed estimates a $1,000 increase in loans disbursed to a student before age 23 leads to a one-to-two percent reduction in homeownership by the student’s mid-twenties. While the effect of the $1,000 increase in student loan debt leads to a meaningful reduction in homeownership for households in their mid- to late twenties, by age 32 the estimated 0.5 percent reduction in homeownership is a relatively small fraction of the actual homeownership rate.

Next week, we examine the sustainability of first-time homeownership.

SOURCE

https://libertystreeteconomics.newyorkfed.org/2019/04/a-better-measure-of-first-time-homebuyers.html