THE STATE OF DEBT IN AMERICA: 4th QUARTER REPORT

The Federal Reserve Bank of New York’s Center for Microeconomic Data recently issued its Quarterly Report on Household Debt and Credit.

Through the fourth quarter of 2018, total household debt increased by $32 billion (0.2%) to $13.54 trillion. It was the 18thconsecutive quarter with an increase. The total is now $869 billion higher than the previous peak of $12.68 trillion, from the third quarter of 2008. Overall household debt is now 21.4% above the post-financial crisis low reached during the second quarter of 2013.

Here are the key takeaways of the first quarter report, by segment:

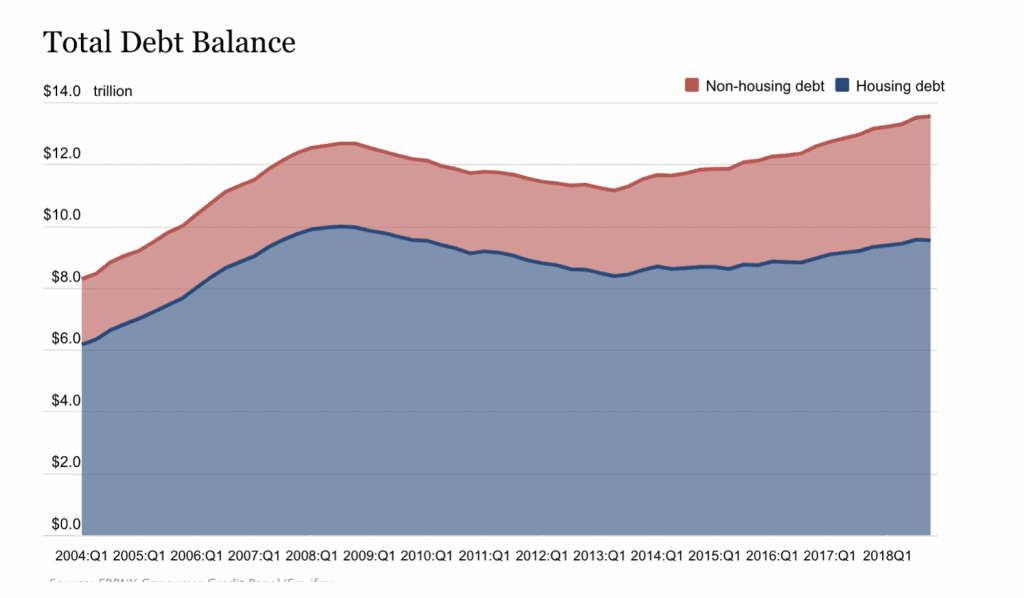

HOUSING DEBT

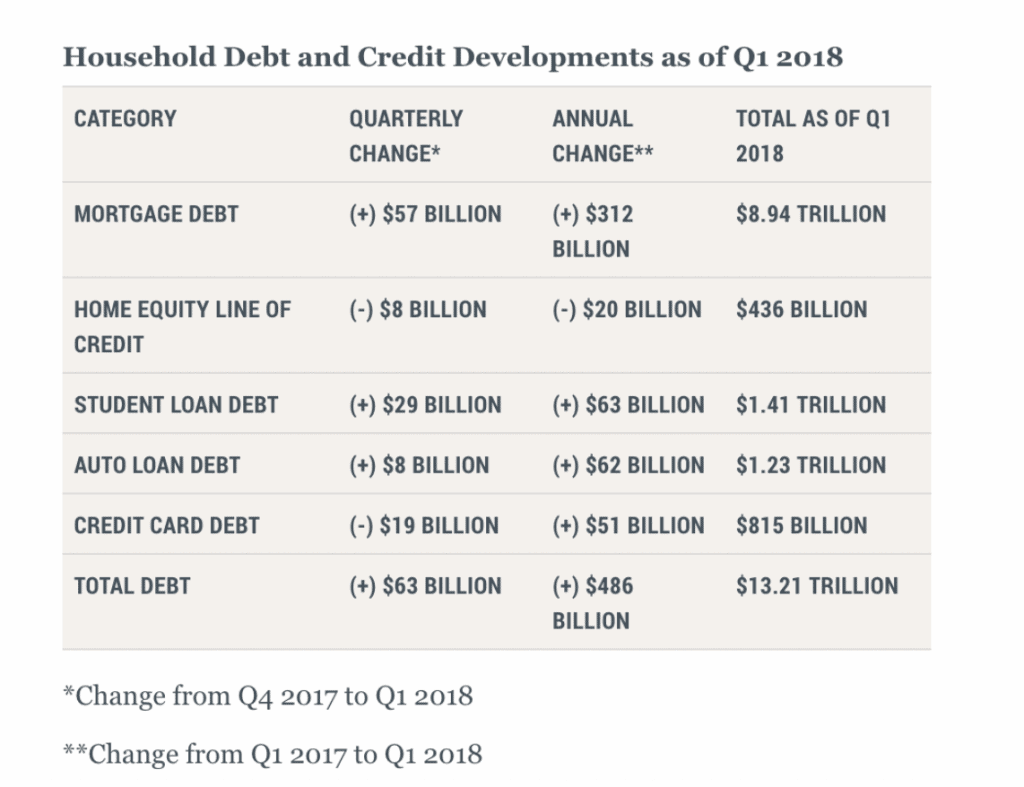

- Mortgage balances-the largest component of household debt-stand at $9.1 trillion.

- Mortgage originations declined to $401 billion, the lowest level in four years.

- Balances on home equity lines of credit (HELOC) continued their downward trend, declining by $10 billion, to $412 billion. This is the lowest level seen in 14 years

,. - The median credit score of newly–originating mortgage borrowers increased from 755 to 761.

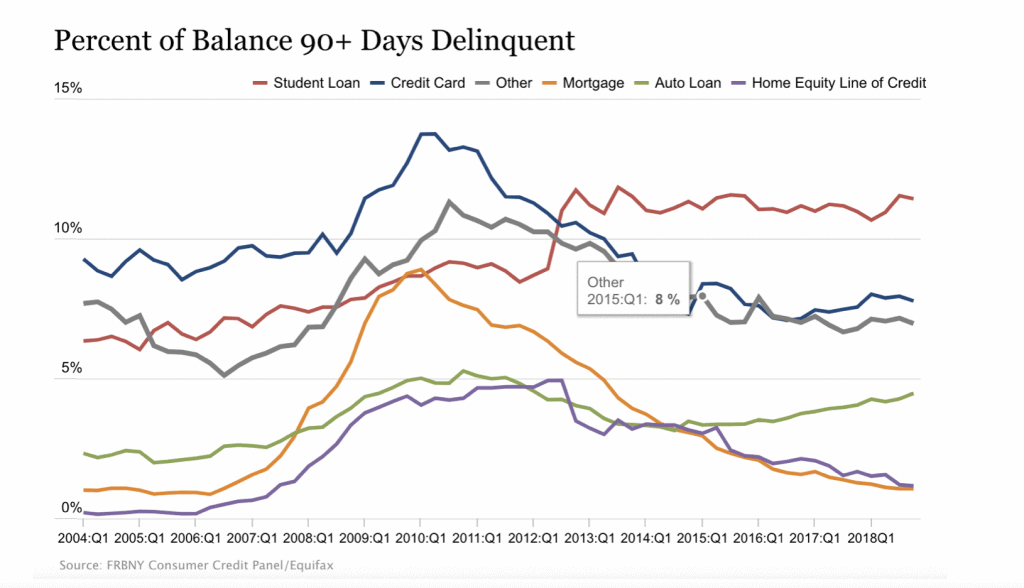

- Mortgage delinquencies were relatively flat, with 1.1% of mortgage balances 90 or more days delinquent in the first quarter.

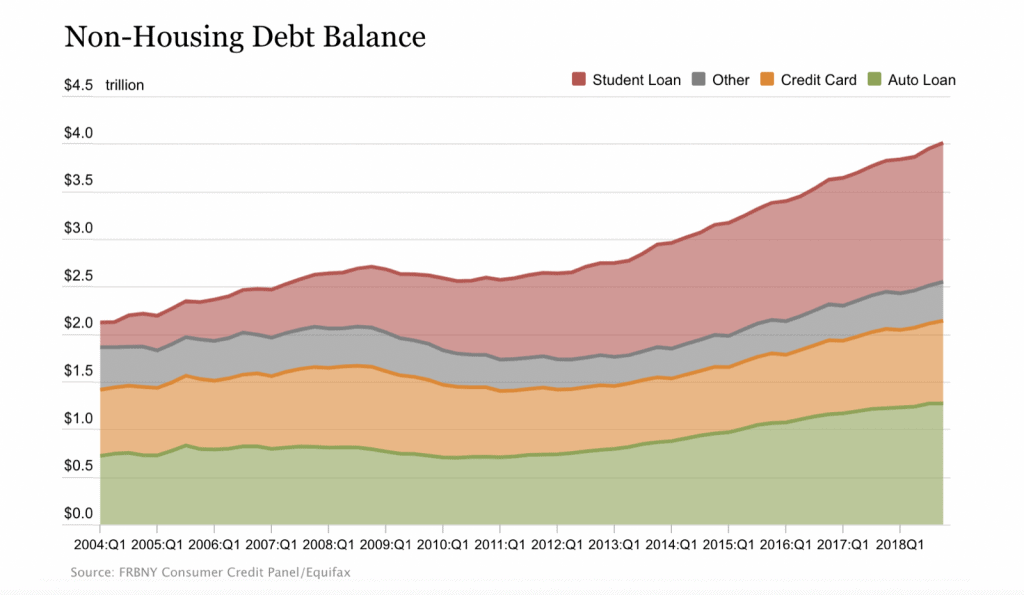

NON-HOUSEHOLD DEBT

- Outstanding student loan debt grew to $1.46 trillion, from $1.44 trillion at the end of the third quarter.

- There was $144 billion in newly–originated auto loans, continuing a nine-year trend. The total of $584 billion in auto loan originations is the highest in the 19–year history of compiling data on auto loan originations.

- Credit card balances rose by $26 billion, to $870 billion.

DELINQUENCIES, BANKRUPTCIES AND CREDIT INQUIRIES

- Aggregate delinquency rates remained steady in the fourth quarter of 2018,

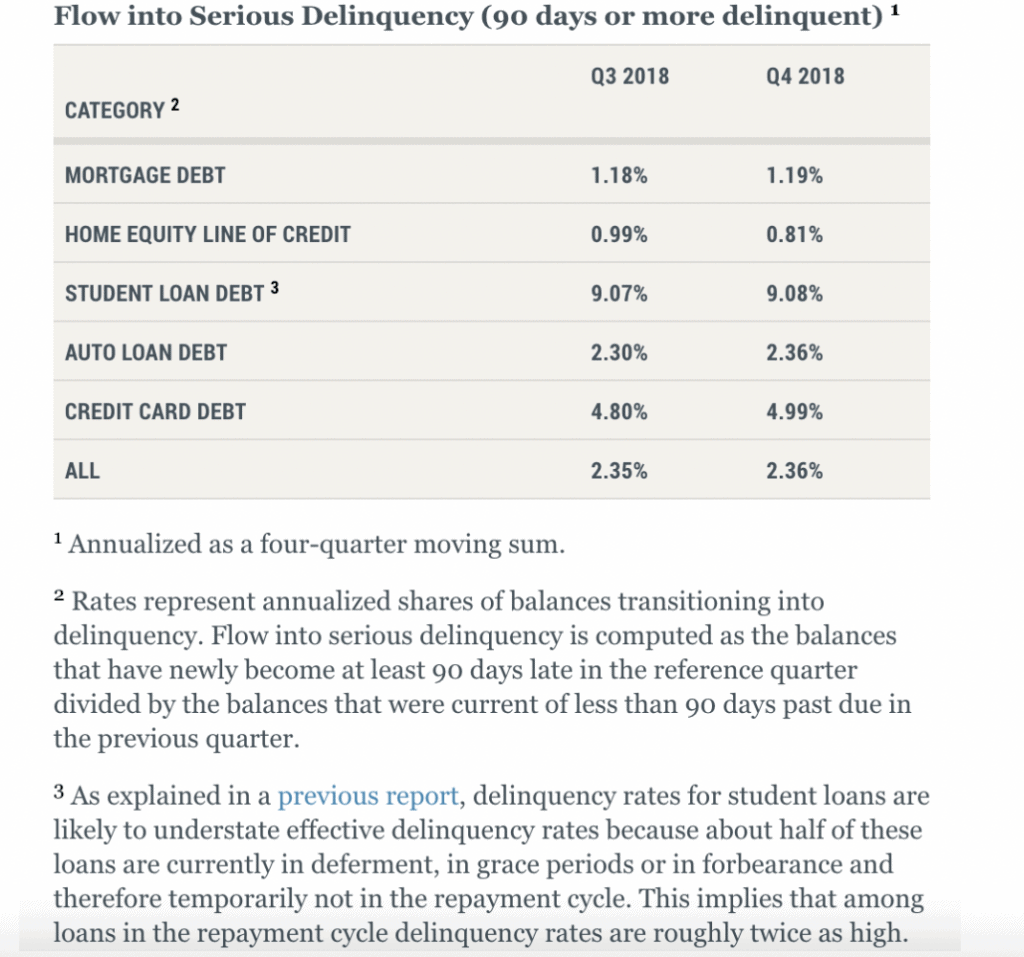

–with 4.7% of outstanding debt in some stage of delinquency. Of the $630 billion in debt that is delinquent, $416 billion is seriously delinquent (i.e. at least 90 days). The flow into 90+ day delinquency for credit card balances has been rising since 2017, while the flow into 90+ day delinquency for auto loan balances has been slowly trending upward since 2012. - About 195,000 consumers hada bankruptcy notation added to their credit reports in the fourth quarter, five thousand fewer than in the fourth quarter of 2017.

- The number of credit inquiries within the past six months—an indicator of consumer credit demand—declined to the lowest level seen in the history of the data.

- Account closings were at their highest level since 2010.

Here is summary of the developments in household debt across each category:

In terms of flow into serious delinquency, we see that there was little change from Q3 to Q4 2018:

SOURCE

https://www.newyorkfed.org/newsevents/news/research/2018/rp180517