A recent report from the Federal Reserve Bank of New York’s Center for Microeconomic Data shows total household debt balances have increased by $192 billion in second-quarter 2019, boosted primarily by a $162 billion gain in mortgage installment balances.

The new mortgage total of $9.4 trillion is slightly higher than the previous high in mortgage balances from the third quarter of 2008.

The source for the Quarterly Reporton Household Debt and Creditis the New York Fed’s Consumer Credit Panel, a data set comprised of anonymized credit reports from the credit reporting agency Equifax.

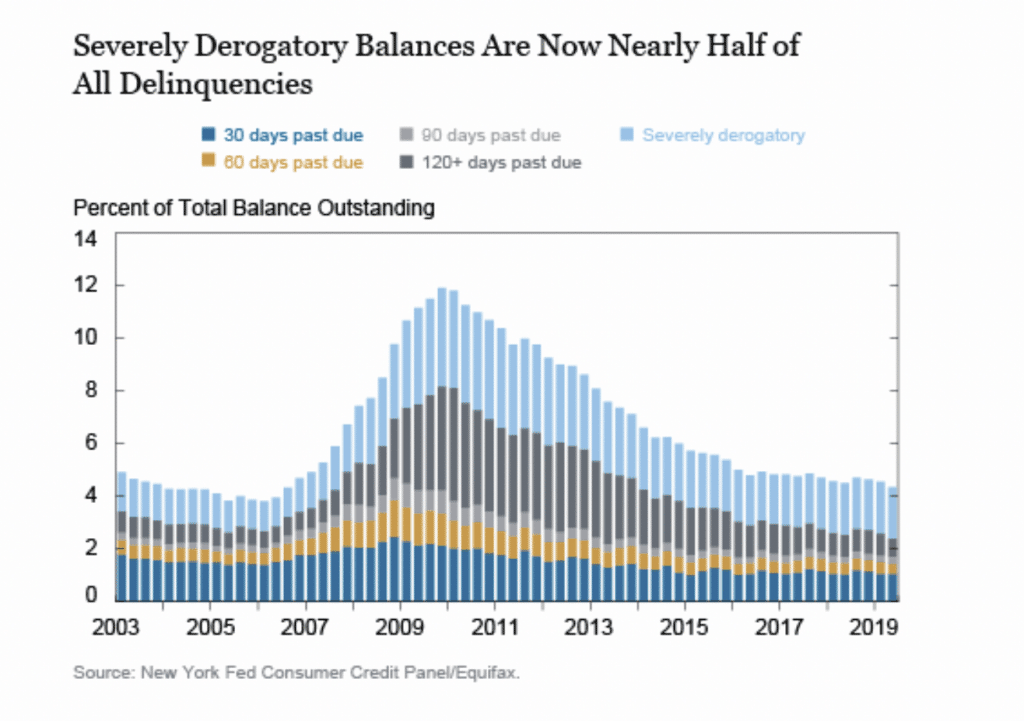

The Fed’s Quarterly Report was designed to measure the health of the consumer balance sheet. Credit bureaus serve as repositories for consumer level “report cards” of borrowing and repayment success, and a simple aggregation of delinquent balances as a percentage of total outstanding balances creates stock delinquency rates, as well as enables us to provide a detailed picture of delinquent debt over time.

Fed data tracks several categories of delinquency – for example, 30, 60, 90, and 120-plus days past due – plus “severely derogatory,” which includes any stage of delinquency paired with a repossession, foreclosure, or “charge off” (meaning that the lender has removed the debt from its books).

Credit bureau data enables us to provide a detailed picture of delinquent debt over time and the chart below depicts the delinquency rate, by severity, since 2003. During and after the Great Recession, the 90-plus day delinquency rate, especially for mortgages, soared and an unprecedented number of properties entered foreclosure. This created a surge in severely derogatory balances that took years to work down, even as other delinquencies declined rapidly.

Although the housing crisis produced a huge increase in severely derogatory mortgages, that effect has dissipated as the foreclosure pipeline has cleared out in even the slowest states.

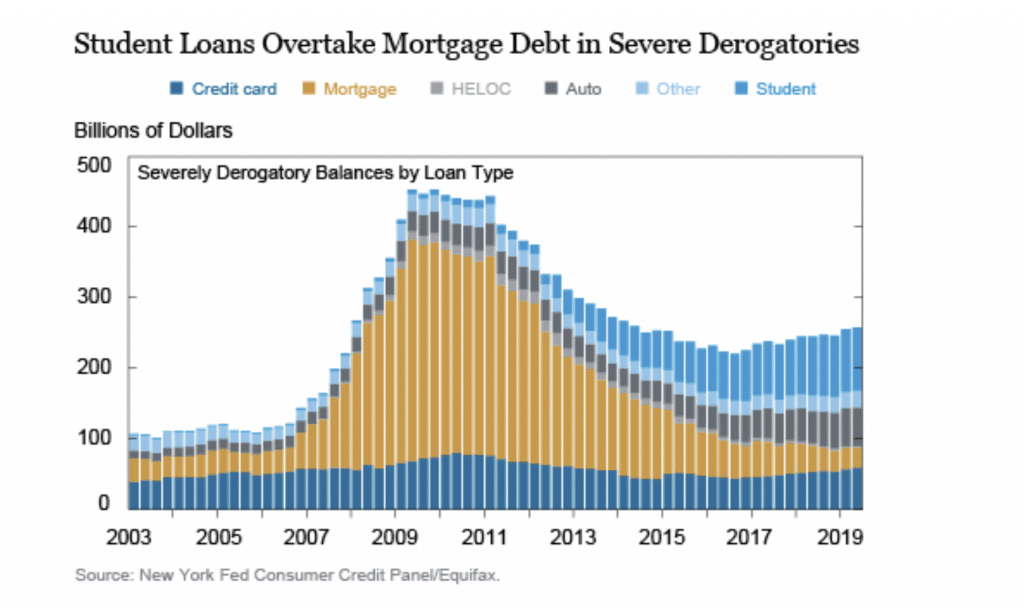

Auto and student loan balances are the interesting components: In the second quarter 2019, the outstanding severely derogatory balance is comprised of 35 percent defaulted student loans, a stunning increase. Auto loans are now 21 percent of the outstanding severely derogatory balance, a larger share than normal.

Auto debt has the lowest “adjusted” serious delinquency rate, below even mortgage and HELOC, and student debt has the highest by far. But, these relative levels would be misleading. A major reason is charge-off practices: Student loans are typically reported as defaulted only after a full year (360 days past due), while auto loans tend to charge off before they reach 120 days past due.

Delinquent debt is important in its own right because it requires repayment, but also because it is reported on credit reports and affects a household’s ability to access credit. Clearly, the health of the household balance sheet remains an economic focus.