Over the last 10 year, the Consumer Payment Research Center, a vehicle of the Federal Reserve Bank of Boston, has studied trends in consumer payment behavior – a valuable tool in a period of evolving payment systems.

The major finding is that consumer payment behavior has been largely stable over the last 10 years. In particular, the 2016 7 and 2017 Surveys of Consumer Payment Choice revealed that most consumers use all four of the major payment options – cash, debit card, credit card, and paper check – in any given month.

The Fed report examined several metrics for gauging usage of payment instruments, including security, convenience, and cost.

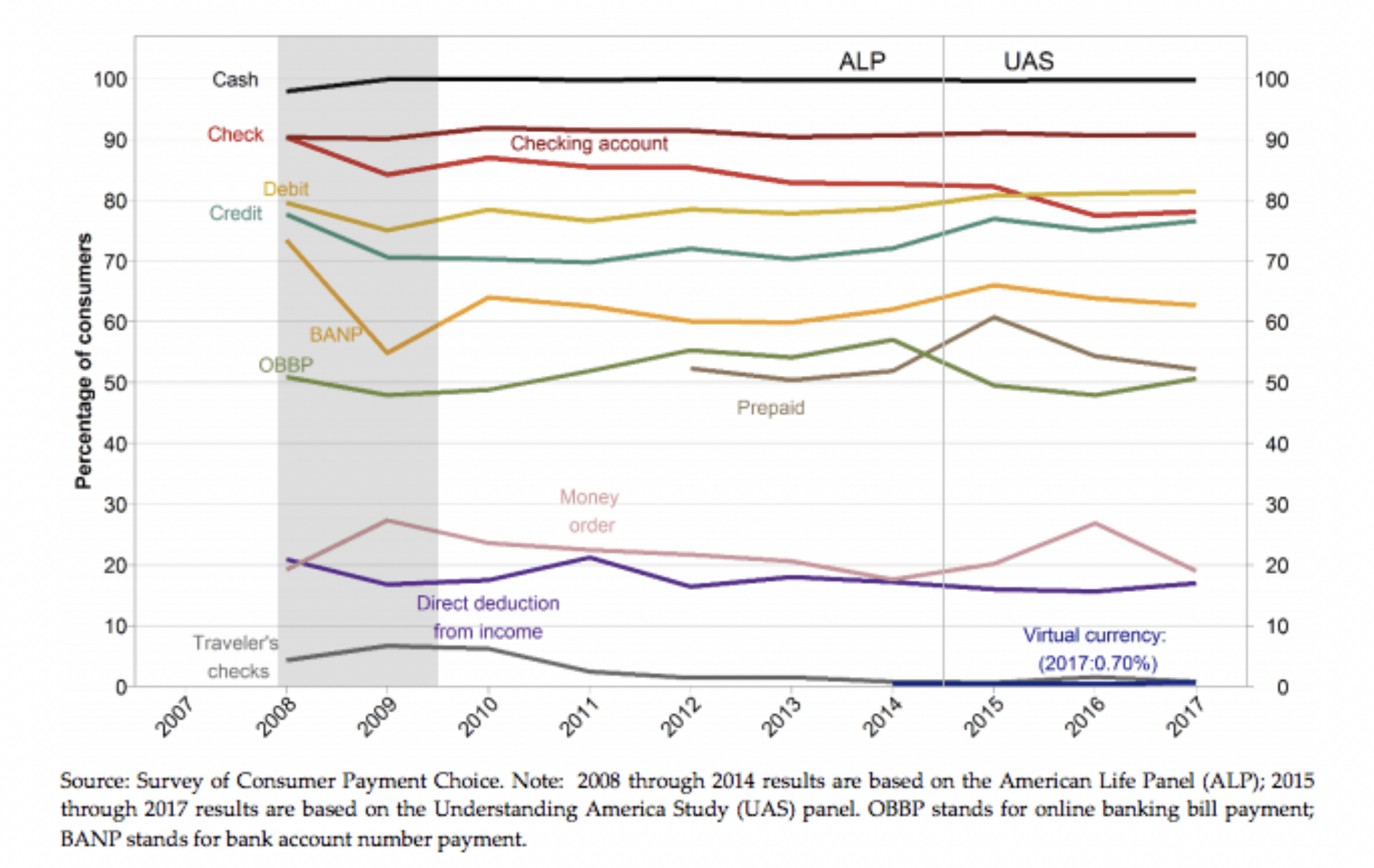

The chart below graphically demonstrates the percentages of Americans using different types of payment instruments.

To summarize the findings demonstrated on the chart:

• More than 70 percent of consumers use all the major payment options as defined above.

• The 2017 report showed 12 percent of consumers didn’t use cash for a single transaction during the previous year.

• Beginning in 2015, the use of paper checks declined while debit card use rose;: fewer than 80 percent of consumers with paper checks reported actually using them.

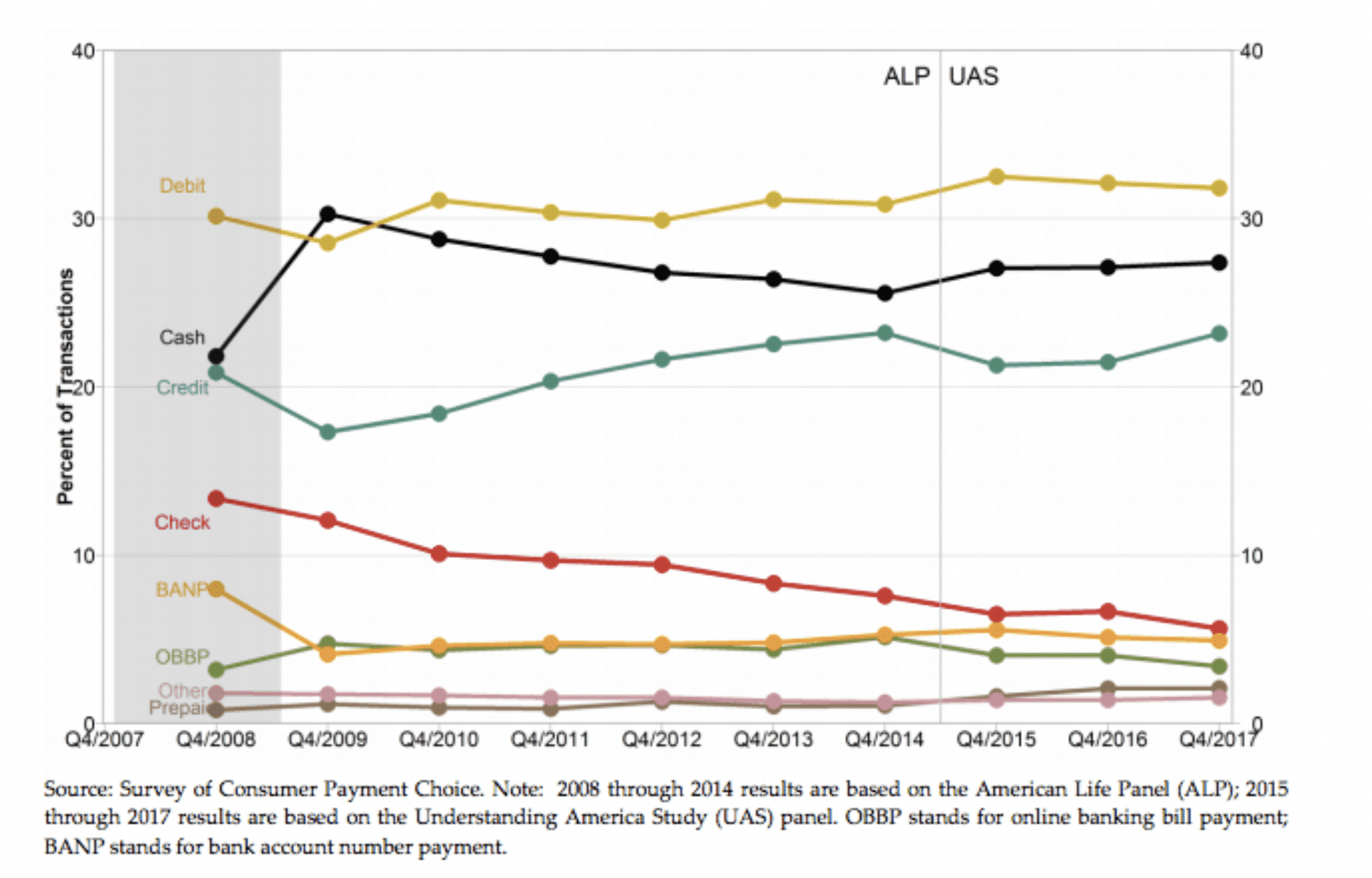

Debit card, credit card and cash have consistently been the most popular payment vehicles over the 10 years of the study. By 2017, most payments were being made with debit card., with a consumer average of 22.1 debit payments or purchases per month. Out of an average total of 40 payments per consumer each month, debit thus accounts for just over 57 percent of all payments.

The chart below graphs the above narrative, showing the decline in paper check usage and steady use of debit, credit and cash. (As a sidebar of interest, note the bump in cash use and correlating drop in credit card use during the 2008 recession.)

One of the more statistically significant findings of the last few years’ studies is the increase in online purchasing and payment by American consumers. Most buyers still purchase retail goods in person, accounting for about half of all purchases, but online purchases bumped up to 12 percent in 2017 from 10 percent in 2015, a statistically significant finding.

As concerns about identity fraud and hacking have increased, it’s notable to point out that credit cards consistently get the highest ratings for records retention and security, as well as scoring high marks among consumers for convenience and acceptance. Credit cards get lowest marks for cost based on interest rates and fees.

Cash, at risk for being lost or stolen, ranked lowest of all payment methods for security.

The period between the 2015 and 2017 studies showed a significant shift in consumer credit card payment.: In 2015, 59 percent of credit card holders reported an unpaid balance of revolving debt, but by October 2017, that figure had dropped to 54.5 percent.

Perhaps surprisingly, given the rise of technology for smartphones, the use of non-bank payment accounts such as PayPal remains low, and the stability of payment methods used by consumers over the last 10 years demonstrates a slowness to adapt to change.