The Federal Reserve just released its report on household debt, which reached $16.51 trillion in the 3rd quarter. Total debt rose $351 billion versus the previous quarter, representing the most significant quarter-over-quarter increase since 2007. Mortgage debt represents 71% of the total increase, or $282 billion. But the big story in the debt report was credit card debt, which increased 15% over a year ago. This increase represents the largest increase in credit card debt in over 20 years.

WHAT’S DRIVING CREDIT CARD DEBT

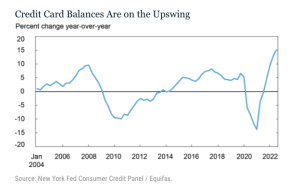

Credit card debt fell during the early portion of the COVID pandemic. But as we look at 2022, we see a relatively rapid increase in the credit card debt level, as seen in the chart below.

- New debt linked to fresh consumption

- Revolving or carry-over debt from previous months

There are over 500 million open credit card accounts, making this vehicle the most prevalent type of consumer debt in the U.S. Concerning overall credit card usage:

- 191 million Americans have at least one credit card

- Half of all Americans have multiple credit cards

- About 13% of Americans have five or more credit cards

- Credit card usage starts young; 73% of Americans have an open credit card account by the age of 25.

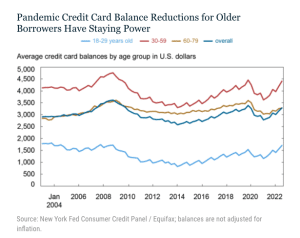

CREDIT CARD BALANCES AND AGE DEMOGRAPHICS

The chart below breaks out credit card balances based on three broad age groups. Here’s what we see:

- Credit card balances for the most significant spending demographic, 30-59, have risen steadily and are now at pre-pandemic levels. This age group saw the most dramatic decrease in credit card spending in the early months of the pandemic.

- Balances for the oldest demographic, 60-79, have risen steadily in recent quarters but still fall below their pre-pandemic levels.

- Younger borrowers under 30 saw a minor reduction in spending during the pandemic, but their credit card spending now exceeds pre-pandemic levels.

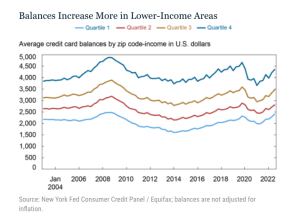

The Fed then looked to see if income had any bearing on credit card usage and balances. NOTE: Because the Fed does not access borrower income information, they use borrower zip codes to break them into equal population income quartiles. Here’s what we see below:

- All income groups exhibited similar credit card usage patterns in the months following the onset of the pandemic and the subsequent two years.

- The highest income quartile experienced the most significant decrease in credit card balances in the early months of the pandemic. Balances for this group are still below pre-pandemic levels. A reference point here: higher income groups are less likely to have revolving credit card accounts. As such, the Fed speculates that this group’s steep drop in balances is likely a function of reduced consumption, especially during the height of the pandemic.

- There was a modest reduction in average balances during the pandemic for the lowest-income group. But the balances for this group have increased steadily in the previous two years and now exceed pre-pandemic levels.

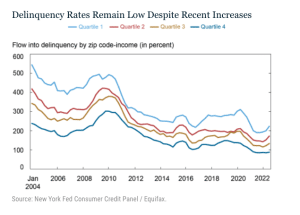

- Delinquency rates are gradually increasing. But it’s important to recognize that these increases are coming off of low levels that we saw during the pandemic.

- Across all groups, delinquency rates are dramatically lower than during the Great Recession.

Naturally, this scenario raises concerns that we will see a rise in delinquencies. But, on the flip side, the modest delinquency rates of recent years (especially in comparison to historical trends) suggest that American consumers, in general, are doing a better job of managing their finances. Thus, we have cause for cautious optimism.

SOURCES

To learn more about the RDS and our approach to Master Servicing, contact: Kacey Rask : Vice-President, Portfolio Servicing

[email protected] /513.489.8877, ext. 261