For the last few posts, we’ve examined the 2018 Fair Lending Report given to Congress by the Consumer Financial Protection Bureau and, specifically, issues surrounding consumers with little to no credit.

We’ve tackled the rural vs. urban divide and what products “credit invisibles” use to enter the market.

In our final installment of the series, we investigate how access to traditional banking services and brick-and-mortar institutions affect the credit invisibles, regardless of their geography.

If access to traditional banks matters for credit invisibility, then the high levels of credit invisibility in rural areas and lower-income areas of metropolitan statistical areas (MSA) might reflect this lack of access.

This result is consistent with the idea of credit deserts—geographic areas with little or no access to traditional lenders—being a cause of credit invisibility.

The CFPB studied whether proximity to banks is a factor in the frequency with which people use credit cards as their entry products or in the incidence of credit invisibility.

The study pinpointed the bank branch that was closest to the center of each Census tract using bank branch locations from the FDIC’s Summary of Deposits data.

If proximity to a depository was an important factor in obtaining a credit card, then one might expect the use of credit cards as an entry product to be higher among consumers for whom the distance to the nearest branch is shorter. The CFPB study showed that among people in MSAs who transitioned out of credit invisibility before turning 25, the use of credit cards as an entry product does decline with distance.

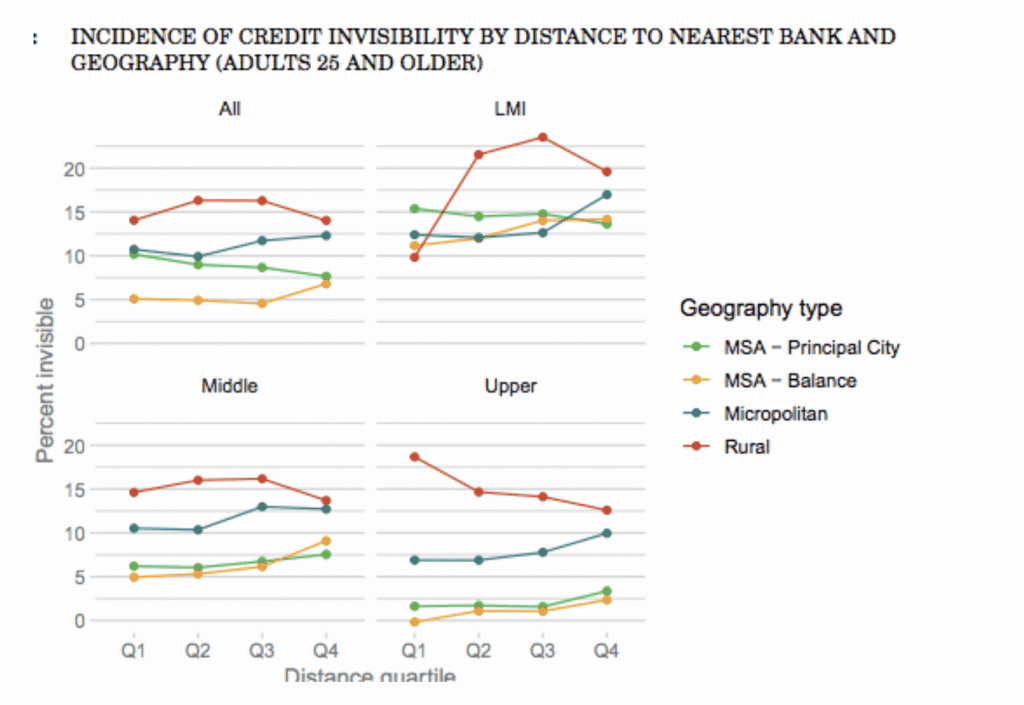

The graph below shows the relationship between the incidence of credit invisibility and branch distance among adults 25 and older. The upper-left panel shows the pattern across all tract relative income levels and the other three panels show the pattern for each income level separately.

If proximity to financial institutions was an important factor in access to credit, the lines should be upward-sloping, reflecting a higher incidence of credit invisibility at greater distance. Instead, there appears to be little relationship between distance to the nearest

branch and the incidence of credit invisibility.

Similar patterns are observed for each relative income level. These results provide little evidence that bank branch proximity is an important factor in explaining why consumers are credit invisible.

Nevertheless, they are consistent with data from the Federal Deposit Insurance Corporation’s National Survey of Unbanked and Underbanked Households finding that proximity to a bank is one of the less common reasons that consumers remain unbanked. When respondents without checking or savings accounts were asked why they did not have an account, only nine percent cited “inconvenient locations” as a reason and only two percent identified it as the main reason for not having an account.

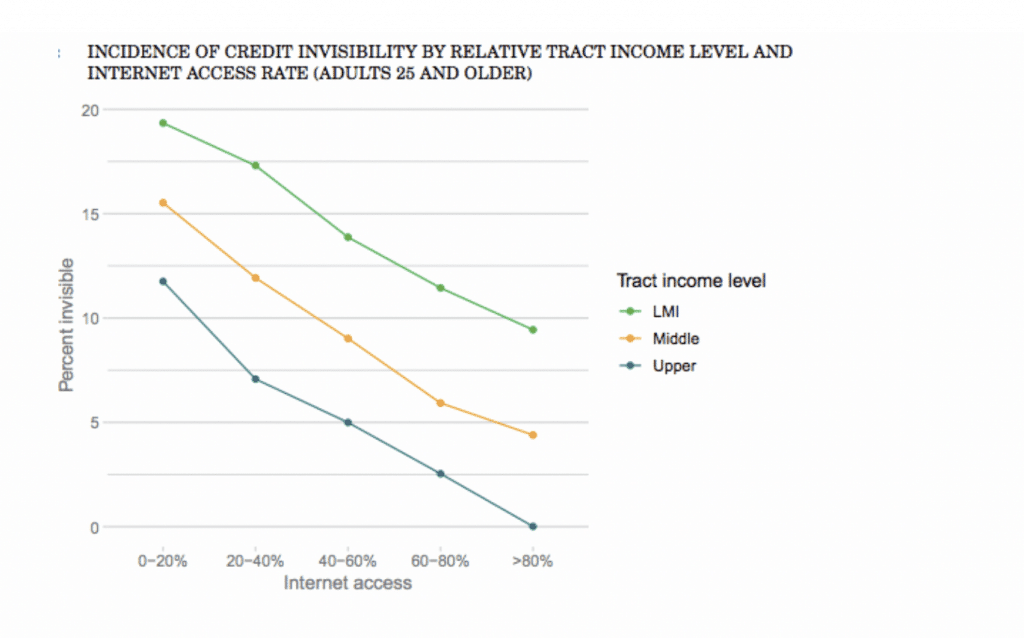

One factor that might reduce the importance of a nearby bank branch is easy access to the Internet. This is particularly true for credit cards, where applications tend to be made online.

According to the Federal Communication Commission’s Internet Access Services Report, the incidence of credit invisibility is consistently higher in tracts where fewer households have high-speed internet, a pattern observed for all three tract income levels. This is borne out by the chart found below.

While this relationship is not necessarily causal, credit invisibility is more prevalent in areas with less digital access to traditional financial service providers.

SOURCE