One of the most daunting challenges facing the U.S. economy is the rising tide of student loan debt. According to the New York Federal Reserve Bank:

- Student indebtedness increased by more than 170% in the decade from 2006 to 2016.

- About 5% of borrowers have more than $100,000 in debt but account for 30% of the total debt.

- Recent graduates with student loans leave school with an average debt of $34,000, up 70% in the past decade.

Of course, with this level of debt, we are seeing an increase in the level of defaults on these loans. According to the New York Fed, of those students who left college in 2010 and 2011, 28% defaulted on their loans within five years. This compares to a 19% default rate for those who left school five years earlier.

In November of last year, the Fed issued an analysis entitled “Who Is More Likely to Default on Student Loans?” In this post, we’ll summarize that November analysis.

The Fed study focused on individuals born between 1980 and 1986. It tracked both their college attendance and student loan default status by age. The study posed five questions with regard to student loan defaults:

- Do default rates differ by college type?

- How do default rates of dropouts compare to those of graduates, and does this relationship vary by degree program?

- Does default vary with college major?

- Does college selectivity matter for this relationship, and for student loan default more generally?

- Are students from less advantaged backgrounds more likely to default than students from more advantaged backgrounds?

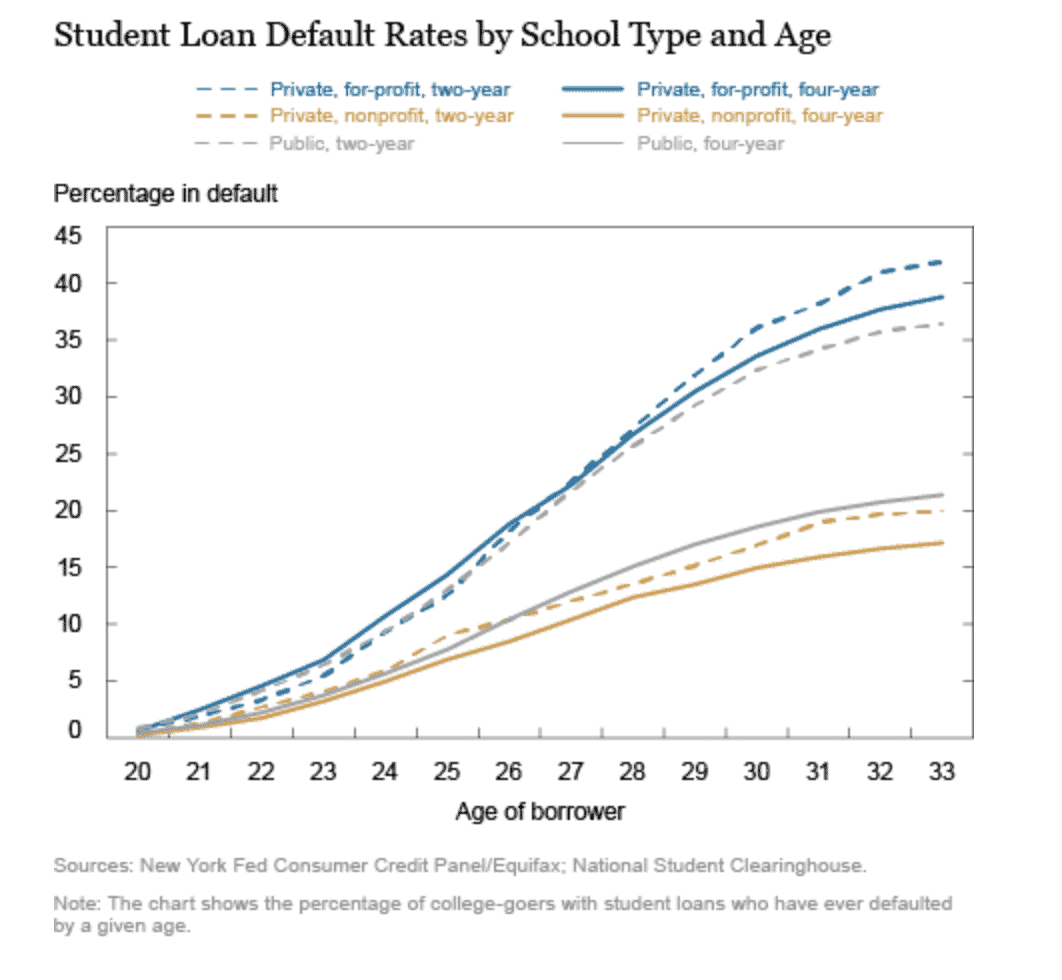

DEFAULT BY COLLEGE TYPE

The chart below looks at student loan defaults across six variables, covering both private non-and for-profit schools as well as public schools.

Here’s what we see:

- Students who attended private, for-profit institutions have the highest default rates once they reach their mid-twenties.

- Students who attended private, not-for-profit schools have the lowest default rates.

- Regardless of the type of school, two-year students have higher default rates than four-year students.

- Interestingly, the default rates between two-and four-year private college students are less than five percentage points at age 33. By contrast, the default rate for public community college students (two-year) is nearly 25 percentage points higher than those with a four-year, public college degree.

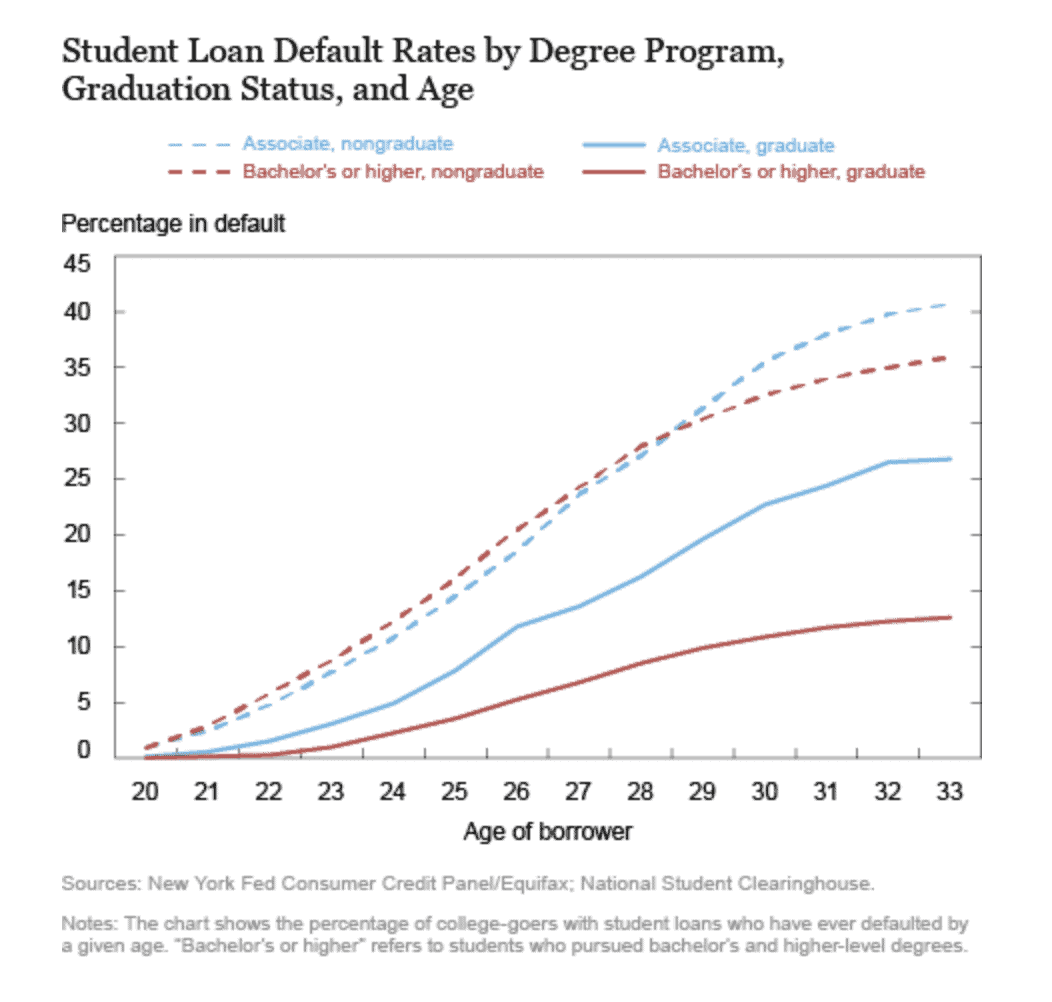

DEFAULT BY GRADUATION STATUS AND TYPE OF PROGRAM

Next, the study looks at how graduation status and type of program is linked to student loan defaults:

As with much of this study, the results are not surprising:

- Whether from a bachelor’s or associate’s degree program, students who drop out are significantly more likely to default on loans than those who graduate.

- Among graduates, students with associate’s degrees default at higher rates than their counterparts with bachelor’s degrees.

- The default rate gap between two- and four-year graduates continues to increase with age (13 percentage points by age 33).

Clearly, the premium paid for a four-year bachelor’s degree pays dividends, especially with regard to minimizing the likelihood of defaulting on a loan.

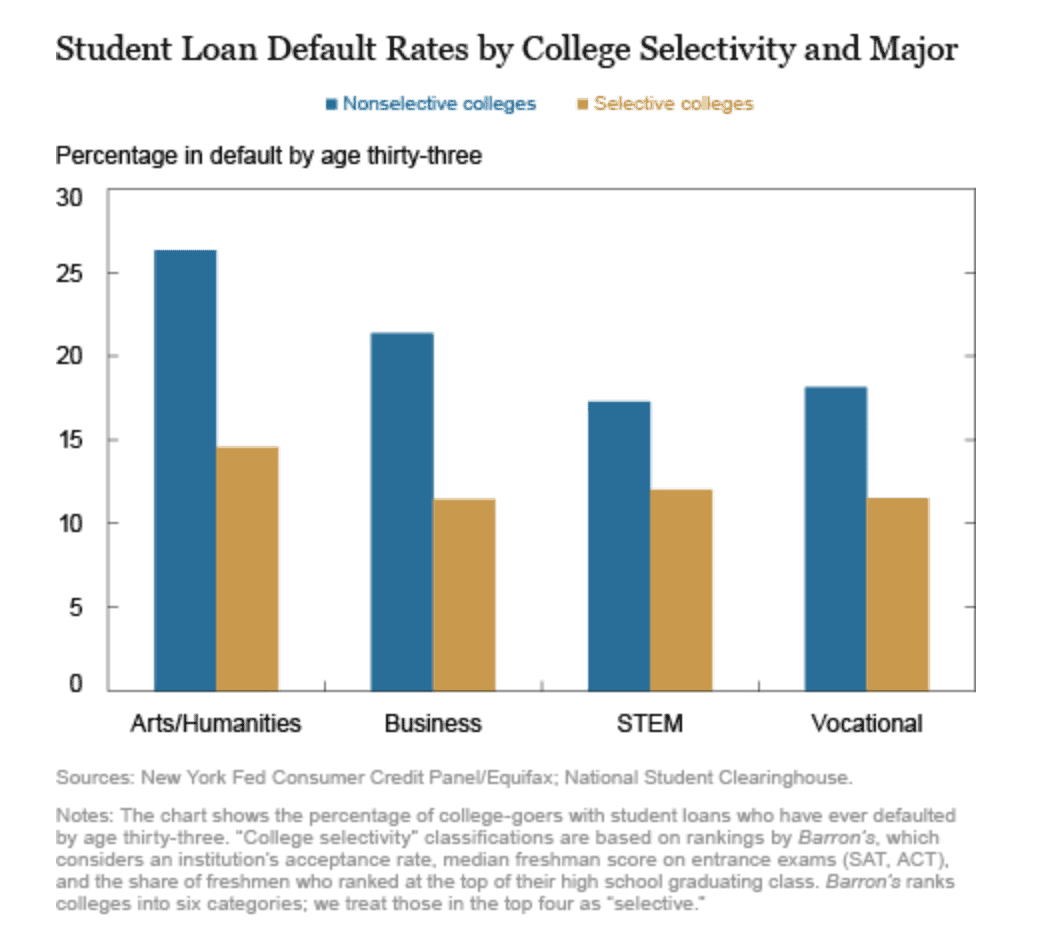

DEFAULT BY COLLEGE SELECTIVITY AND MAJOR

This next chart blends two sets of variables:

- Selectivity: based on Barron’s Profile of American Colleges, the Fed looked at “selectivity” by breaking four-year colleges into two categories:

- Selective colleges, which were ranked as “competitive” by Barron’s

- Non-selective colleges

- Major: students were also classified into one of four broad categories

- Arts and Humanities

- Business and Law

- STEM

- Vocational

Here’s what we learned:

- Arts and Humanities majors default at than other types of graduates.

- STEM graduates default at the lowest rate, but it is not a much lower rate than that for Business and Vocational graduates.

- Students attending non-selective colleges have higher default rates no matter what their major.

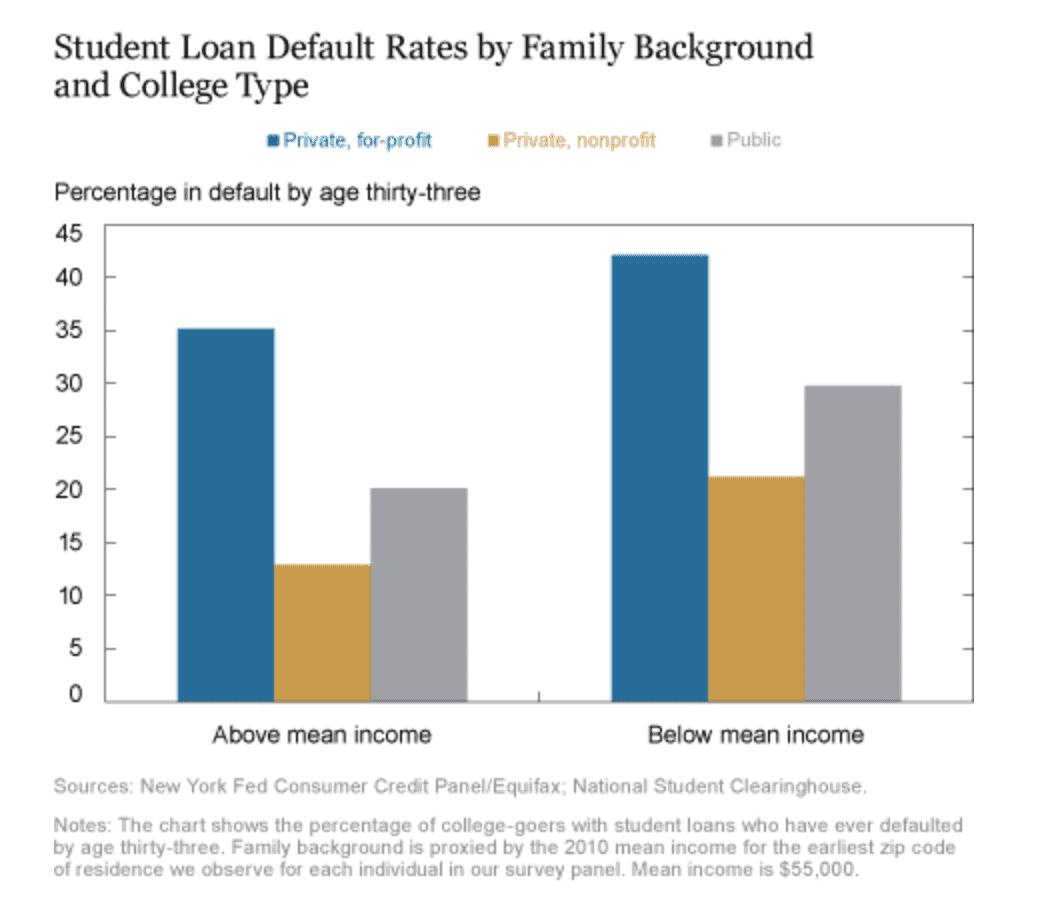

DEFAULT BY FAMILY BACKGROUND AND COLLEGE TYPE

The final set of variables reviewed in this study was family background, specifically family income. Individuals were categorized based on the average 2010 income in the zip code in which they resided, leading to two panels: those from areas with an average income above $55,000 and individuals from areas with an average income below $55,000.

This analysis revealed the following:

- Within each college type, students from less-advantaged backgrounds have higher default rates than students from more advantaged areas.

- There is almost a 30 percentage point difference between the group with the highest default (private, for-profit students from less advantaged areas) and the lowest default rate (private, not-for-profit students from more advantaged backgrounds).

- Interestingly, public college students from more advantaged backgrounds default at nearly the same rate as private, not-for-profit students from less advantaged backgrounds.

Across the board, attending a four-year private, for-profit college correlates most strongly with the likelihood of defaulting on student loans. Dropping out is the second strongest variable related to defaults.

The long-term implication, of course, is that “life outcomes,” such as the ability to buy a home and also maintain a healthy credit score, will vary greatly among student loan holders based on their educational choices and family backgrounds.

SOURCE