The term “sub-prime loan” carries a lot of baggage in our economic lexicon since defaults on sub-prime mortgages helped fuel the Great Recession of 2008-2009. As a fall-out of the financial crisis, regulators took steps to rein in the use of sub-prime mortgages in order to minimize the risk of another collapse. Still, we are seeing a rise in the use of various forms of security-backed mortgages again

But there is another type of sub-prime market that is growing at a dramatic rate, yet getting very little attention: sub-prime auto loans. According to Wells Fargo, $26 billion worth of sub-prime auto-bonds were sold in 2016-more than a ten-fold increase over the $2.5 billion sold in 2009.

A LITTLE ABOUT SUB-PRIME AUTO LOANS

Similar to a sub-prime mortgage, a sub-prime auto loan allows people with sub-standard credit scores or limited credit history to secure a loan on a new vehicle.

Experian estimates that more than one-third of U.S. car purchases are now financed with sub-prime loans. These loans carry significantly higher interest rates, longer terms and often include pre-payment penalties. Let’s compare:

- The average loan for a sub-prime borrower (credit score range: 501-600) carries an interest rate in excess of 10% with terms extending to 72 months.

- Prime borrowers (600-780) pay less than 4% with terms extending to about 69 months.

Perhaps most disturbing is the growth in deep sub-prime loans, those given to consumers with credit scores below 500. Experian estimates that this category of auto loan has grown at a rate of 14.9% over the past year.

Sub-prime auto loans now make up about 16% of the overall auto-loan market.

TROUBLE ON THE ROAD AHEAD?

CNBC estimates that nearly 9 out of 10 new car purchases in the U.S. are financed through leases or other types of loans. Today, there are more than $1 trillion in outstanding auto loans. The market is being fueled by a number of factors:

- Continued low interest rates

- Low unemployment

- Aggressive manufacturer marketing

- Increased dealer and manufacturer price incentives

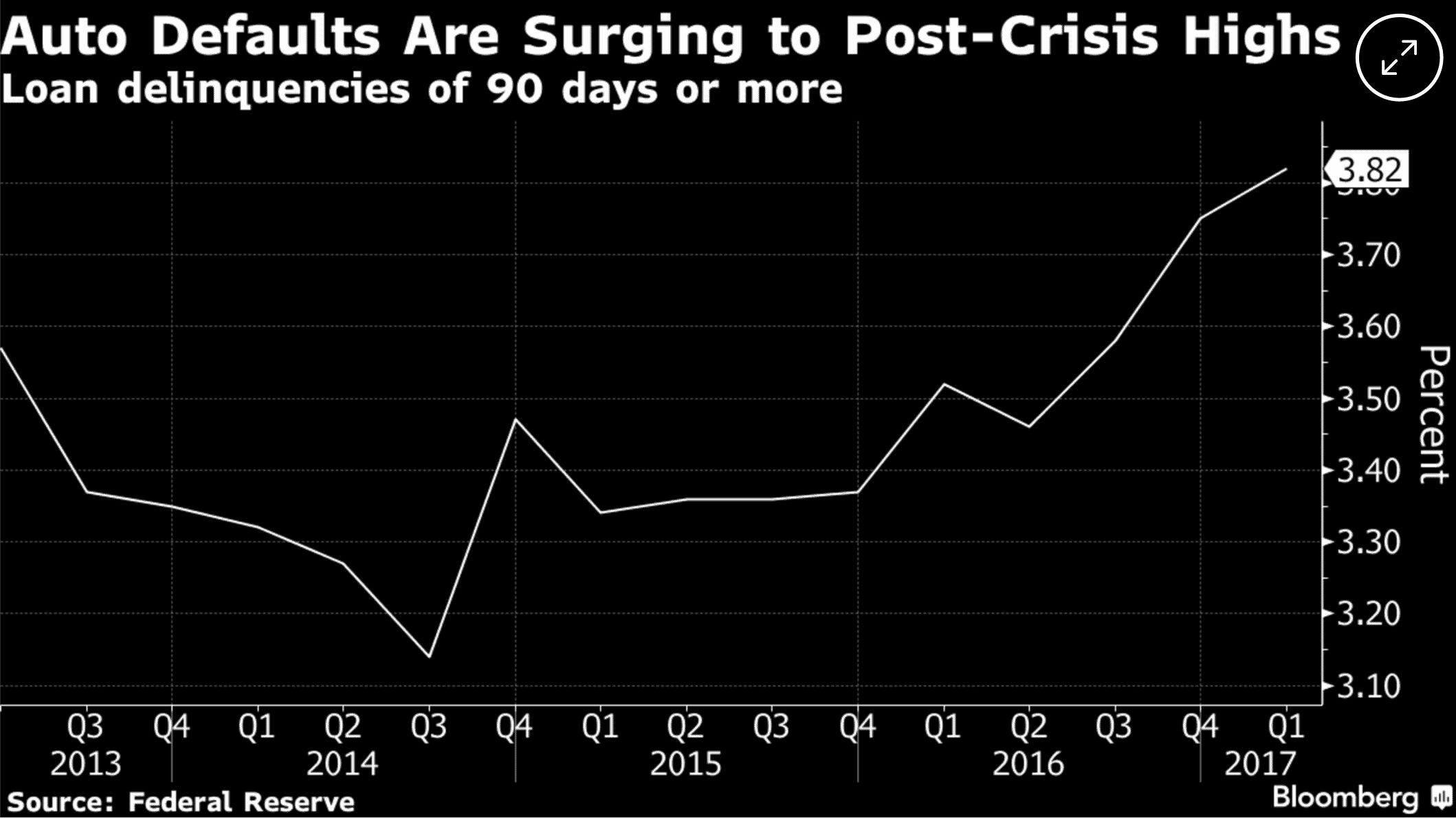

Unfortunately, as more people are borrowing to buy new cars, we are seeing a surge in the number of defaulted auto loans. Since 2010, auto loan delinquencies are up more than 50%. In fact, of the 11 loan categories tracked by the American Bankers Association Consumer Credit Delinquency Bulletin, auto loans have shown the greatest level of delinquencies in recent years.

The increase in sub-prime and even deep sub-prime loans is a major culprit in the rise in delinquencies. People without the means to pay are being enticed into the showrooms and approved for loans at exorbitant terms as outlined above. These are often consumers who are financially stretched on all fronts and are one missed paycheck away from financial disaster.

Exacerbating this problem is an increase in the level of fraud being perpetrated in the auto loan process. According to Bloomberg, as many as 1% of auto loan applications include some type of material misrepresentation, and this rate is rising. While this level may seem insignificant, it’s worth noting it approximates the level of loan application fraud we saw during the lead up to the mortgage crisis. The most common types of fraud are related to details about employment and family or personal income. However, loan application fraud isn’t limited to the consumer. In their zeal to close a deal, dealers can also falsify information on a loan application, such as the type of vehicle purchased and the value of that vehicle.

As the table below details, auto loan delinquencies have surpassed the levels seen during the post crisis period.

ECONOMIC IMPACT: IS THIS A CRISIS?

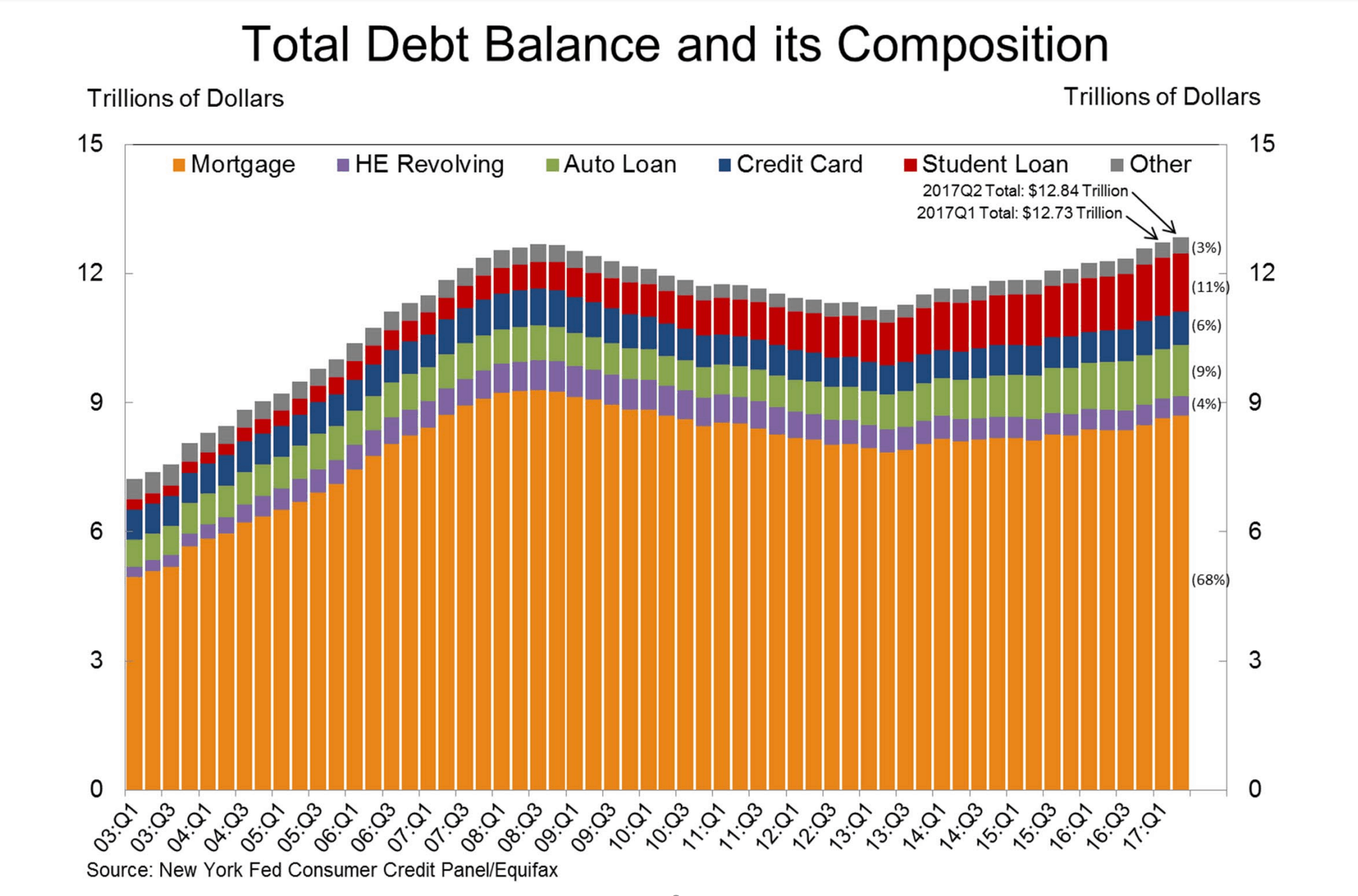

As mentioned earlier, it was sub-prime mortgages packaged into investment securities that triggered that financial collapse in 2008. Sub-prime auto loans are now similarly packaged into investment securities. As the level of auto loan defaults increases, there is rising concern about the stability of these auto loan securities. However, analysts are quick to point out that because auto loans represent less than 10% of household debt (see table below), a crisis in the sub-prime auto loan market is unlikely to impact the global economy as did the housing collapse in 2008.

Look for future posts on developments in the auto loan market.

SOURCES:

https://www.cnbc.com/2017/06/07/lenders-hit-the-brakes-on-subprime-auto-loans.html

http://www.businessinsider.com/subprime-auto-loans-are-a-reminder-of-the-housing-crisis-2017-4

https://www.cnbc.com/2017/06/12/auto-loan-delinquencies-rise-as-drivers-splurge-on-pricey-cars.html

https://www.newyorkfed.org/microeconomics/hhdc.html