In July of this year, the Federal Reserve Bank of New York issues a staff report entitled: Echoes of Rising Tuition in Students’ Borrowing, Education Attainment and Home Ownership in Post Recession America.

While, understandably, much attention is paid to the absolute level of student loan debt (now surpassing $1.2 trillion), little is written about how this debt is impacting other aspects of the economy. The Fed’s study attempts to shed light on the subject by focusing primarily on the relationship of student debt and borrowing to post-education living circumstances.

A 21st CENTURY SNAPSHOT

To provide context to this issue, the study begins with a summation of the significant changes young consumers have faced since the turn of the century:

- Student loan debt has grown nearly four-fold, going from $360 billion in 2004 to more than $1.2 trillion in 2016.

- Homeownership among those 30 and younger has fallen from 31 to 21% during the same period.

- About one-third of 23-25-year-olds lived with their parents in 2014. As of 2016, that number had grown to 44%.

Let’s walk through the key findings of the study

REALLOCATION OF DEBT

From 2003 to 2015, we see a dramatic change in the credit report of a representative 30-year old:

- Home-secured debt: -28%

- Auto-loan debt: -6%

- Credit card debt: -36%

- Student loan debt: +174%

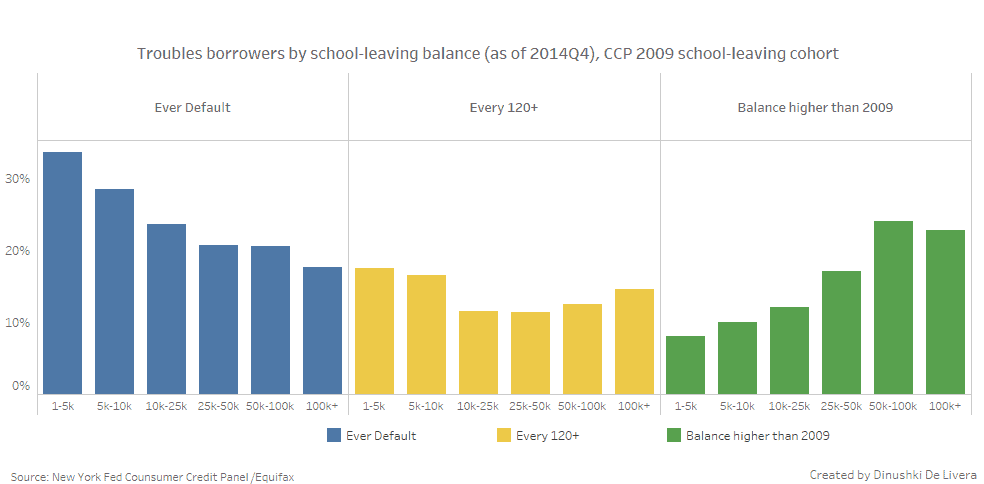

REPAYMENT CHALLENGES

As relates to repaying this massive debt, it’s interesting to note the relationship between the amount borrowed and related repayment challenges. As you’ll see in the chart below:

- Repayment struggles are most common with low balance borrowers ($1,000-5,000) and high balance borrowers ($50,000+).

- The most successful re-payers have moderate balances, between $10,000-25,000. But even within this group, as many as 40% falls behind on payments or become severely delinquent.

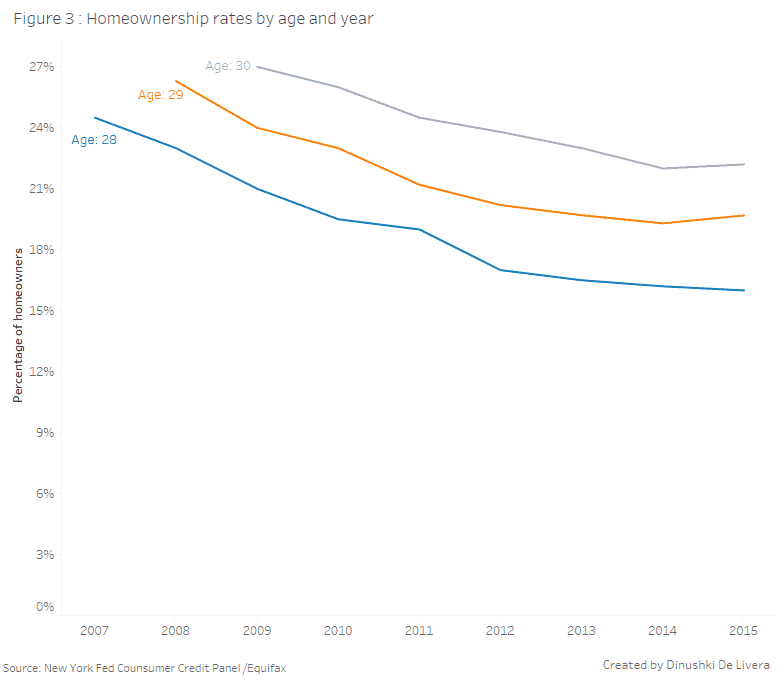

HOME OWNERSHIP PATTERNS

The study correlated home ownership patterns of consumers in their late 20s. The authors inferred home ownership based on the presence of home-secured debt on the consumer’s credit report.

Between 2007 and 2015, home ownership among 28 year olds declined from 24.4% to 16%. This translates to an annual rate of decline of 0.94%. The report identified similar rates of decline in both 29 and 30-year old adults.

The chart below breaks out the trends for this period:

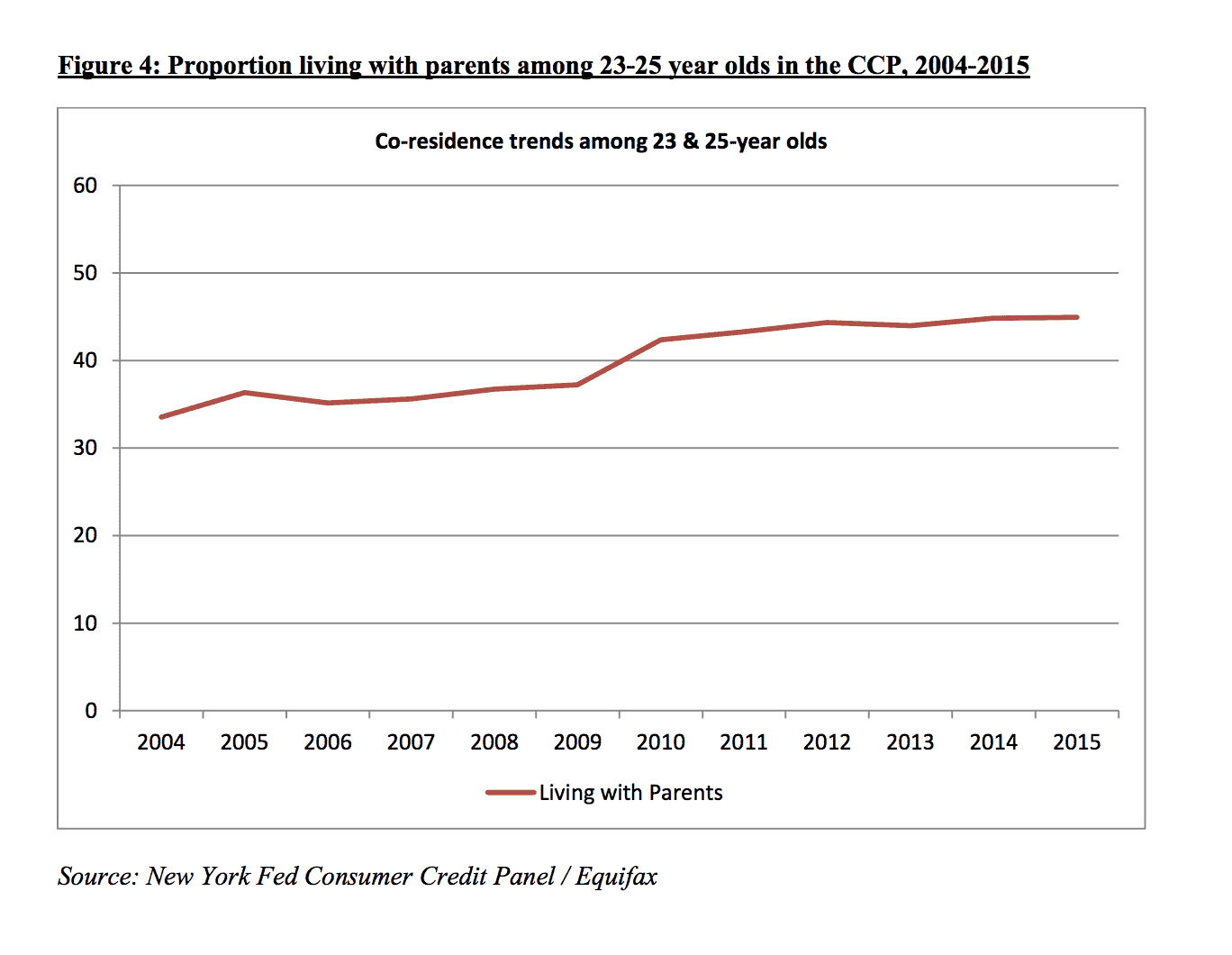

LIVING AT HOME

As home ownership has declined, young Americans are choosing to live with their parents. As the chart below indicates, about 1/3 of 23-25-year-old adults lived with their parents in 2004. Today, that number is approaching 50%:

The report closes with a warning to states that continue to increase state tuition:

The results suggest that states that increase college costs for current student cohorts can expect to see a response not through a decline in workforce skills, but instead through weaker spending and wealth accumulation among young consumers in the years to come.

Indeed, there is a clear ripple effect with rising tuition that extends well beyond the issue of student loan debt. In future posts, we will explore other aspects of student debt in more detail.

SOURCE: