In our third installment of the Consumer Financial Protection Bureau’s 2018 Fair Lending Report to Congress, we further examine issues keeping consumers ‘credit invisible’ and will look at products by which those people enter the credit market.

As we discussed in our last post, credit invisibility is persistent in rural areas, regardless of income, and lower-income urban areas, and now we look at the differences in the means by which consumers in these locations first establish their credit histories.

An earlier report by the CFPB, “Becoming Credit Visible,” documented that credit cards are the predominant “entry products,’ or the first reported item establishing a credit record, consumers used to transition out of credit invisibility.

The CFPB studied how the propensity to use credit cards as entry products varies among geographic areas, specifically among consumers who transitioned before turning 25.

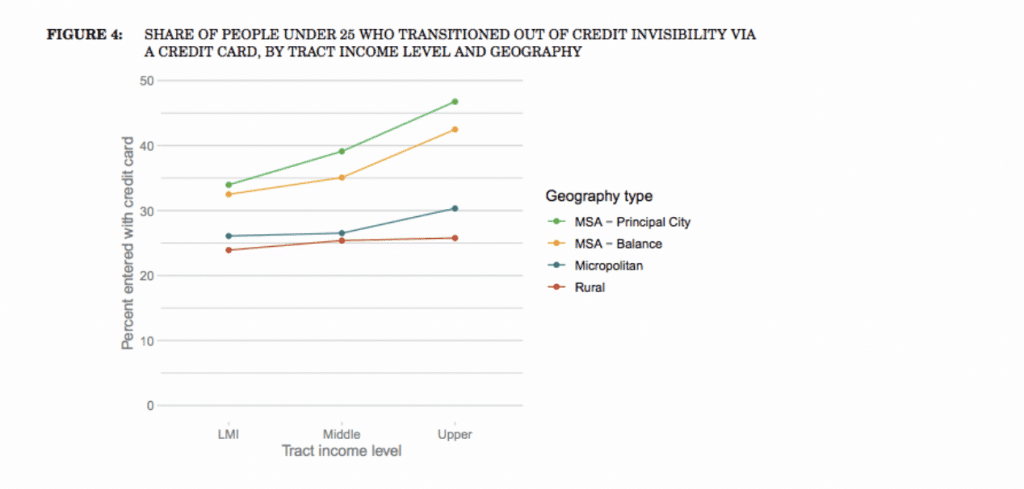

The figure below shows the share of consumers younger than 25 whose entry product was a credit card and transitioned out of credit invisibility.

There are two notable patterns shown in the graph. First, the upward-sloping relationship between neighborhood income and the likelihood of establishing a credit card is much stronger in MSAs than it is in Micropolitan or rural areas. In contrast, outside of MSAs, the relationship is flatter, much like the overall relationship between the incidence of credit invisibility and neighborhood income in these areas.

Second, the overall rate of using a credit card as an entry product is about 10 percent lower outside of MSAs than compared to within MSAs. The significant variation in credit card use as an entry product across geographic areas might be surprising.

Credit cards are often marketed directly to consumers through the mail, television, or online and do not have to be applied for in person. This suggests that credit cards should be as accessible to people in rural areas as they are in MSAs. Nevertheless, the 2015 National Survey of Unbanked and Underbanked Households from the Federal Deposit Insurance Corporation suggests that consumer credit card use may be closely tied to other services that banks provide locally. That data shows only seven percent of unbanked consumers, those without a checking or savings account, report having had a credit card in the past 12 months. This is significantly lower than the 58 percent of banked consumers with credit cards.

There are many potential reasons why people who do not use banking services are less likely to hold credit cards, such as lower income or comfort with using financial services.

It is possible that when credit card lenders make decisions about credit-invisible applicants, they may be more willing to extend credit to those with whom they have an existing deposit account relationship. If so, the problem of credit invisibility may be closely related to a lack of access to traditional banking services.

In our next – and final – installment of this series, we will examine the role of traditional brick and mortar financial institutions helps invisibles transition to a credit history or similarly prevents from credit documentation.

SOURCE