We recently began posting our predictions for quarterly loan charge-off rates. Check out our most recent post HERE.

We’ll continue this series throughout 2017 and beyond

In today’s post, we’ll take a snapshot of what to expect on both the credit card and residential real estate fronts.

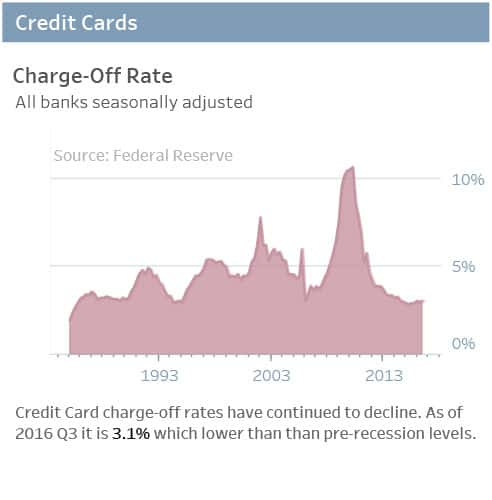

CREDIT CARD CHARGE OFF RATES

As of the 3rd quarter, 2016, the credit card charge-off rate stands at 3.1%, which is near its historic lows. As you can see from the table below, the charge-off rates have continued to decline since their Great Recession peak of 6.8%, in Q2, 2009, but recently have started to trend up.

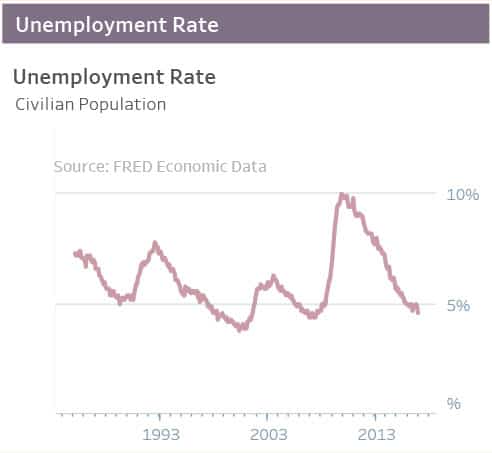

As we expected, charge-off rates have started edging up in 2017, based on two factors. First, despite the recent Federal Reserve interest increase, we believe creditors will continue to loosen lending policies. Second, the unemployment rate should continue to fall as more baby boomers retire. As you can see below, the current rate is 4.6%.

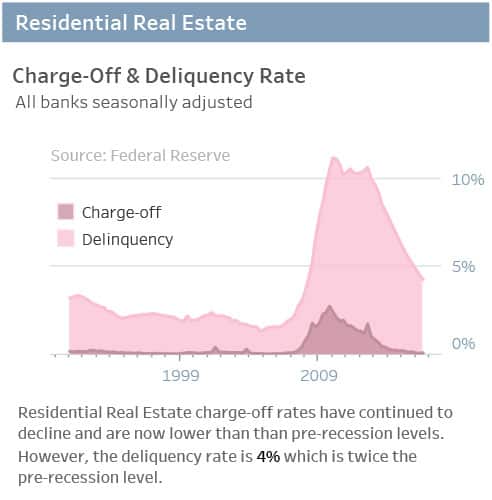

REAL ESTATE CHARGE OFF AND DELINQUENCY

Residential real estate charge-off rates have continued to decline and are now lower than pre-recession levels. On the flip side, the delinquency rate of 4% is still higher than the pre-recession levels. For perspective, from the mid-50s through the early 2000s, residential real estate delinquency rates were in the 2% range. As you can see from the table below, while dramatically improved from the recession peak of 11.2% in Q1 2010, the current level is at a rate nearly double that for the two decades preceding the recession.

As for the future, we anticipate that both residential real estate charge-off and delinquency rates will increase as a result of several factors. First, as shown in the table below, new privately owned housing starts will continue to increase, hitting 1.1 million in 2017. Second, mortgage rates, while possibly edging up, are still at extremely attractive rates. Third, lending policies are expected to loosen slightly in the coming year. It’s possible that the Federal Housing Authority may reduce fees for first-time buyers. Also, government-owned mortgage companies are expected to begin backing larger mortgages for the first time since the Great Recession.

Of course, the one thing we can’t predict at this point is if and how financial and credit markets will be impacted by policy changes from the new administration. Regardless, we’ll continue to post our quarterly charge-off and delinquency projections in this blog.