In our prior two posts, we’ve addressed the concept of wealth disparity between blacks and whites by reviewing studies from the Federal Reserve Bank of Cleveland. In this one, we wrap up the series by examining a model for the persistency of this gap.

Most models are between observable characteristics and wealth estimated over short periods of time, thus likely underestimating the importance of initial conditions and income disparities for future wealth.

In a model the Cleveland Fed constructed, households have many motivations for saving, including retirement and to insure against sudden fluctuations against labor income. The model makes predictions about types of wealth gaps, questions if the observed racial income and wealth gaps are compatible with each other, and which factors make the largest contribution to the racial wealth gap.

One factor accounts for the racial wealth gap almost entirely by itself: the racial income gap. The Fed results stand in contrast to the results of earlier studies that focus on a single point in time and find that the wealth gap is too large for the income gap to explain. The Fed study comes to a different conclusion from earlier ones in that it accounts for the dynamic nature of wealth accumulation.4

Let’s explain how the labor income gap accounts for the racial wealth gap. First, the model predicts that, starting from 1962, it would take 259 years for the ratio of black and white mean wealth to reach 0.90.

Second, changing the labor income gap in the model changes the wealth gap dramatically. For example, when the labor income gap is removed, meaning black and white households immediately earn the same income from their labor from 1962 onward, the black-to-white wealth ratio reaches 90 percent by 2007.

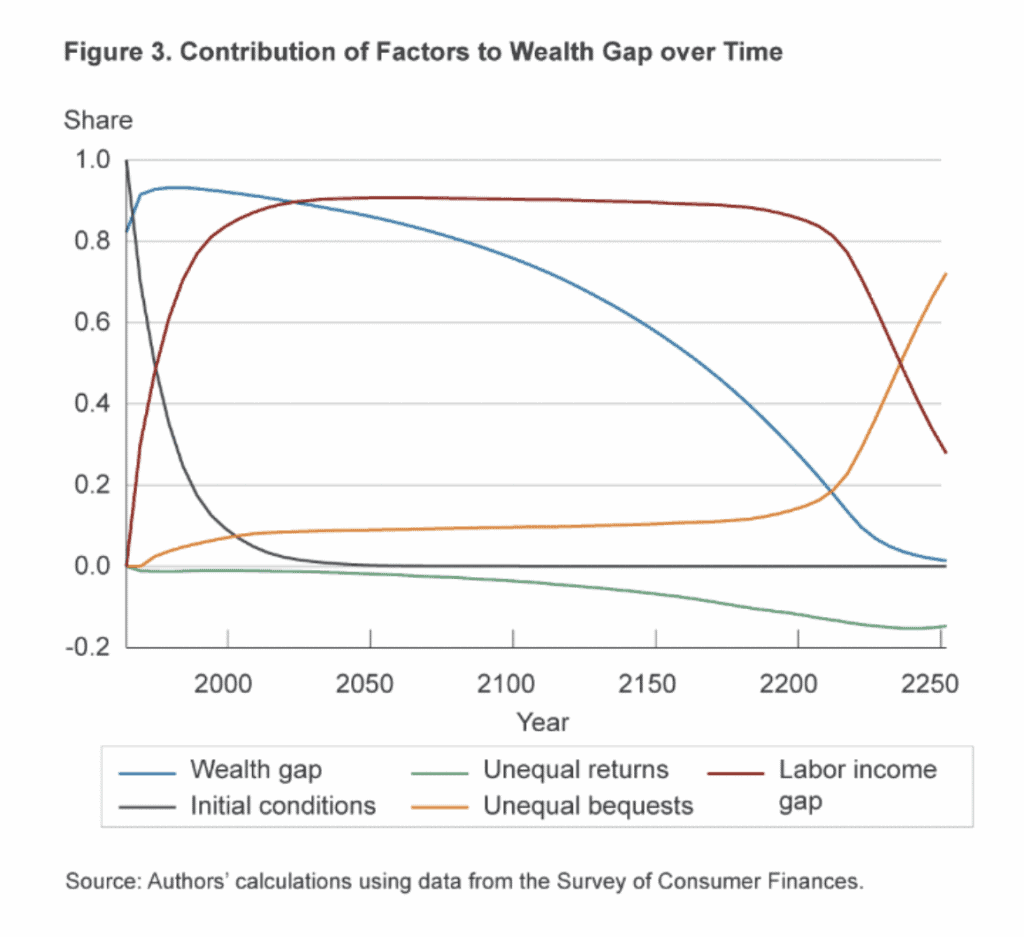

Figure 3 deconstructs the wealth gap at each point in time into its contributing factors. Not surprisingly, initial conditions play an important role early on. Regardless of the different factors tested, it takes time to undo the extreme racial wealth inequalities. Over time, however, the model puts less weight on the initial disparity for propagating the racial wealth gap and more weight on persistent systemic differences in economic opportunity. The model predicts that by 1977 the gap in labor income was a larger contributor to the wealth gap than initial inequality, and by 1990 the labor income gap accounts for more than 80 percent of the wealth gap. That gap remains the dominant factor until far in the future, when the racial wealth gap is nearly closed.

The Fed analysis supports the conclusion that the racial labor income gap is the primary driver behind the large and persistent difference in average wealth between black and white households.

SOURCE