In the third installment of our series on Financial Invisibles, we examine the characteristics that make up the top two tiers broken out in the August 2017 study conducted by Unifund and PYMNTS.com.

Despite the tag “No Worries,” this group, at the top of our four categories, is still considered invisible, because they have the means but not the willingness to participate in the financial system. The “Second Chances” category, which includes those who have had delinquencies but can still opt into traditional financial tools, has many characteristics in common with the bottom two tiers nonetheless.

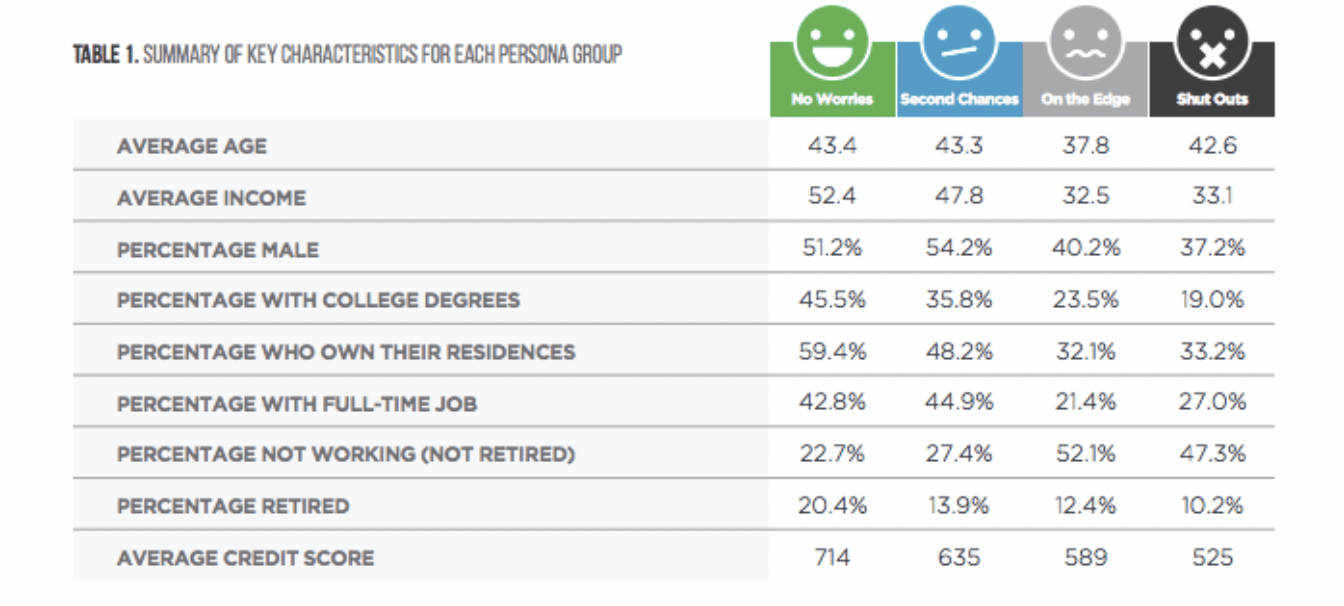

Bear in mind all the 2,000-plus people sampled for the survey mirror the total U.S. population in terms of income with 70 percent of the sample making $50,000 or less a year and 40 percent coming in at less than $25,000.

The chart below gives the clearest picture of who makes up the No Worries and Second Chances groups: both groups are much more likely to be male, have college degrees, and own their own residences – the last two being traditional markers of success in America – than the bottom group, the Shut Outs. But, there is a significant drop off in credit score as well as homeownership and college degrees between No Worries and Second Chances.

Given the above traits, it’s not surprising that No Worries is the group that is most invested in traditional financial systems or has been at some point. We noted in the first segment of this series that 98 percent of No Worries have or have had a bank account at some point and 92 percent of Second Chances have, compared to 50 percent of On the Edge and 66 percent of Shut Outs.

Similarly, more than 65 percent of the top two categories have owned credit cards, a vastly higher proportion than the other two, with only four percent of Shut Outs and 30 percent of On the Edges holding credit cards. Ninety-nine percent of the No Worries group reports paying bills on time.

On the face of these facts, it would appear neither of the top tier groups has much to worry about, so we should examine why they aren’t participating in the financial system; all facts in the study point to them being able to do so.

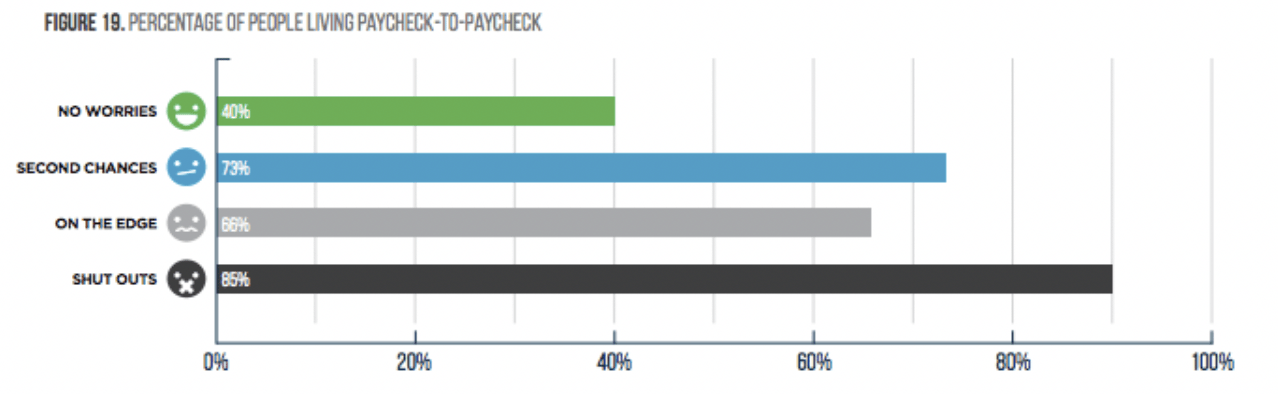

The key factor is that, across the entire sample, 60 percent of respondents say they live paycheck to paycheck. While No Worries falls far below the other categories, still 40 percent of that group is living paycheck to paycheck, on the verge of being financially derailed by one unplanned-for expense. Surprisingly, more Second Chances – 73 percent – than On the Edge – 66 percent live in fiscally precarious conditions.

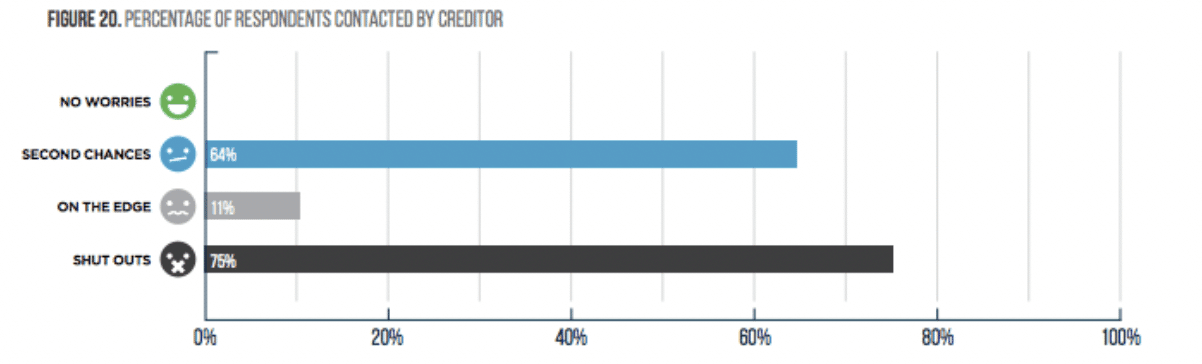

The greatest measure for the definition of each group may be how often each reported being contacted by creditors. Literally, not one person who fits into the No Worries group reported ever being contacted by a creditor; paying bills in on time is the hallmark of this group.

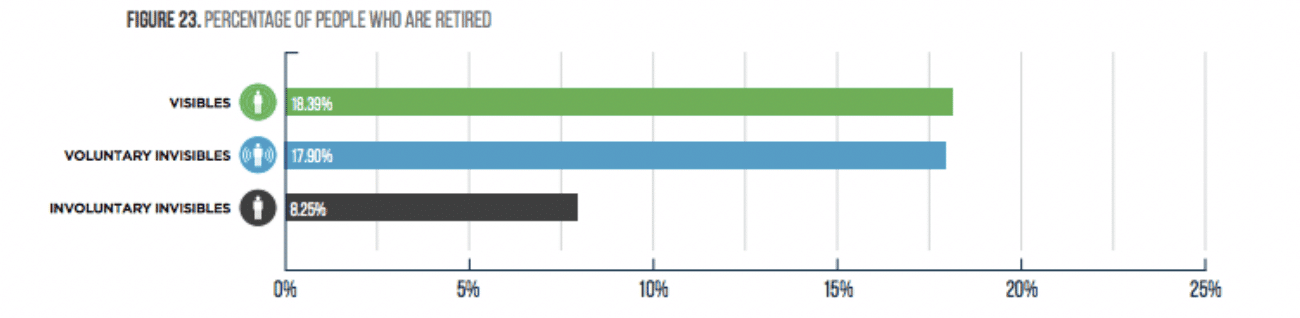

Thus, the No Worries and the Second Chances fit into a larger category of Voluntary Invisibles, unlike the Shut Outs, who may want to be part of the financial system but are prohibited by past delinquencies and are Involuntary Invisibles. Judging from the study, as demonstrated below, retirement is a significant factor for the Voluntary Invisibles. Just over 18 percent of Visibles and just under 18 percent of Voluntary Invisibles are retired, showing that living on a fixed income could be a factor in use of traditional financial products.

In our fourth and last installment of the series, we will examine the study update completed in first quarter of 2018 to compare what changed for respondents since the third quarter 2017 original study.