Americans love perfection. We all remember resenting the kids who got a perfect score on their SATs.

Today’s credit-conscious consumers are focused on a new benchmark for perfection: a FICO score of 850. People have become obsessed with improving their “number.” As a reminder, FICO is a type of credit score created by Fair Issac Corporation. Lenders use FICO scores and other credit details to assess a borrower’s credit risk.

According to Bloomberg, more than 200 million Americans have a FICO score. Here’s what we know about them:

- The average FICO score is about 700. This is what the average FICO score was during the lead-up to the Great Recession.

- Less than 3 million people (1.4%) have a perfect credit score of 850.

- There are over 4 million “super prime” consumers who have FICO scores of at least 800 and above.

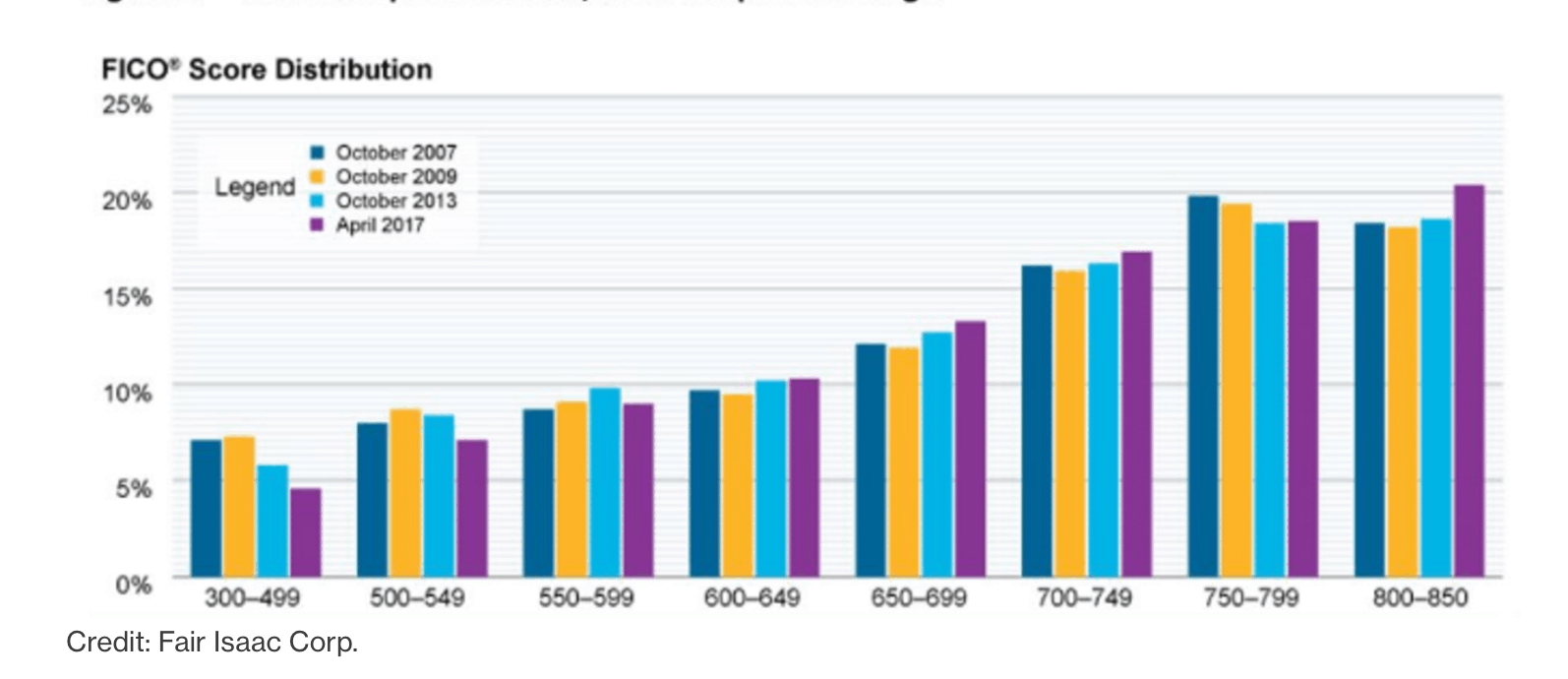

The table below summarizes FICO score distribution through April 2017:

First, let’s deal with the reality of credit perfection. It’s fine to strive for a perfect FICO score of 850. But there is little marginal value to having a perfect credit score, versus, say, a score of 750. So, if you’re in that above average range, take a deep breath and relax.

But you still may want to strive for perfection or as close to perfection as possible. Improving your credit score takes patience and discipline. Here are several steps that will help the process as outlined in MYFICO.com:

- Set up payment reminders. Timely payment is an important factor in maintaining a strong credit score. Many banks send automatic reminders. It’s also easy to set up automatic bill paying through your bank’s website.

- Reduce the amount of debt you owe. Yes, this is easier said than done, but it is possible. Organize your payments to focus on debts with the highest average interest rate. These are often credit card payments.

- If you miss payments, act quickly. Get current and stay current. The longer you pay your bills on time after being late, the more your FICO scores will increase.

- Keep balances low on credit cards and other “revolving credit.” Maintaining high credit card balances has a considerable impact on your credit score.

- Don’t open new credit cards that you don’t need to increase your available credit. In particular, avoid opening a card to save X% during the Chinos sale at your local department store. This is an impulse decision that lowers the average age of your credit history.

- Remember that closing an account does not make it go away. Hold onto your credit cards. The length of your credit history helps improve your score over time.

- Limit how much available credit you use to 30% per card.

- Secure a higher credit limit but keep your spending in check.

Of course, you may need to first fix your credit score. This often means correcting errors on your credit history. Once you fix your credit score, follow the guidelines above to maintain a solid credit history. You’ll need to be patient as you strive to raise your FICO score. And, as we said above, while perfection is nice, it’s not worth the energy in the final analysis. It may be good for your self-esteem, but it’s not likely to get you a line of credit than the slightly lower credit score. So, relax and be slightly above average like the rest of us.