On March 27, Congress passed the CARES Act, which gave Americans both direct stimulus checks and enhanced unemployment benefits to soften the blow of the economic fallout of COVID-19.

The goal, of course, was to salvage the ravaged U.S. economy by having Americans put the lion’s share of the stimulus money into increased consumption.

Did the strategy work?

In today’s post we address this question, using a recently-released study by the Federal Reserve Bank of New York. The Fed did a deep dive into America’s post-COVID spending strategies using its Survey of Consumer Expectations, a nationally representative, internet-based survey of about 1,300 households.

WHERE DID THE CARES STIMULUS MONEY GO?

The Fed reports that 89 percent of respondents said they received some level of stimulus support, made up of direct stimulus checks and other support, such as unemployment benefits. The mean level of stimulus support across all respondents averaged $2,400.

Interestingly, the bulk of stimulus money did not go into increased consumption, as we see below:

- 29 percent of stimulus money was used for household consumption

- 35 percent was used to pay down existing debt

- 36 percent went to household savings

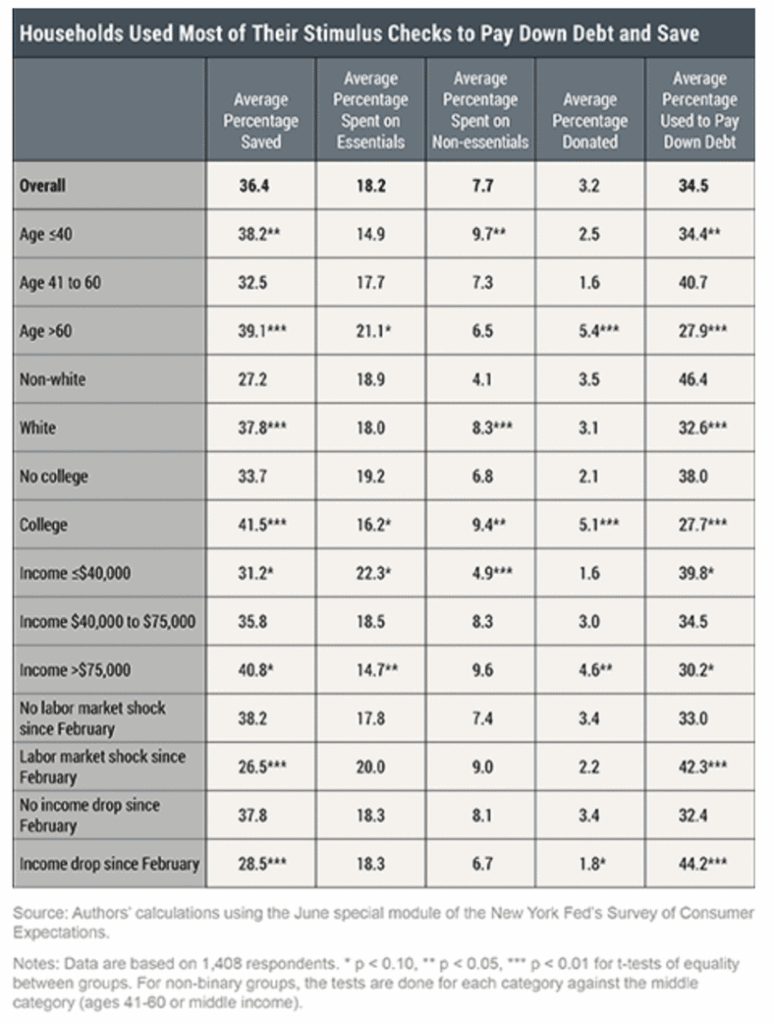

The table below breaks out household stimulus allocations for savings, consumption (essential, non-essential, donations) and debt-reduction by a variety of demographic and economic factors.

Here are a few highlights:

- In general, older, white, college-educated, higher income Americans put more into savings and less into debt reduction compared to other groups.

- Middle-aged households tended to be more prudent than other groups, putting more toward savings and paying down debt, and less in consumption, especially of non-essential items.

- Younger, college-educated, upper-income Americans spent more on non-essential items that other groups.

- Those who experienced “labor market shock,” put significantly less money into savings than their counterparts, and focused on spending stimulus money on essential items, plus paying down as much debt as possible.

- We see similar patterns with those who experienced a drop in income, with lower levels of savings and more debt-reduction.

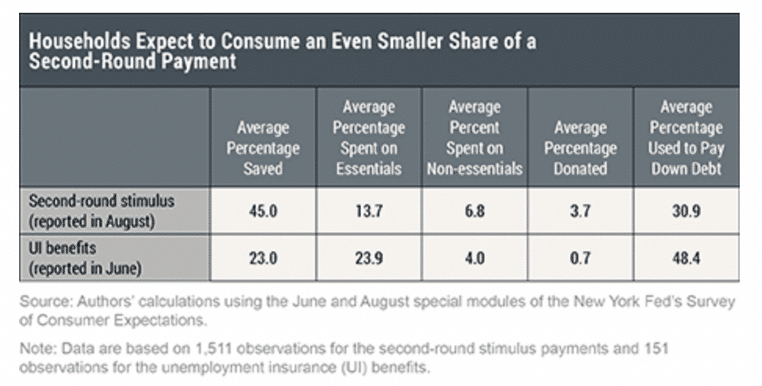

HOW WILL AMERICANS SPEND FUTURE STIMULUS CHECKS?

As of this writing, it appears that Congress will not pass a second stimulus package. However, the Fed report explored how Americans would spend a second round of stimulus money, should things change.

Looking at the table below, we learn the following:

- Compared to current allocations, Americans say they will put significantly more (45 percent vs. 36 percent) into savings.

- Conversely, they will put less toward paying down debt and significantly less (-25%) toward household spending.

It’s interesting that less than one-third of CARES money went toward true economic stimulation, as measured by increased consumer spending. As the report shows, most people chose to be prudent with their CARES allocations, focusing on savings or paying down debt.

Still, as we look back over the past six months, it’s safe to say that CARES did, in fact, initially stimulate the economy. Looking at the most recent data from the Bureau of Economic Analysis, we see that:

- After a historic 12.7 percent drop in Personal Consumption Expenditures (PCE) in April, spending picked up, quite significantly, in the following two months, before leveling off in recent months:

- May: +8.7 percent (vs. prior month)

- June: +6.5 percent

- July: +1.5 percent

- August: +1.0 percent

It’s worth noting that both personal and disposable income are down in August, 2.7 percent and 3.5 percent respectfully. This might explain why PCE has flattened, and also suggests the possibility of sluggish spending in the near-term.

You can find a link to the full BEA report below.

We will update this report as new data becomes available.

SOURCE

https://www.bea.gov/news/2020/personal-income-and-outlays-august-2020