We are beginning to see an uptick in credit card delinquencies.

While still well below the delinquency levels of the Great Recession, rising delinquencies hint at increased losses for lenders. Buoyed by full employment and a healthy economy, lenders are more willing to take risks by extending loans and credit cards to consumers with lower credit scores.

Andrew Haughwout, Senior Vice President of the New York Federal Reserve Bank, said: “We have seen some loosening of standards on card originations: low credit score individuals getting credit cards or extended limits, allowing them to borrow more.”

WHAT CONSTITUTES DELINQUENCY

A credit card becomes delinquent when a consumer falls behind on payments.

In everyday use, any account past due is a delinquent account. However, a credit card issuer will not report an account as delinquent to the credit bureaus until a cardholder has failed to make at least a minimum payment for at least 30 days have passed since the due date.

Importantly, delinquency is not reported to the major credit reporting bureaus until payment is late by 30 days or more. In essence, every consumer gets a grace period about repayment and their subsequent credit score.

The obvious downside with successive, missed payments is a dramatic impact on your credit score. While your score will dip at 30 days delinquent, your credit score can drop by as many as 125 points after 60 days.

The following is taken directly from the 2nd Quarter 2017 Federal Reserve Bank of New York Report on Household Debt and Credit as authored by Andrew Haughwout, Donghoon Lee, Joelle Scally, and Wilbert van der Klaauw.

The Report reflects that overall debt balances increased in the period, continuing their moderate growth since 2013. Nearly all types of balances grew, with mortgages and auto loans rising by $64 billion and $23 billion, respectively. Credit card balances increased by $20 billion, recovering from the typical seasonal first-quarter decline.

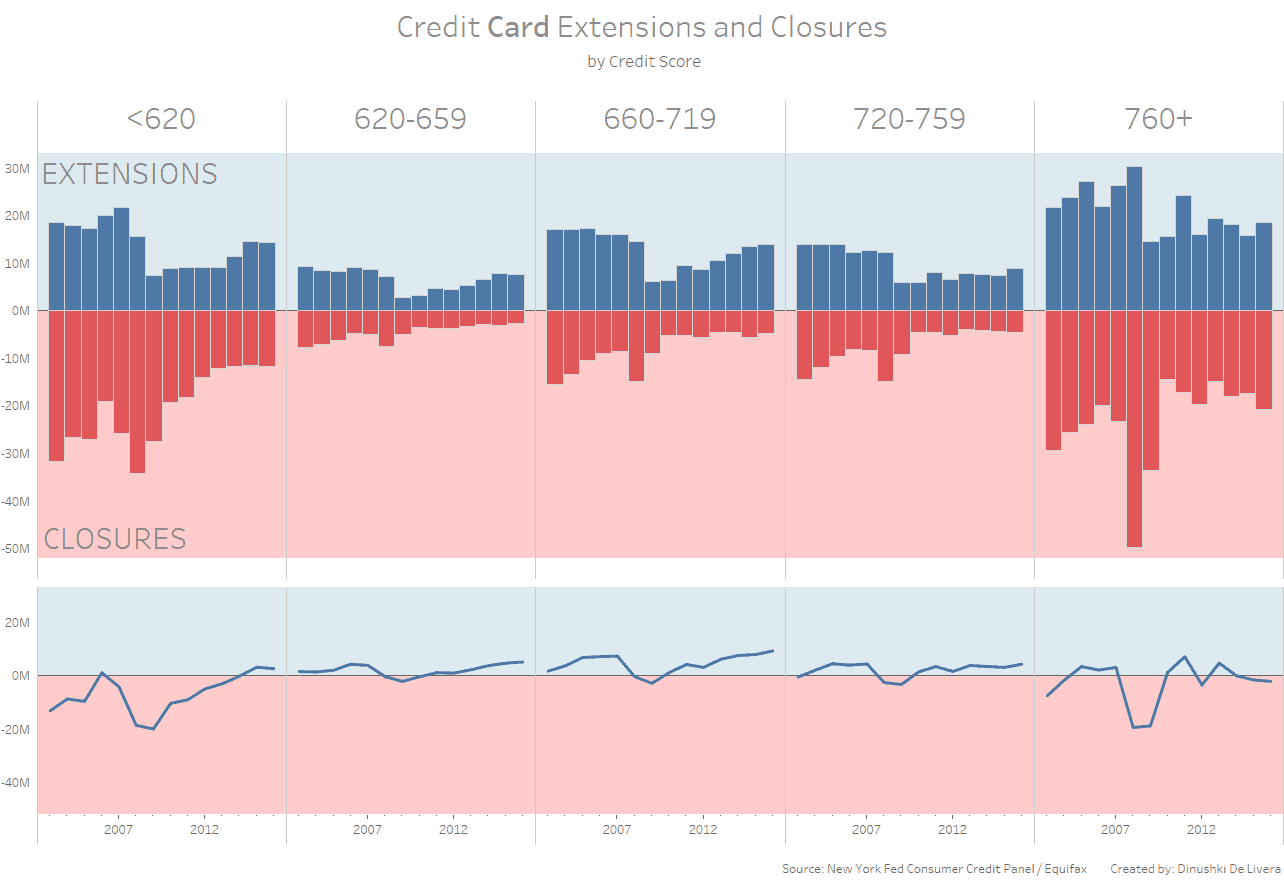

Credit Card Originations

The chart below depicts card issuance and account closure, by credit score band. There has been a net increase in credit card accounts (new accounts minus closed accounts), a trend observed since the sharp decline prompted by the CARD Act in 2009. Disaggregated by type of borrower, new accounts issued to nonprime borrowers (with scores below 660) were flat in 2016 after increasing the previous two years. So, the overall growth in issuance is due to more cards being issued to prime borrowers with credit scores over 660.

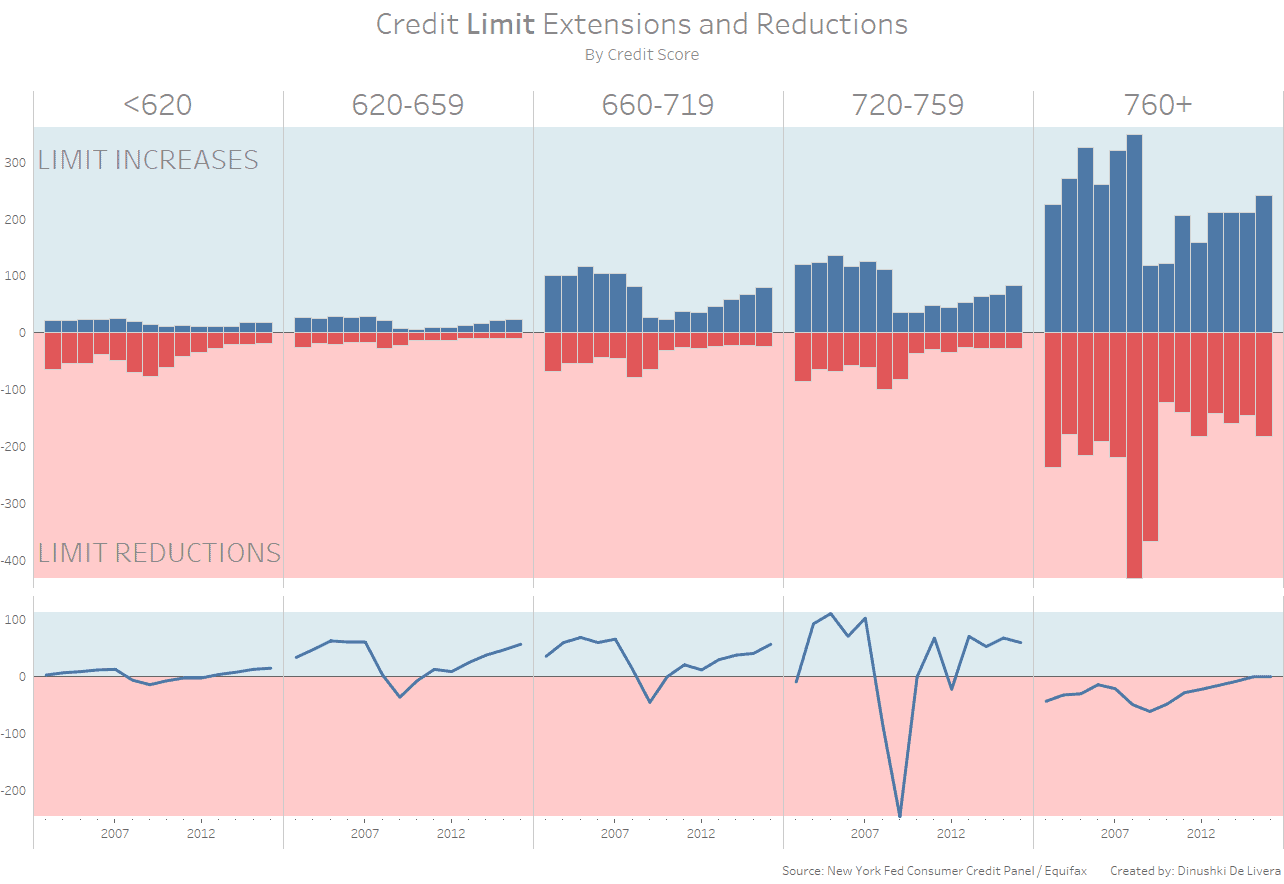

We also see continued growth in aggregate credit limits, with disproportionate increases to higher-credit score borrowers (see chart below); aggregate limits have grown notably in the last year, but the growth is primarily due to limit extensions to higher-score borrowers. The median threshold on new cards for borrowers with scores over 760 was $8,500 in 2016, while the median limit of borrowers with credit scores under 620 was $750, as banks manage risks inherent in unsecured debt to nonprime borrowers. So, while we see some moderate increase in the limits of nonprime borrowers, it is a tiny piece of the aggregate, and that mitigates risks stemming from the rise in card issuance to lower score borrowers.

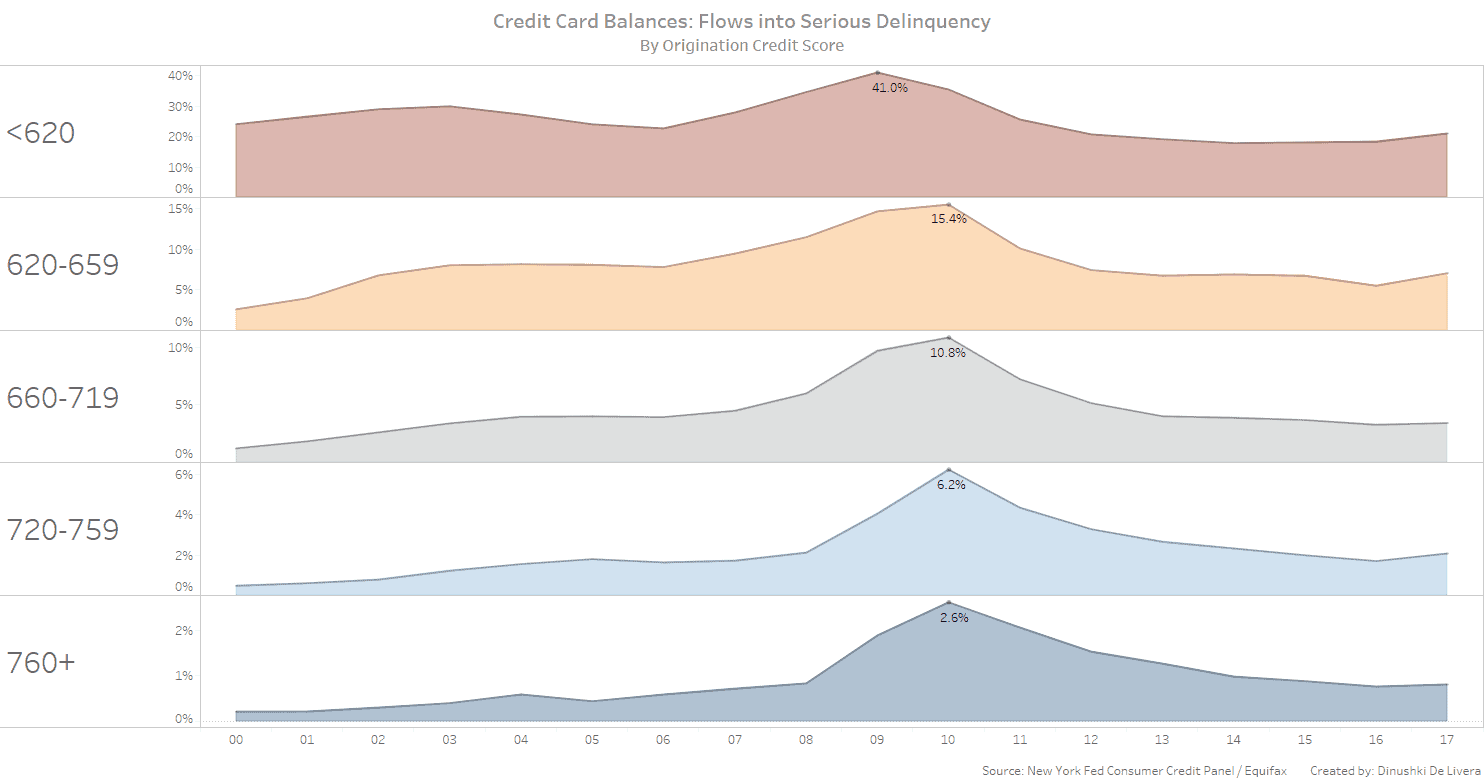

Delinquency

We noted last quarter that transitions into delinquency for card balances had increased, following upticks in the two previous quarters. The transition into serious delinquency is defined as balances that have gone from current or early delinquency into ninety or more days late, as a percentage of the balance from the previous quarter that was less than ninety days past due. This growth is potentially concerning, particularly in the context of a healthy economy and low interest rates. In the chart below, we disaggregate the delinquency transitions by credit score band. We don’t observe individual accounts in the Consumer Credit Panel for credit cards, so we use the credit score for each during the quarter that a consumer has most recently opened a new card. We’ve smoothed our data using four-quarter moving sums to minimize seasonal changes.

We see a notable increase in the transition to ninety-plus days delinquency primarily in the lower two credit score buckets, so the consumer distress appears to be limited to those borrowers (although there are small increases in the transition rates for the prime groups as well). The restoration of access to credit for lower-score borrowers has been a long time in the making, and the lower delinquency transition rates between 2013 and 2015 might have been anomalous, primarily owing to tighter standards during the Great Recession and after. Looking over the full span of data, the latest transition rate of 22 percent per year for subprime accounts is still low.

We will provide an update on the Fed issues the Q3 report.

SOURCES:

http://www.investopedia.com/articles/pf/11/intro-to-credit-card-delinquency.asp