In the second part of our series on credit card debt, we examine the use of credit cards as a payment choice and how credit card debt affects choice.

In review, the data comes from a study commissioned by the Federal Reserve Bank of Boston, which drew on two sources of information: first, the Survey of Consumer Payment Choice (SCPC), a nationally representative survey of self-reported consumer payment behavior conducted annually and, second, Equifax, one of the nation’s three major consumer credit reporting agencies, which provided administrative data.

Credit cards are a unique method of payment because they can be used as a source of credit in addition to serving as a means of payment. Identifying consumers who borrow on their credit cards allowed the Fed to analyze their other payment habits and preferences to see if they behave differently from those who repay their credit card balances each month.

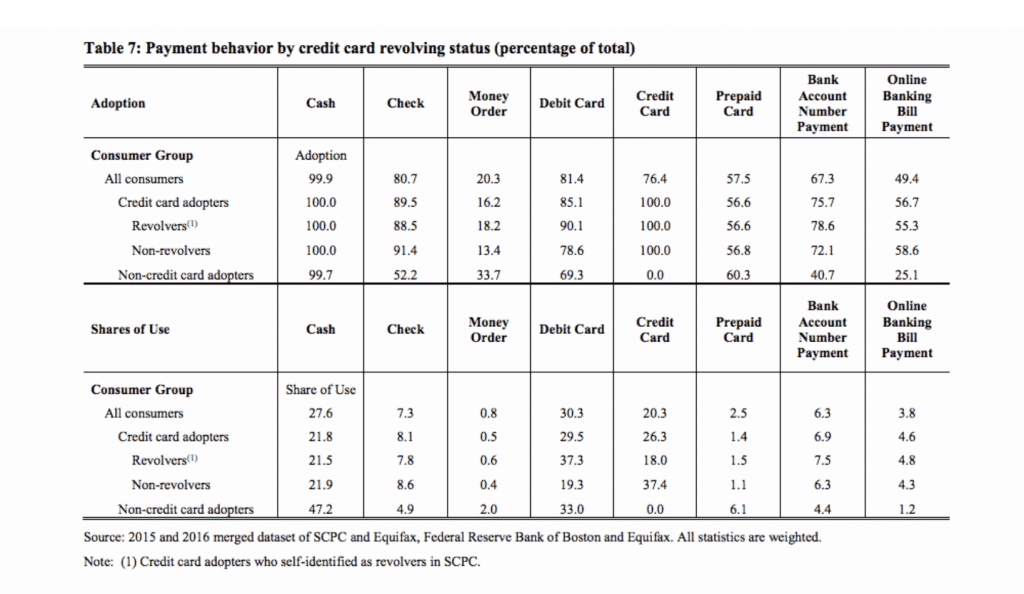

As part of the analysis of the relationship between payment preferences and credit card debt, the table below shows the rates of adoption and shares of use of various payment methods for all consumers and breaks down use by credit card revolvers and non-revolvers

Note that credit card revolvers are more likely to have a debit card than consumers who pay their credit card balances on time (payment method adoption, top panel of above chart). In the sample, 90 percent of revolvers and 78 percent of non-revolvers hold a debit card. Comparing the shares of use by payment instrument (bottom panel), revolvers have much higher shares of debit card transactions and much lower shares of credit card transactions, relative to convenience users who pay their credit card bills on time. On average, revolvers use debit cards more than twice as frequently as credit cards (37 percent versus 18 percent),while convenience users do the reverse: They use credit cards twice as often as debit cards (37 percent versus 19 percent). Credit card revolvers might avoid using their credit cards in order to curtail their debt, or so that at least they don’t increase their debt.

Revolvers differ from convenience users along the demographic and financial attributes, as we discussed in our earlier post. Compared with convenience users, revolvers are more likely to have lower income and be less educated. Thus, unconditional differences across income and education hold even when the probability of revolving is conditional on having a credit card.

The probability of revolving increases slightly with age, albeit at a decreasing rate. Being black or unemployed does not increase the probability of revolving, conditional on having a credit card.

The Fed also found that revolvers use their credit cards less frequently than convenience users do, but also found income and demographic attributes affect who revolves.

Revolvers use their credit cards less frequently than their debit cards, but they carry balances that are several thousand dollars higher than those of convenience users on average.

In summary, as credit risk scores rise, consumers increase their credit card balances initially, but above the score of 750, credit card balances decline with the risk score. Credit card revolvers differ from consumers who pay their balances each month: They are more likely to have lower income and less education. They also are much more likely to use a debit card instead of a credit card, but revolvers carry much higher balances on their cards, even controlling for demographic and income attributes.

Consumers who carry debt might be liquidity-constrained and not have cheaper borrowing alternatives. Payday loans, for example, are likely to be even more expensive than credit card loans, while home equity loans are not available to nonhomeowners. Thus, supply-side constraints may cause credit card revolving. The high cost of paying off credit card debt could exacerbate existing inequalities in disposable income among consumers.

SOURCE