Last week’s post explored the question of whether or not increasing house prices are pushing us in the direction of another HOUSING BUBBLE.

Indeed, while housing prices have grown dramatically during the pandemic, we showed that the situation is much different than during the lead-up to the Great Recession when we had three years of double-digit (14 percent on average) housing price increases.

Today, we return to the Federal Reserve’s analysis to explain what might happen to the housing market in the event of sustained drops in housing prices in the coming year. Would such a “shock” replicate what happened in the early 2000s and plunge the economy into another deep recession.

MORTGAGE PERFORMANCE INDICATORS

In general, the Fed points out that the fundamentals today are much different and more stable than during the pre-crisis period.

One compelling data point is that the “owners share of housing wealth” is at 67 percent, a level not seen since 1989. This number refers to the property’s value minus the debt owed, expressed as a share of property value.

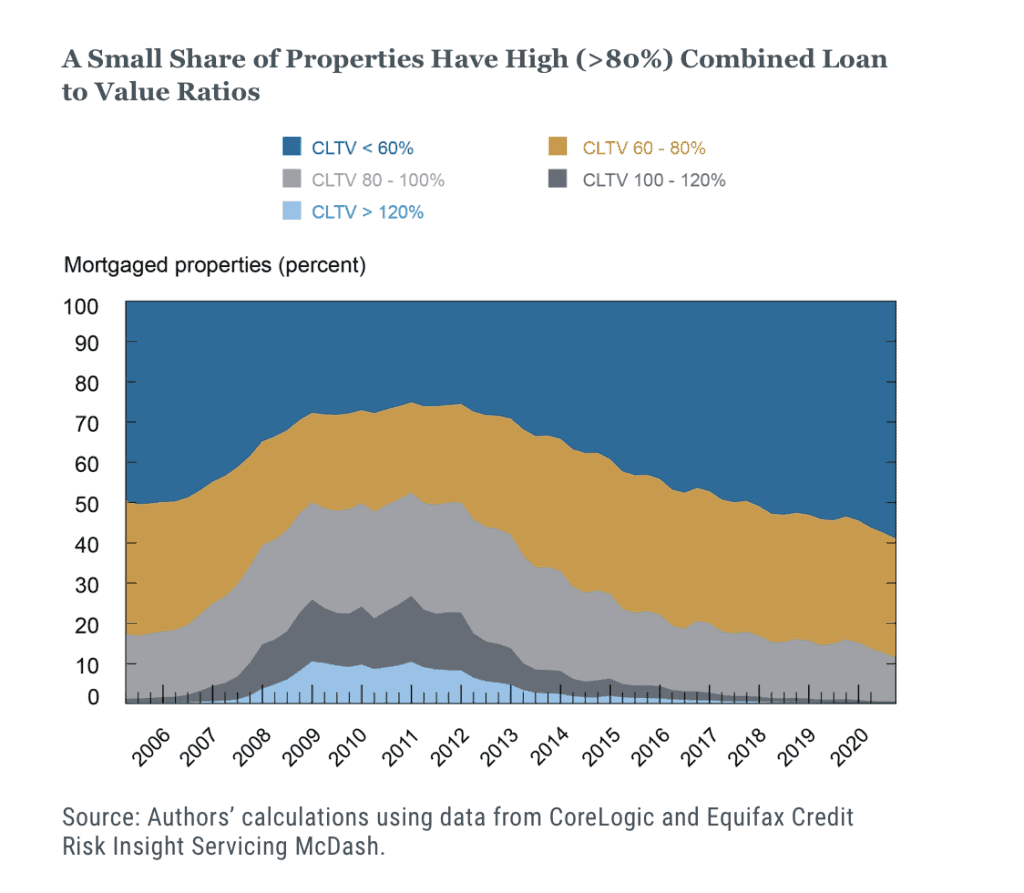

But, as this is an aggregate figure, the Red took a deeper look at the “leverage” situation by studying Combined Loan to Value (CLTV) rates for a large segment of mortgage properties.

The chart below looks at CLTV distribution across current mortgage borrowers through December 2020:

- Blue and light gray indicates properties in “negative equity,” meaning CLTV over 100 percent.

- Light gray, gold, and dark blue highlight decreasing levels of leverage.

Importantly, if you look at the blue and light gray bands, negative equity today is at minimal levels compared to the levels seen in 2009-2011. By contrast, more than 85 percent of all properties have a CLTV below 80 percent, giving them more cushion against future shocks.

However, it’s worth noting that American homeowners had similar levels of equity in 2006. But again, there is a significant difference between then and now, and that is creditworthiness:

- More than two-thirds of mortgage debt in 2020 was held by those with FICO scores of 740 or above. In 2006, 50 percent of mortgages were held by borrowers at 740+.

- Perhaps more importantly, 20 percent of mortgage debt in 2006 was held by borrowers with scores under 660; we are at half that level in the current market.

So, again, the fundamentals suggest we are in a much stronger place today than in the early 2000s. But the Fed wanted to push the analysis by theorizing what might happen if housing prices began dropping.

A SHOCK TO THE SYSTEM?

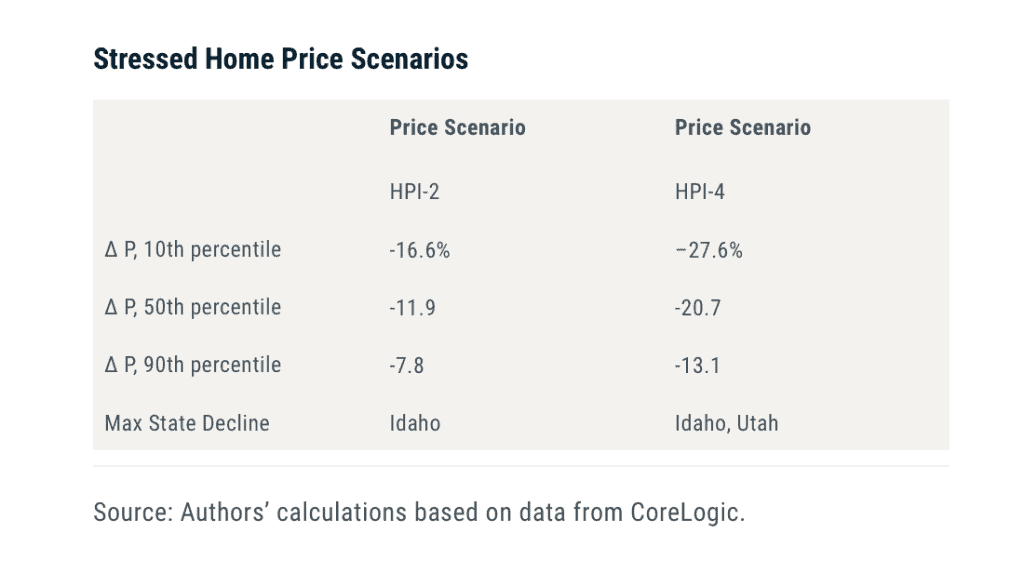

To address this question, the Fed calculated potential delinquencies based on two dramatic price decline scenarios: revert to levels from two years ago (HPI-2) and four years ago (HPI-4).

Using county data from CoreLogic, the table below breaks out what housing price increases would look like at the 10th, 50th, and 90th percentile for each scenario. As you can see, the median county under the most severe HPI-4 scenario would see housing prices drop by 27 percent. Even the 10 percent, least affected counties would experience a double-digit drop in prices.

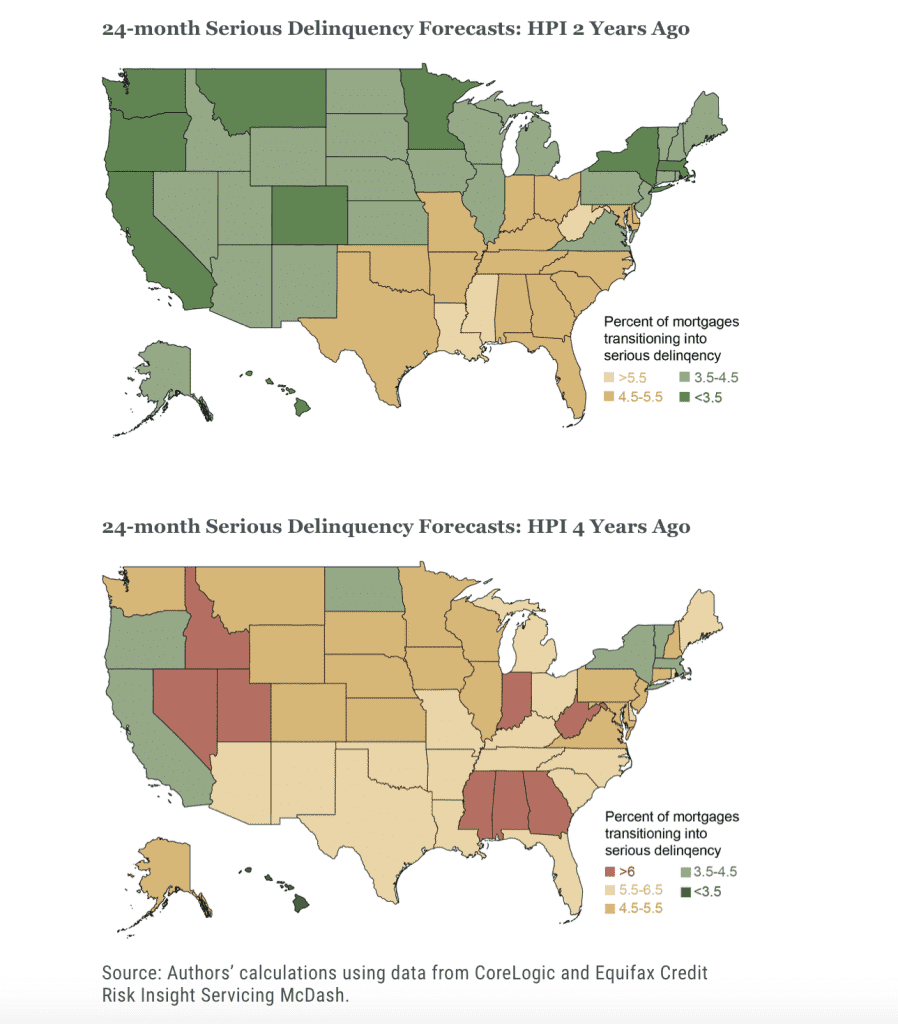

Using the same data, the maps below depict the potential for mortgages to transition into default under each scenario. The Fed used 2007-2010 default rates for each CLTV and FICO score combination to estimate transition rates. On a national level (not shown):

- 3.9 percent of mortgages would transition into default under the HPI-2 scenario by December 2020, and 5.1 percent for the four-year scenario.

While these are dramatic increases in default rates, it’s still worth remembering that they would be well below the default levels experienced throughout the Great Recession.

Concerning state-level impacts of price declines:

- Arizona, Florida, and Nevada were three of the hardest-hit states during the crisis and would continue as high-risk areas for increased mortgage defaults.

- California, which was hit extremely hard during the recession, is now a below-average risk for increased defaults.

- A handful of states that have seen robust and recent price increases would not be vulnerable to dramatic price drops, namely: Georgia, Idaho, Indiana, Mississippi, and Utah.

But again, the Fed stresses that, while some states are currently vulnerable to sudden drops in housing prices, it’s doubtful any would experience the kinds of devastating default rates seen nationally during the crisis or in the hardest-hit states mentioned above.

We will likely see the housing market “normalize” in 2022. But even in the event of price declines, the healthy fundamentals outlined above (and in the previous post) should keep the overall housing market (and by extension, the U.S. economy) on solid ground.

SOURCE

Andrew F. Haughwout and Belicia Rodriguez, “If Prices Fall, Mortgage Foreclosures Will Rise,” Federal Reserve Bank of New York Liberty Street Economics, September 8, 2021, https://libertystreeteconomics.newyorkfed.org/2021/09/if-prices-fall-mortgage-foreclosures-will-rise/

To learn more about Recovery Decision Science’s Business Intelligence Team, contact:

Kacey Rask : Vice-President, Portfolio Servicing

[email protected] / 513.489.8877, ext. 261