In August 2017, Unifund partnered with PYMNTS.com to conduct a study of Financial Invisibles in American society. By definition, the Financial Invisibles are those who don’t fully participate in traditional banking and financial systems.

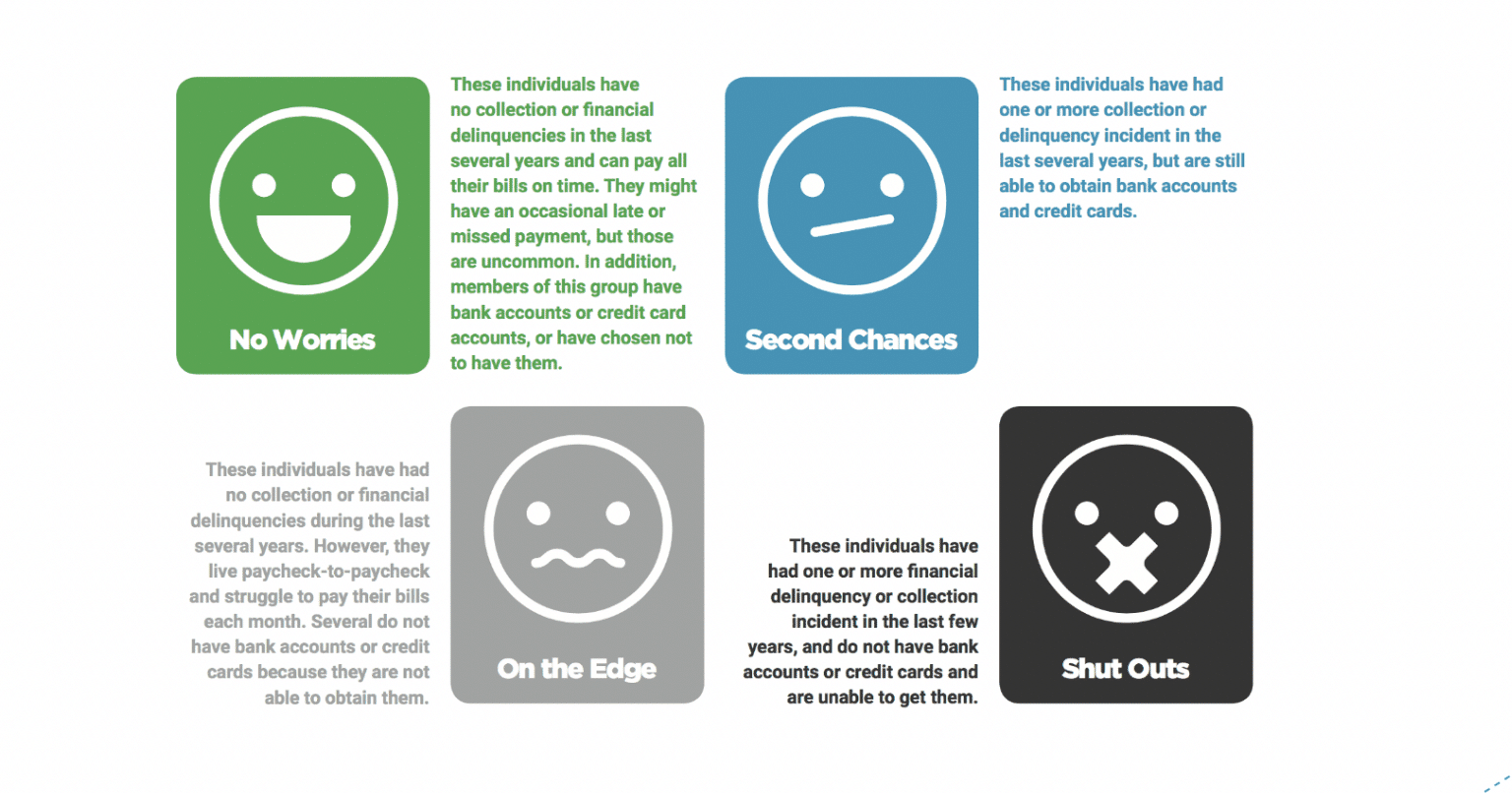

To examine the reasons why so many Americans still don’t use credit cards or even hold checking accounts, PYMNTS.com initially surveyed a 2,000-plus person demographic mix that mirrors the total population and divided the survey group into four financial consumer categories:

In spring 2018, they again surveyed a sample of more than 2,000 Financial Invisibles to see if their circumstances had improved, worsened, or stayed the same from 2017 to 2018.

Over the course of this 4-part blog series, we’ll explore the results of the studies, documenting what the initial survey found and the evolution of the survey population’s financial well-being from the time of the first survey to the second one. We will take deep dives into examinations of how each group defined above handles various financial situations, including bill payment and use of credit products. We’ll examine the differences in Voluntary Invisibles – those people who have the ability to fully participate in the financial system but opt not to – and Involuntary Invisibles – those who, through delinquencies and poor credit, have no option to participate.

The August 2017 study served as a baseline from which we can compare later studies to track trends.

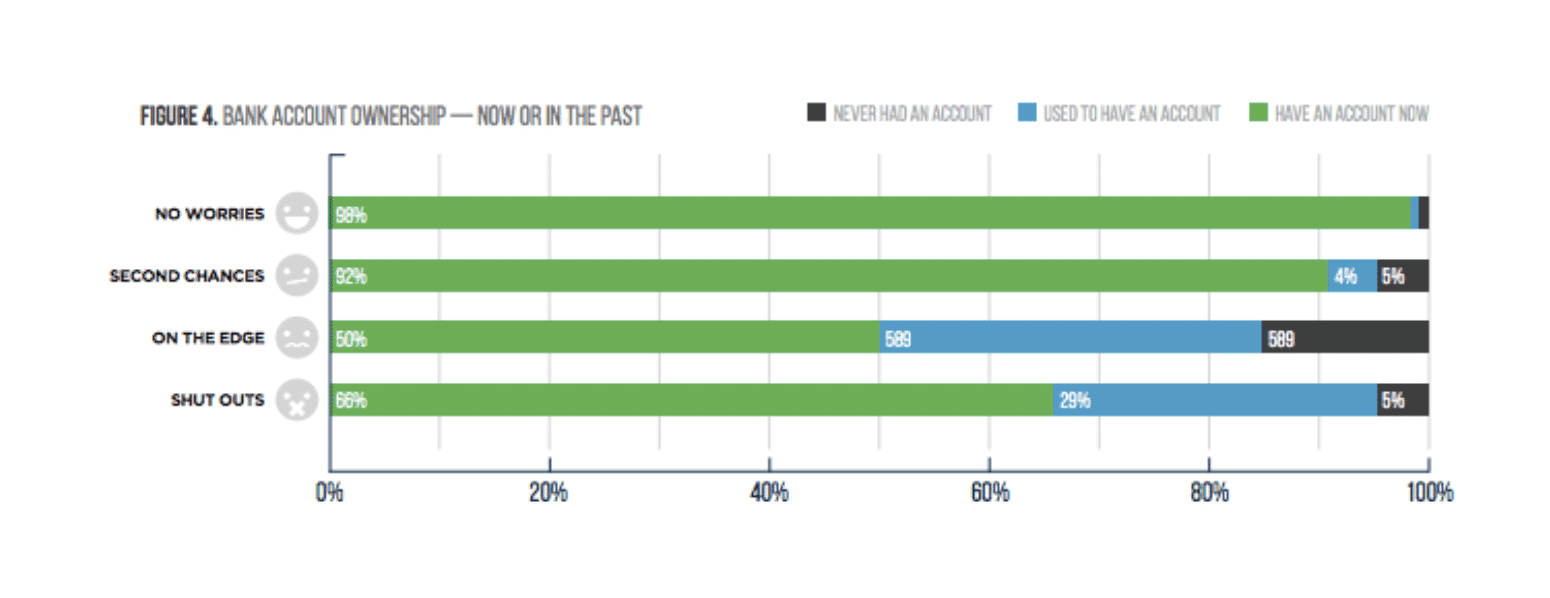

Key findings of the baseline study revolved around the use of traditional financial tools. Eighty-six percent of respondents reported having either a checking or savings account and two-thirds of those who don’t currently hold a bank account have had one in the past. However, the figure below graphically demonstrates a drastic break in current account holders between the top two and bottom two levels: 98 percent of No Worries and 92 percent of the Second Chances groups are current account holders, while only 50 percent of On the Edge and 66 percent of Shut Outs have bank accounts. As the chart shows, small percentages in each group have never had bank accounts.

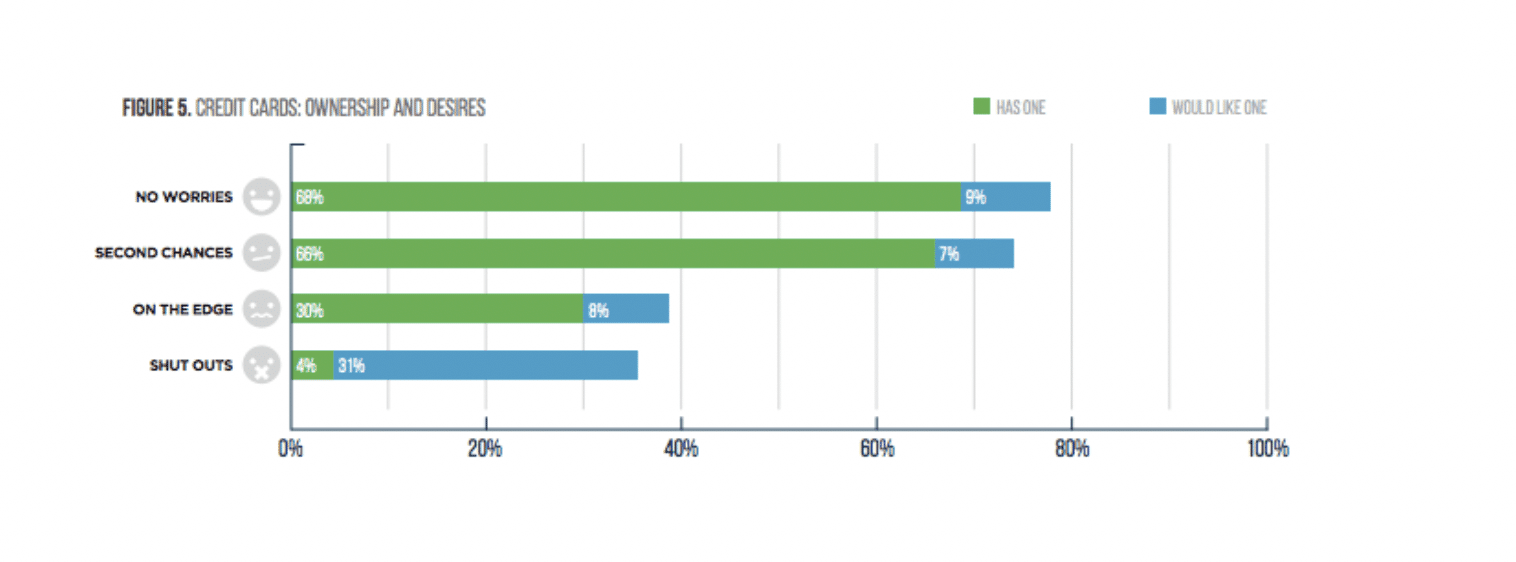

The drop-off is even steeper in use of credit cards. Of the No Worries, 68 percent have credit cards and 66 percent of Second Chances do, while a mere four percent of Shut Outs report holding credit and only 30 percent of On the Edge. Except for the case of Shut Out, most of those without credit cards say they don’t want one. Thirty-one percent of Shut Outs, however, would like to obtain a credit card.

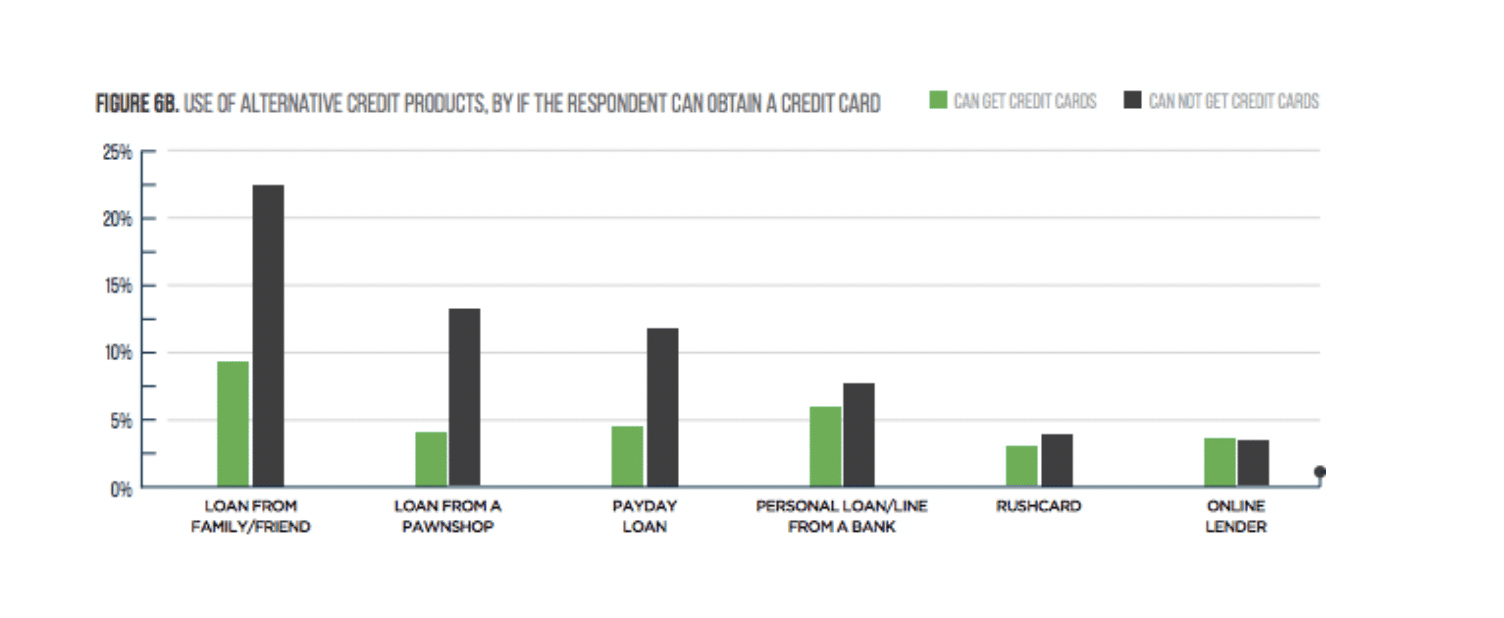

Those who aren’t able to get credit cards are far more likely to use non-traditional financial products, including pawn shops, payday loans and even personal loans from friends or family.

The next post in this series will take a closer look at the two groups who comprise the largest segment of those who are considered Financial Invisibles: Shut Outs and On-the-Edge.

Here is a link to the full Financial Invisibles Report