The New York Fed recently released its quarterly report on household debt in America. In today’s post, we’ll take a look at the highlights of the report.

KEY HIGHLIGHTS

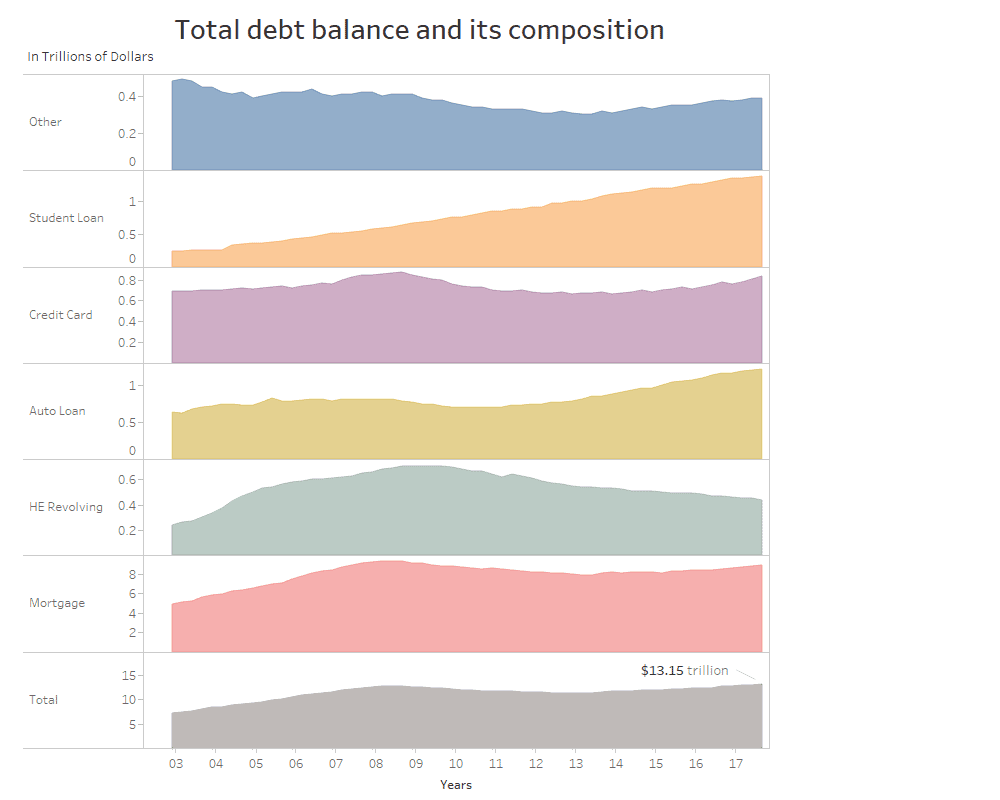

As of December 31, aggregate household debt in the United States is at $13.15 trillion:

- The aggregate debt is now $473 billion higher than the previous peak of $12.68 trillion in Q3

- Aggregate household debt has increased for the 14th consecutive quarter.

- Q4 2017’s increase of $193 billion was 1.5% over Q3 2017.

- Mortgage balances increased significantly during Q4 2017:

- As of December 31, mortgage balances were at $8.8 trillion-increasing $139 billion versus the previous quarter.

- HELOC (Home Equity Lines of Credit) declined slightly, by $4 billion, to $44 billion.

- Non-housing balances continued their upward trend, growing $58 billion for the quarter, the key components including:

- Auto loans balances: +8 billion.

- Credit card balances: +$26 billion.

- Student loan balances: +$21 billion.

NEW CREDIT

New extensions of credit declined slightly in Q4 2017:

- Mortgage originations (identified as new mortgage balances on consumer credit reports and refinanced mortgages) declined $27 billion from Q3 to $452 billion.

- Auto loan originations stand at $37 billion-a slight decline. However, 2017, as a whole, was the highest year ever recorded with regard to auto loan originations.

- Aggregate credit card limits rose 1%, which was the 20th consecutive quarter of growth for this category.

DELINQUENCY RATES/CREDIT

Overall, delinquency rates improved in Q4 2017. As of December 31st, 4.7%, $619 billion, of outstanding debt was in some stage of delinquency:

- $406 billion is in serious delinquency (at least 90 days late or “severely derogatory”).

- Credit card flow into 90 days of delinquency has been increasing notably from the previous year.

- The flow into 90+ day delinquency for auto loan balances has been slowly increasing since 2012.

About 200,000 consumers had a bankruptcy notation added to their credit reports in Q4 2017-an improvement versus the same time a year ago.

In terms of credit scores for newly-originating borrowers:

- Declined from 760 to 755 for mortgage borrowers.

- Increased from 705 to 707 for auto-loan borrowers.

For more detail, here is a link to the full report: https://www.newyorkfed.org/medialibrary/interactives/householdcredit/data/pdf/HHDC_2017Q4.pdf