This is the final post in our five-part series covering the New York Federal Reserve’s study on heterogeneity in the United States. Today, we look at Medicare and its impact on financial health, and, in particular, its role in equalizing financial strain.

The Fed reiterates that a critical factor in financial strain is debt in collection-debt that is more than 120 days past due and has been placed with a collection agency. Importantly, there are dramatic geographic differences when it comes to looking at debt in collection. For example, the average Massachusetts resident holds less than $60 in collection debt, compared to Texans with more than $300 on average.

MEDICARE AND DEBT IN COLLECTIONS

Most people qualify for Medicare when they reach 65. By that age, they’ve already begun to make major changes in their lives, perhaps starting with retirement. Many begin to decrease consumption, while others are likely to move in with adult children.

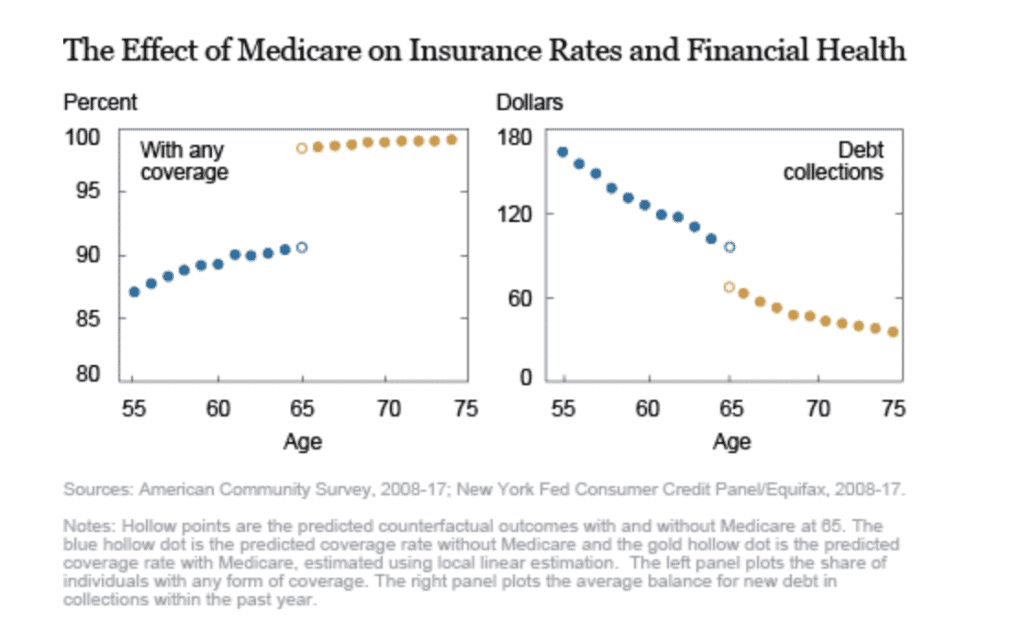

The chart below is interesting because it shows how Medicare dramatically shifts the incidence of debt in collection.

- The LEFT panel (blue dots) shows the level of insurance coverage for aging adults, reaching 92% for 64 year-olds prior to receiving Medicare. With Medicare (gold dots), insurance coverage hits 100% for everyone 65 and older.

- The RIGHT panel charts the corresponding impact with regard to dollars in collections. Again, you see (blue dots), that debt gradually decreases as the population ages, and insurance coverage increases. But when Medicare kicks in, we see a dramatic decrease in debt in collections.

THE BENEFITS OF MEDICARE-GEOGRAPHIC

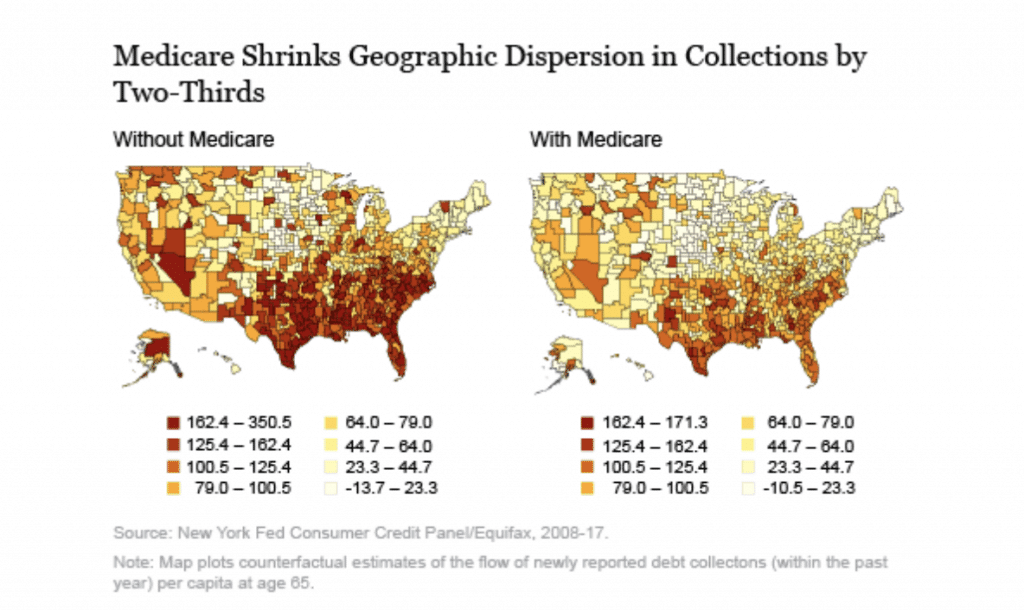

As we note above, there are significant differences in the levels of debt in collections on a state-by-state basis. In the figure below:

- The LEFT panel shows debt in collection before Medicare. You can see the extent of debt in collection throughout the southern tier of states, expanding westward.

- The RIGHT panel reveals the impact of Medicare. Notably, we see a significant shift, or flattening, of debt in collection as those in the southern region begin qualifying for Medicare. For example, the aforementioned gap in collections between Massachusetts and Texas is reduced by two-thirds because of the availability of Medicare.

THE BENEFITS OF MEDICARE-VULNERABLE POPULATIONS

The Fed study also revealed that the financial health benefits of Medicare get distributed in ways that reach poor and vulnerable populations. Most notably, the variables most associated with declines in collections per newly insured are:

- The fraction of residents in commuting zones who are black

- The fraction of residents with disabilities

- The market share of for-profit hospitals (which tend to provide less charity care than non-profits)

THE BENEFITS OF MEDICARE: THE “NEAR ELDERY.”

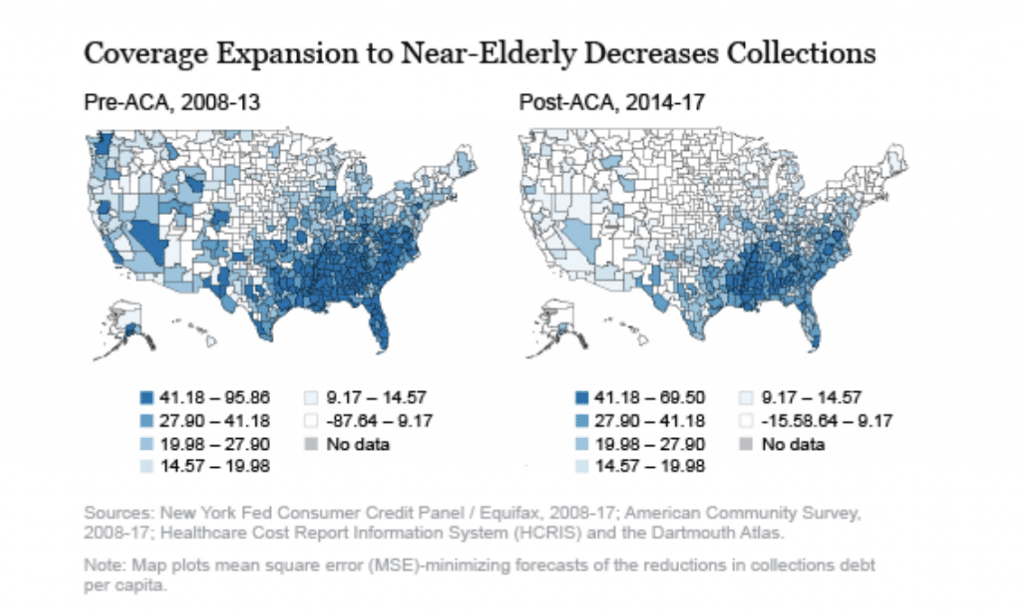

Finally, in an effort to inform future policy decisions, the study took a speculative look the impact of expanding Medicare benefits to the “near elderly,” defined as 64-year old adults.

The figure below shows the geographic distribution of the reduction in amounts of collections that would take place if Medicare were expanded to the near-elderly. One assumes insurance coverage pre-ACA (2008-2013), while the other assumes post-ACA (2014-2017) coverage.

The report made a few interesting conclusions:

- As you can see from the RIGHT panel, expanding Medicare to the near-elderly reduces the amount of debt in collections, especially in the southern tier of states.

- However, the ACA actually reduces the overall benefits of expanding Medicare coverage to the near-elderly. That’s because the ACA helped most of the near-elderly to obtain health insurance, either through Medicaid expansion or the health insurance exchanges.

Clearly, this study shows the value that health insurance plays in the heterogeneity of financial strain across the country. In conclusion, the Fed had this to say:

“Even universal programs like Medicare have different impacts on different parts of the country. Importantly, understanding these regional variations can ultimately have an impact in drafting policies to reach the people who are most in need of help.”

If you would like to read the full report, CLICK HERE.